Sive Morten

Special Consultant to the FPA

- Messages

- 18,630

Fundamentals

Within just two weeks market sentiment and overall environment has changed drastically. The first bell was right after Thanksgiving when omicron has been detected. I already expressed my opinion that I see a lot of artificial things around it, and it it is too many coincidence around its appearing. But we should understand that people who support omicron panic, governments and central banks are from the same boat. All markets have tried to resist to this topic, standing near the tops for the two weeks, trying to return back, but it seems that it is not let to do. Bitcoin yesterday has dropped under 42K and this might be the beginning of massive sell-off in risky assets. Now we also see multiple signals from central banks that omicron is changing their view on the policy. Till the end of the year we could get big wave of news that could totally re-shape fundamental background. Such negative moments as inflation and supply chain problems could increase even further. This topic is so huge that we can't discuss all aspects even in the weekly report, but gradually we try to do this within few weeks.

Market overview

Commerzbank's head of FX and commodity research Ulrich Leuchtmann wrote in a client note that the euro had initially benefited from the Omicron variant because of the dovishness of the ECB.

Goldman Sachs said it would not change its economic forecasts on the basis of the Omicron variant until its likely impact became clearer.

Copper prices fell to a two-week low on Tuesday as worries about the damage to demand and economic growth from the Omicron coronavirus variant and monetary policy tightening in the United States weighed on sentiment.

Analysts say problems with shipping metal to consumers is partly behind shortages in some locations, including Europe and the United States. The main trucking lobbies in Canada and the United States are warning that vaccine and testing requirements for workers will further disrupt supply chains because there is already a dire shortage of drivers. More than two-thirds of goods traded between Canada and the United States travels on roads and highways. Motor carriers move 70% of all U.S. freight tonnage.

It estimates that 10-20%, or between 12,000-22,000 of Canadian truck drivers, and 40%, or some 16,000 of U.S. truck drivers traveling into Canada would be sidelined if the requirement begins.

Moderna's CEO said COVID-19 vaccines are unlikely to be as effective against the Omicron variant as they have been with other types. "There is no world, I think, where (the effectiveness) is the same level . . . we had with Delta," Moderna Chief Executive Stéphane Bancel told the Financial Times in an interview.

The euro surged on Tuesday and was on track for its biggest three-day rising streak this year, as traders cut their short positions on the single currency after Moderna's CEO said COVID-19 vaccines were unlikely to be as effective against the Omicron variant as they have been with other types.

Risk appetite took a battering across all markets for a second day in less than a week after his comments reinforced expectations that the global economy is set for a rocky and longer return to normalcy in the coming months. That was most evident in the jump in the value of the euro on Tuesday as traders rushed to cut their large short bets on the U.S. Federal Reserve raising interest rates quicker than its global peers next year.

Money markets pushed back their expectation of a first, full 25 basis-point rate hike to September 2022, versus July last week. Unwinding of popular carry trades in the currency markets was the theme in London trading, with the Aussie tanking 0.8% versus the Swiss currency while the franc held within striking distance of a July 2015 low against the euro.

The Australian and New Zealand dollars remained under pressure on Wednesday having hit their lowest levels of the year after the U.S. Federal Reserve flagged a quicker withdrawal of stimulus, while worries about the Omicron variant also weighed.

Against the backdrop of Omicron uncertainty and rising COVID-19 cases in Europe, the end of crisis-level interest rates in the United States looms even larger following hawkish comments from Federal Reserve Chair Jerome Powell overnight. The dollar index already logged its biggest monthly rise since June in November on the thinking that inflation could drive rates U.S. higher sooner rather than later.

It again leapt briefly and short-dated bonds and interest rate futures whipped lower after Powell told lawmakers it was time to retire his description of price pressures as transitory, and that policymakers would discuss a faster taper.

The dollar's rebound started as a report from the Institute for Supply Management came out showing that U.S. manufacturing activity picked up in November amid strong demand for goods, keeping inflation high as factories continued to struggle with pandemic-related shortages of raw materials.

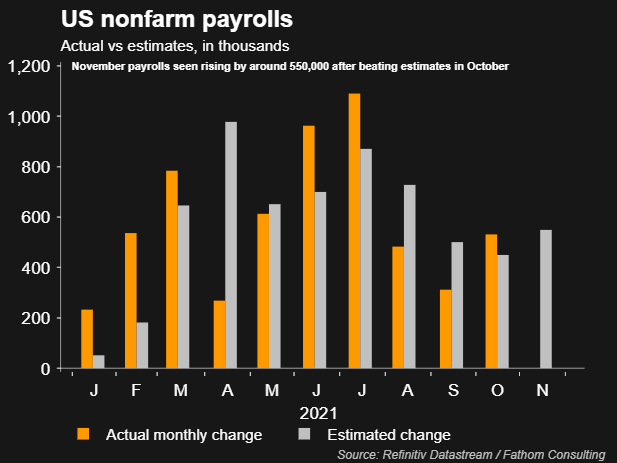

Nonfarm payrolls increased by 210,000 jobs last month, the Labor Department said, well below the 550,000 jobs economists polled by Reuters had forecast. The miss is significant because it comes even before the discovery of the new Omicron variant of the coronavirus which may further cloud the growth outlook. But the economy created 82,000 more jobs than initially reported in September and October, a sign of strength. That left employment 3.9 million jobs below the peak in February 2020.

U.S. Treasury yields tumbled on Friday in choppy trading, with the 10-year yield dropping below 1.4% for the first time since September as a risk-off sentiment took hold in markets, sending Wall Street lower.

Friday's labor report showed labor force participation rose to 61.8%, the highest since it fell off a cliff in the early days of the pandemic, and women - many of whom stayed home from jobs to fill in childcare, schooling and eldercare gaps - entered the labor force at the fastest rate since March.

Economists at Goldman Sachs noted following the report that the survey response rate that feeds into the payrolls number was the lowest for a November in 13 years. Several months this year have seen upward revisions in later readings, owing in part to the difficulty of data collection during the pandemic. From May through September, 748,000 more jobs were created than reported in the Labor Department's initial estimate.

CENTRAL BANKS REACTION ON OMICRON

The higher prices seen today are generally related to the pandemic, but some price increases are also being seen more broadly and the risk of higher inflation has increased, Federal Reserve Chair Jerome Powell said on Tuesday.

The Bank of Japan can hold off on expanding stimulus unless a spike in Omicron cases triggers huge market turbulence, board member Seiji Adachi said, suggesting policymakers will tread cautiously as they ascertain the risks posed by the variant. Adachi, a former economist considered as among those favoring aggressive monetary easing, also said inflationary pressures in Japan were not just being driven up by rising energy costs but also from changing corporate price-setting behavior.

Adachi shrugged off concern raised by some analysts that recent yen declines could push up import costs and lead to stagflation, where inflation accelerates even as the economy remains in bad shape.

Euro zone inflation remains temporary, two key European Central Bank policymakers argued on Thursday, even as U.S. officials made the case this week for abandoning the use of "transitory " to describe what have proven to be persistent price pressures. Inflation in the 19-country currency bloc hit a record high 4.9% last month and is likely to stay above the ECB's 2% target in 2022 but the bank has long argued that price pressure will abate on its own.

The debate is especially relevant as the ECB gears up for a crucial meeting on Dec. 16 when it is likely to end a pandemic emergency support scheme but may ramp up other support measures to pick up the slack.

Finnish central bank chief Olli Rehn sided with Panetta, specifically using the word "transitory" which U.S. Fed chief Jerome Powell said this week should be abandoned, although Rehn acknowledged inflation may take longer to come down than earlier thought.

The Omicron variant of COVID-19 could potentially prolong some of the supply chain challenges that heightened inflationary pressures during the pandemic and central banks need flexibility to address the uncertain landscape, a panel of economic experts said during the Reuters Next conference on Thursday.

Policymakers are aware that they could face substantial risks in financial markets, credit markets and in inflation if there is a negative reaction to a shift in monetary policy, said Jose Perez-Gorozpe, head of emerging markets credit research at S&P Global Ratings.

Several Federal Reserve officials have shared publicly that they are open to winding down their asset purchases more quickly so they can raise interest rates sooner if needed to address inflation, a topic that will be discussed during their Dec. 14-15 meeting.

Bank of England policymaker Michael Saunders, who voted for an interest rate hike last month, said on Friday he wanted more information about the impact of the new Omicron coronavirus variant before deciding how to vote this month. Investors were pricing in only a 33% chance of a December rate hike after the speech, down from about 75% last week before news broke of the new variant.

To be continued...

Within just two weeks market sentiment and overall environment has changed drastically. The first bell was right after Thanksgiving when omicron has been detected. I already expressed my opinion that I see a lot of artificial things around it, and it it is too many coincidence around its appearing. But we should understand that people who support omicron panic, governments and central banks are from the same boat. All markets have tried to resist to this topic, standing near the tops for the two weeks, trying to return back, but it seems that it is not let to do. Bitcoin yesterday has dropped under 42K and this might be the beginning of massive sell-off in risky assets. Now we also see multiple signals from central banks that omicron is changing their view on the policy. Till the end of the year we could get big wave of news that could totally re-shape fundamental background. Such negative moments as inflation and supply chain problems could increase even further. This topic is so huge that we can't discuss all aspects even in the weekly report, but gradually we try to do this within few weeks.

Market overview

"(Last) Friday's move was overdone, but the economic outlook is even more uncertain than it was a week ago," wrote Kit Juckes, head of FX strategy at Societe Generale, in a note to clients.

Commerzbank's head of FX and commodity research Ulrich Leuchtmann wrote in a client note that the euro had initially benefited from the Omicron variant because of the dovishness of the ECB.

"If Omicron leads to lockdowns and a renewed reduction in economic activity on a global scale all rate hike expectations turn out to be in vain and then they will be priced out again pretty quickly," he said. And which currencies will be the relative winners? Of course, the ones where rate hikes were never priced in very much in the first place. And those were EUR, JPY and CHF."

"Vaccine efficacy results with the next two weeks will be the most important headline to watch out for as well as whether symptoms are different from that of other variants," Nomura analyst Jordan Rochester said in a note to clients.

Goldman Sachs said it would not change its economic forecasts on the basis of the Omicron variant until its likely impact became clearer.

Copper prices fell to a two-week low on Tuesday as worries about the damage to demand and economic growth from the Omicron coronavirus variant and monetary policy tightening in the United States weighed on sentiment.

"While the severity of the new variant remains a big uncertainty, it casts a shadow over demand growth in the near future and further complicates the supply chain," said ING analyst Wenyu Yao.

Analysts say problems with shipping metal to consumers is partly behind shortages in some locations, including Europe and the United States. The main trucking lobbies in Canada and the United States are warning that vaccine and testing requirements for workers will further disrupt supply chains because there is already a dire shortage of drivers. More than two-thirds of goods traded between Canada and the United States travels on roads and highways. Motor carriers move 70% of all U.S. freight tonnage.

It estimates that 10-20%, or between 12,000-22,000 of Canadian truck drivers, and 40%, or some 16,000 of U.S. truck drivers traveling into Canada would be sidelined if the requirement begins.

"This is not a trucking issue. This is a Canada-U.S. economic issue," Laskowski told Reuters, adding about 70% of that C$650 billion ($507 billion) U.S.-Canada trade moves by truck.

"We'll be seeing shortages of goods in stores" if the vaccine requirement deadline is not delayed, said Perrin Beatty, president of the Canadian Chamber of Commerce.

Moderna's CEO said COVID-19 vaccines are unlikely to be as effective against the Omicron variant as they have been with other types. "There is no world, I think, where (the effectiveness) is the same level . . . we had with Delta," Moderna Chief Executive Stéphane Bancel told the Financial Times in an interview.

"Market participants’ fears over a more disruptive outcome for the global economy have been reinforced overnight by comments from Moderna Inc. CEO," Mizuho strategists said in client note.

The euro surged on Tuesday and was on track for its biggest three-day rising streak this year, as traders cut their short positions on the single currency after Moderna's CEO said COVID-19 vaccines were unlikely to be as effective against the Omicron variant as they have been with other types.

Risk appetite took a battering across all markets for a second day in less than a week after his comments reinforced expectations that the global economy is set for a rocky and longer return to normalcy in the coming months. That was most evident in the jump in the value of the euro on Tuesday as traders rushed to cut their large short bets on the U.S. Federal Reserve raising interest rates quicker than its global peers next year.

"This is Round 2 of Omicron jitters evident in the unwinding of short euro/long stock positions," said Kenneth Broux, an FX strategist at Societe Generale in London. There is an element of short euro covering as well and the unwinding of U.S. rate hike bets is also undermining the dollar."

Money markets pushed back their expectation of a first, full 25 basis-point rate hike to September 2022, versus July last week. Unwinding of popular carry trades in the currency markets was the theme in London trading, with the Aussie tanking 0.8% versus the Swiss currency while the franc held within striking distance of a July 2015 low against the euro.

The Australian and New Zealand dollars remained under pressure on Wednesday having hit their lowest levels of the year after the U.S. Federal Reserve flagged a quicker withdrawal of stimulus, while worries about the Omicron variant also weighed.

"Further market pricing for FOMC rate hikes and/or negative news about Omicron can push AUD/USD below 0.7000," analysts at Australia's top bank Commonwealth of Australia said in a note.

Against the backdrop of Omicron uncertainty and rising COVID-19 cases in Europe, the end of crisis-level interest rates in the United States looms even larger following hawkish comments from Federal Reserve Chair Jerome Powell overnight. The dollar index already logged its biggest monthly rise since June in November on the thinking that inflation could drive rates U.S. higher sooner rather than later.

It again leapt briefly and short-dated bonds and interest rate futures whipped lower after Powell told lawmakers it was time to retire his description of price pressures as transitory, and that policymakers would discuss a faster taper.

"His references to bringing the tapering schedule forward a few months sounded as if he sees the (Fed) thinking (it would conclude in) March or April rather than May or June," said Steve Englander, head of FX research at Standard Chartered in New York. For the dollar, the knee-jerk reaction to a more hawkish Fed is likely to be strength, but we are skeptical that this will persist if growth fears emerge," he added.

The dollar's rebound started as a report from the Institute for Supply Management came out showing that U.S. manufacturing activity picked up in November amid strong demand for goods, keeping inflation high as factories continued to struggle with pandemic-related shortages of raw materials.

Nonfarm payrolls increased by 210,000 jobs last month, the Labor Department said, well below the 550,000 jobs economists polled by Reuters had forecast. The miss is significant because it comes even before the discovery of the new Omicron variant of the coronavirus which may further cloud the growth outlook. But the economy created 82,000 more jobs than initially reported in September and October, a sign of strength. That left employment 3.9 million jobs below the peak in February 2020.

"The Fed will see the report as more than adequate to stay on course to accelerate tapering of asset purchases at the December meeting, implying an end to purchases in March," said Andrew Hollenhorst, chief U.S. economist at Citigroup in New York. "Moreover, an unemployment rate that is poised to fall below 4.0% perhaps in the coming months keeps a first Fed rate hike in June or even earlier firmly on the table."

"On the surface, the numbers came in disappointing because they did not match expectations, but it was not a weak report," said Kevin Flanagan, head of fixed income strategy at WisdomTree Investments.

U.S. Treasury yields tumbled on Friday in choppy trading, with the 10-year yield dropping below 1.4% for the first time since September as a risk-off sentiment took hold in markets, sending Wall Street lower.

"There definitely is a broader risk-off tone. Stocks are going down led by high-beta names," said Tom Simons, a money market economist at Jefferies in New York.

Friday's labor report showed labor force participation rose to 61.8%, the highest since it fell off a cliff in the early days of the pandemic, and women - many of whom stayed home from jobs to fill in childcare, schooling and eldercare gaps - entered the labor force at the fastest rate since March.

"We think the Fed will view the economy as near full employment," Barclays economists wrote in a note, adding that not only do they expect the central bank to speed up its taper in December, but also to begin raising rates in March.

Economists at Goldman Sachs noted following the report that the survey response rate that feeds into the payrolls number was the lowest for a November in 13 years. Several months this year have seen upward revisions in later readings, owing in part to the difficulty of data collection during the pandemic. From May through September, 748,000 more jobs were created than reported in the Labor Department's initial estimate.

"We think that it is clear that QE has overstayed its welcome," Blackrock chief investment officer Rick Rieder wrote in a note to investors, but added, "the next few months will be fertile with information on Omicron risks, supply and demand influences, a potentially moderately slowing demand for goods and services, having moved further from the immense fiscal and monetary stimulus, and the potential alleviation of some of the supply-chain pressures that have pressed prices higher."

CENTRAL BANKS REACTION ON OMICRON

The higher prices seen today are generally related to the pandemic, but some price increases are also being seen more broadly and the risk of higher inflation has increased, Federal Reserve Chair Jerome Powell said on Tuesday.

"Generally, the higher prices we're seeing are related to the supply and demand imbalances that can be traced directly back to the pandemic and the reopening of the economy," Powell said during a hearing with the U.S. Senate Banking Committee. "But it's also the case that price increases have spread much more broadly ... and I think the risk of higher inflation has increased."

"We've gotten these conflicting claims about the new variant, and Powell's comments really threw the markets for a loop," said Marc Chandler, chief market strategist at Bannockburn Global Forex. "People are still pretty nervous," Chandler said.

The Bank of Japan can hold off on expanding stimulus unless a spike in Omicron cases triggers huge market turbulence, board member Seiji Adachi said, suggesting policymakers will tread cautiously as they ascertain the risks posed by the variant. Adachi, a former economist considered as among those favoring aggressive monetary easing, also said inflationary pressures in Japan were not just being driven up by rising energy costs but also from changing corporate price-setting behavior.

"The BOJ must consider taking additional easing steps only if developments surrounding the pandemic lead to a yen spike and stock price fall, and when such market conditions persist," Adachi told a briefing.

Adachi shrugged off concern raised by some analysts that recent yen declines could push up import costs and lead to stagflation, where inflation accelerates even as the economy remains in bad shape.

"Personally, I don't think Japan is facing a 'bad weak yen' that could lead to stagflation," Adachi said. The yen's recent fall actually is bringing benefits to the economy" by boosting profits Japanese firms reap overseas, he added.

Euro zone inflation remains temporary, two key European Central Bank policymakers argued on Thursday, even as U.S. officials made the case this week for abandoning the use of "transitory " to describe what have proven to be persistent price pressures. Inflation in the 19-country currency bloc hit a record high 4.9% last month and is likely to stay above the ECB's 2% target in 2022 but the bank has long argued that price pressure will abate on its own.

"The current inflation spike is temporary and driven largely by supply factors," ECB board member Fabio Panetta told a conference. "Central banks should have the patience to look through these effects and explain their policies to the people."

The debate is especially relevant as the ECB gears up for a crucial meeting on Dec. 16 when it is likely to end a pandemic emergency support scheme but may ramp up other support measures to pick up the slack.

Finnish central bank chief Olli Rehn sided with Panetta, specifically using the word "transitory" which U.S. Fed chief Jerome Powell said this week should be abandoned, although Rehn acknowledged inflation may take longer to come down than earlier thought.

"I do recognize that the micro experience of our citizens at the fuel pump is quite difference from the macro reading of economists and central bankers," Rehn told the same conference. "Still, in our view, euro area inflation is mostly transitory... even if some of its components will probably prevail longer over the next year than previously expected," he added.

The Omicron variant of COVID-19 could potentially prolong some of the supply chain challenges that heightened inflationary pressures during the pandemic and central banks need flexibility to address the uncertain landscape, a panel of economic experts said during the Reuters Next conference on Thursday.

"On the supply side, it means the inflationary pressures will probably persist even longer," said Kristin Forbes, an economics professor with the Sloan School of Management at MIT. "And given how tight everything is right now, that could mean some notable increases in inflation ... due to supply side constraints."

Policymakers are aware that they could face substantial risks in financial markets, credit markets and in inflation if there is a negative reaction to a shift in monetary policy, said Jose Perez-Gorozpe, head of emerging markets credit research at S&P Global Ratings.

Several Federal Reserve officials have shared publicly that they are open to winding down their asset purchases more quickly so they can raise interest rates sooner if needed to address inflation, a topic that will be discussed during their Dec. 14-15 meeting.

Bank of England policymaker Michael Saunders, who voted for an interest rate hike last month, said on Friday he wanted more information about the impact of the new Omicron coronavirus variant before deciding how to vote this month. Investors were pricing in only a 33% chance of a December rate hike after the speech, down from about 75% last week before news broke of the new variant.

"At present, given the new Omicron COVID variant has only been detected quite recently, there could be particular advantages in waiting to see more evidence on its possible effects on public health outcomes and hence on the economy," Saunders said in a speech. This could require a more abrupt and painful policy tightening later," Saunders said. "For me, the balance between these considerations is likely to be a key factor at the December meeting."

To be continued...