Sive Morten

Special Consultant to the FPA

- Messages

- 18,621

EUROPEAN FOREX PROFESSIONAL WEEKLY

Analysis and Signals

October 22, 2009

Analysis and Signals

October 22, 2009

Fundamentals

Equity earning reports that have been released during the week have shown that, in general, the economic recovery is underway. Some companies, such as Industrial and Construction, were a bit worse, others were better, such as the technology sector. There were some unexpected unwelcome surprises, such as BAC looses. Nevertheless, data shows that the recovery is still going, and this is the main factor. The reports in general were better than most investors expected, combining with low USD borrowing rates keep pressure on USD.

There were not many macro data during the week. The particularly interesting one was real estate data – Building permits, Hosing starts and PPI. The main surprise was from PPI that have fallen below expectation and had shown disinflation in Producer Prices (-0.6% vs. 1.7% growth in previous month). Real estate data was mixed and relatively neutral – it pointed that growth pace has lost some momentum, but it still ongoing.

So, as a result, we have relatively understandable picture inside the US for some time – growth has lost some momentum, but data shows that it is still growth. Besides, inflation is low and it keeps the fund rate low for a considerable time period. All these facts stimulate investors to actively enter in more risky assets and fund them with USD loans that press on the USD even more strongly.

Run for yield is continuing. From the other side, it worth noting, that there is a risk for second leg of recession still. And the main factor is problems in loan sector. As I mentioned in previous research, JPM has reported that the main income it received is from investments and not from commercial banking that is still depressed. So, there is a possibility that banks will make some loose provisions (delinquencies, foreclosures processes, toxic assets etc) in statements and the level of reserves still will be high. The main question is: will the time that Fed’s have given to banks, due to the fiscal program, be enough to reanimate the loan sector? Will banks be able to magnify loans when the Fed’s economic push effect fades? If not, second leg of recession will have a solid probability.

As for near-term, the macro data from China is particular interesting. It will be released today (Oct-22). It can set a direction for the whole next week. If the data will be better than expected, that will be pressure on the USD. Prior to the US open the market will digest a slew of Chinese economic reports including GDP, industrial production, retail sales, PPI and CPI. The market believes that the global recovery is very much tied to the performance in China and thus the release of these macro figures will be acutely watched.

Now let’s look at our “Basic macroeconomic issues” that we have pointed in August. Now we see point 1; partially, point 3 - we see a growth of these positions for now and USD weakening (By the way, this was a reason of fast USD grow at the second half of 2008) and point 7 that includes the whole chain of economy growth phase. The main thing that we are waiting for – is point 2 (but there is risk left that it can be point 3 (recession second leg) instead.

Basic macroeconomic issues:

1.Investors basically pay attention only to the nearest perspective. Since FED rate tightening is too blurring, we should not to expect meaningful USD strengthening until next year (or till first signs of a rate hike possibility);

2.USD will become stronger when investors see these signs, so the expectations concerning EUR/USD rates parity will change;

3.We can expect growth in the USD, if the possibility of second leg of recession will grow, and if investors will have large borrowing positions in USD;

4.EU economic recovery will have a time lag about 1-2 quarters compared to the US recovering;

5.When EU rates hike expectation will appear, the dollar will turn to weaken;

6.We can see temporary USD strengthen from time to time due some technical movements (risk aversion, stocks buying etc) until the first signs of a rate hike possibility appear.

7.The primary US economic data that will be under scrutiny are personal credit, spending, wages and employment, inflation. This is a final segment in the chain, and it’s very important.

Technical

Previous “trade possibilities(1)” Oct-15-2009:

Monthly:

Momentum is up; extreme price for October is 1.52-1.5240 level. Possibly it can be reached.

Weekly, Daily:

Still no signs of reversion or retracement. The most important thing – expansion at 1.4950 that market has reached on weekly chart. We have to check this important movement. Possibl,y we see some signs of retracement on next week. All the other factors have nothing to say – up trend, up momentum, no overbought levels.

I will post in forum topic, if signals for short-term short position or any signs of retracement will appear in nearest days. I did this last week when an opportunity appeared:

It looks like reverse formation is appeared on 4H chart.

I think that now is possible to go short (around 1.49-1.4920) with s/l 1.4970 (but probably 1.4950 will be enough, the point is that formations can be volatile) and nearest profit 1.4845, but 1.4790 is also possible to reach.

1.4845 was reached (low was 1.4828), s/l 1.4970 was untouched. The 1.4790 target wasn’t reached.

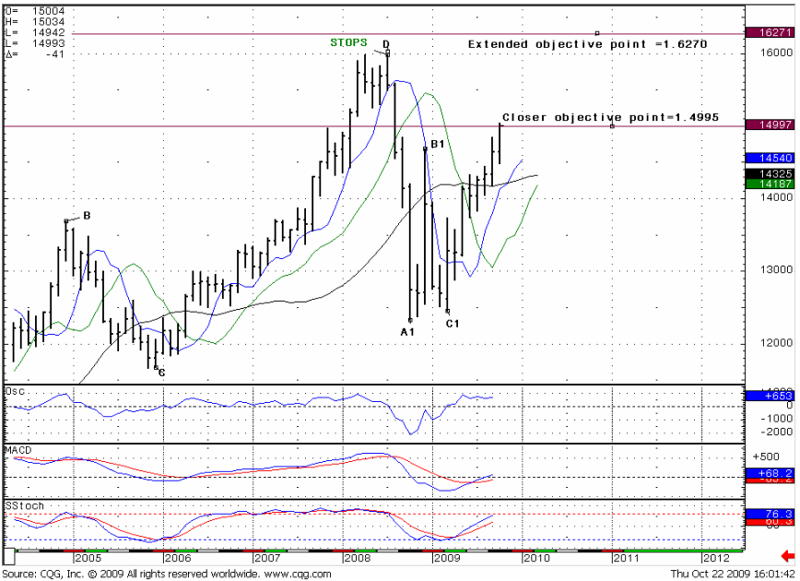

Monthly (EURO FX all sessions CME futures)

During October the market has reached an A1-B1-C1 objective point at 1.4817 and a C-D-A1 objective point at 1.5000 (That is more important). The monthly time frame is a long one, so we need to watch the behavior of the market around this level. Does it have power to go further? If not, we will not be able to see it during 1-2 months, we need at least 5-6 monthly bars to see any consolidation or reversal formation.

As for now, we have strong upside trend, no overbought still. According to my calculations of overbought level, the market will feel solid pressure if price reaches 1.52-1.5240 during the next week (the last week of the month by the way). This level is extreme overbought price for October.

So, for now we can discuss situation in a “when and if” way. If the market continues upside move, my next target is 1.6250, although probably the latest all-time high is more realistic. But think – there are a lot of stops here, and market-makers surely will want to touch them. If it happens, 1.6270 is a real target enough.

As for reverse way – I can’t tell anything, based on monthly chart. We just reach objective point at 1.5000 and that is important. There no signs of retracement yet. But again, we will see some signs first on the lower time frame charts.

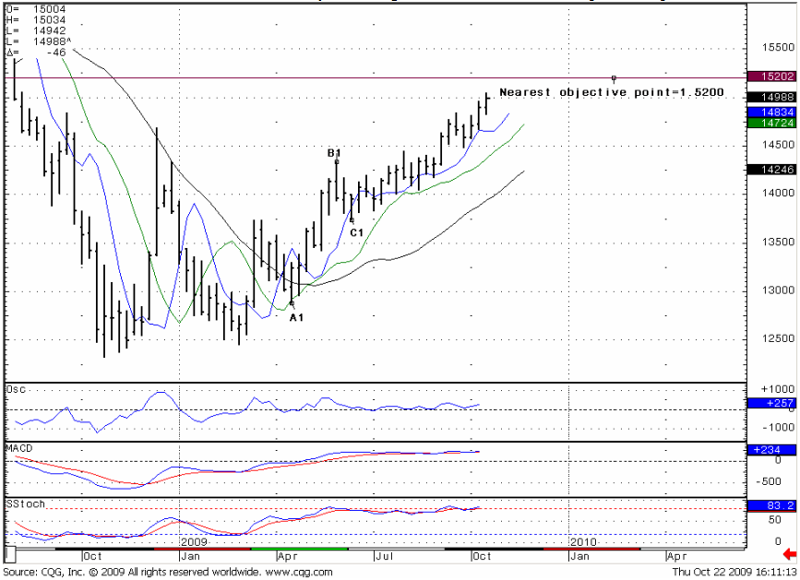

Weekly (EURO FX all sessions CME futures)

The picture is quite similar for weekly – strong upside trend, no overbought level. The nearest target of the next week is an objective point of A1-B1-C1 move – 1.5200. I think that this level can be reached during the next week. Besides, it coincides with the monthly overbought level. This can lead to a pause in any upside move.

Trade EUR/USD possibilities (1):

Monthly:

Momentum is up; extreme price for October is 1.52-1.5240 level. Possibly it can be reached.

Weekly:

The most important thing – market has reached monthly 1.50 target and stay now around it. For now there are still no signs of retracement. If it can go further on next week then the next target is 1.5200 that coincides with extreme overbought level. Retracement is much probable from the 1.5200 level.

(1) “Trade possibilities” are not detailed trade signals with specific entries and exits. They are expectations about possible moves of the market during the week based on market analysis.

<!-- AddThis Button BEGIN -->

<div class="addthis_toolbox addthis_default_style">

<a class="addthis_button_facebook"></a>

<a class="addthis_button_email"></a>

<a class="addthis_button_favorites"></a>

<a class="addthis_button_print"></a>

<span class="addthis_separator">|</span>

<a href="http://www.addthis.com/bookmark.php?v=250&pub=fb-promotion" class="addthis_button_expanded">More</a>

</div>

<script type="text/javascript" src="http://s7.addthis.com/js/250/addthis_widget.js?pub=fb-promotion"></script>

<!-- AddThis Button END -->

General Notice: Information has been obtained from sources believed to be reliable, but the author does not warrant its completeness or accuracy. Opinions and estimates constitute author’s judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this report must make their own independent decisions regarding any securities or financial instruments mentioned herein.