Sive Morten

Special Consultant to the FPA

- Messages

- 18,659

Fundamentals

So, another week of new inflationary environment is passed. Market was keeping the same direction as it was set after stunning inflation data last week. With good US Retail Sales release, the USD power is increased. Now all eyes are on coming Fed meeting minutes and December meeting. Initially it was suggested that hardly next meeting becomes decisive but, with new inflationary sentiment, Fed could adjust its vision on the future and on its policy. Another moment that fear is coming slowly on the markets. Stock investors are reduce their portfolios, while big banks expect humble return in next year. Big bond trading funds start to see signs of the bubble.

Market overview

The dollar was set to post a second week of chunky gains against the euro on Friday as traders wager on interest rates rising faster and further on the North Atlantic's western shore, while sterling and the kiwi have also firmed with rate hike bets.

This week U.S. retail sales beat expectations on the heels of last week's inflation surprise. In Europe, meanwhile, COVID-19 is surging again, car sales slipped for a fourth consecutive month and central bankers are vowing to hold rates low.

President Joe Biden's $1.75 trillion bill to bolster the social safety net and fight climate change passed the U.S. House of Representatives on Friday and headed to the Senate, where divided moderates and liberals still need to reach agreement.

Senate Democrats hope to reach agreement by the end of December with centrist Democrats Joe Manchin and Kyrsten Sinema, who have raised concerns about the bill's size and some of its provisions.

The talking down of speeding inflation as a temporary phenomenon by many central banks poses risks of a more intense monetary adjustment at a later date than would otherwise be needed, Credit Suisse Chairman Antonio Horta-Osorio said.

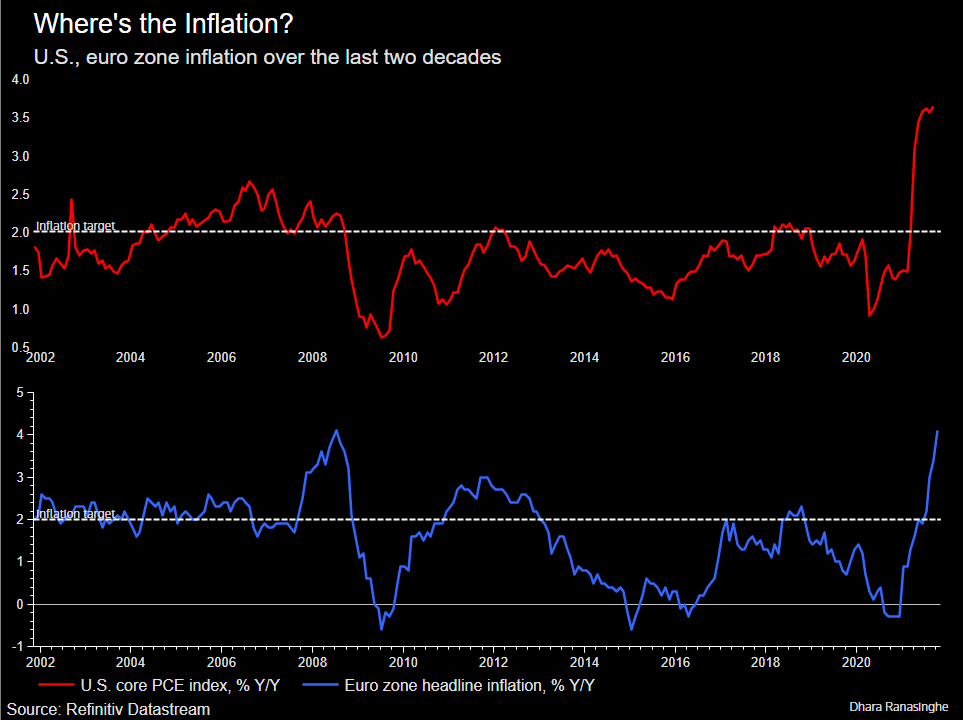

The U.S. Federal Reserve adopted in 2020 a flexible average inflation target (FAIT) designed to be more forgiving of price pressures than before, a major shift in the Fed's dual approach towards achieving maximum employment and stable prices. The European Central Bank followed this year, setting a 2% medium-term inflation target and ditching its long-established "below but close to 2%" goal. Although both dismiss current price pressures as "transitory", they are facing the first real test of these new frameworks.

Euro area annual inflation is above 4%, while the U.S. consumer price index exceeded 6% last month, stoked by supply bottlenecks and red-hot commodity prices.

PIMCO expects that "in Europe, supply chain breakdowns have contributed to deceleration in the Industrial Production measure and an acceleration in headline CPI. Volatility will likely remain elevated in the months ahead, with inflation expected to peak at close to double the European Central Bank’s (ECB) target, and then start to normalize – conditional on energy impacts weakening and a mild winter. ECB President Christine Lagarde recently acknowledged that rate hikes are very unlikely in the next year."

While central banks cannot control such factors, they often act early to ensure consumers' expectations of future inflation do not translate into significantly higher wages. At the ECB, a move may not come for years.

Bubble warnings are ringing louder after a week of dovish central bank bombshells fueled the easiest financial conditions in nearly four decades.

BlackRock Inc.’s Rick Rieder and Allianz SE’s Mohamed El-Erian are among those warning that systemic risks will only multiply, unless monetary officials take more decisive measures to pare extraordinary pandemic stimulus. While policy makers are acutely aware of the dangers in the easy-money era, their accommodative stances are encouraging ever-increasing flows to the riskiest markets.

The crypto industry just hit over $3 trillion in value, the biggest junk bond exchange-traded fund is booming after getting the most cash since March, and major stock indexes are sitting near records. No wonder a cross-asset gauge shows the easy U.S. investing climate is one for the history books.

The risk binge is intensifying worries over market froth and lax central bank watchdogs. The world’s biggest, the Federal Reserve, signaled last week a delay in interest-rate increases until the labor market is in better shape after it announced a widely expected reduction in asset purchases.

Last week the Bank of England shocked markets with a decision not to raise rates. Meanwhile European Central Bank President Christine Lagarde pushed back against wagers on a rate hike in 2022.

With supply-side pressures threatening growth, central bankers risk either acting too fast and derailing recoveries or being too slow and letting inflation get out of control. Officials are therefore taking a measured approach, despite some investors pressing for a more decisive end to pandemic stimulus.

US "Inflation - Jobs" balance

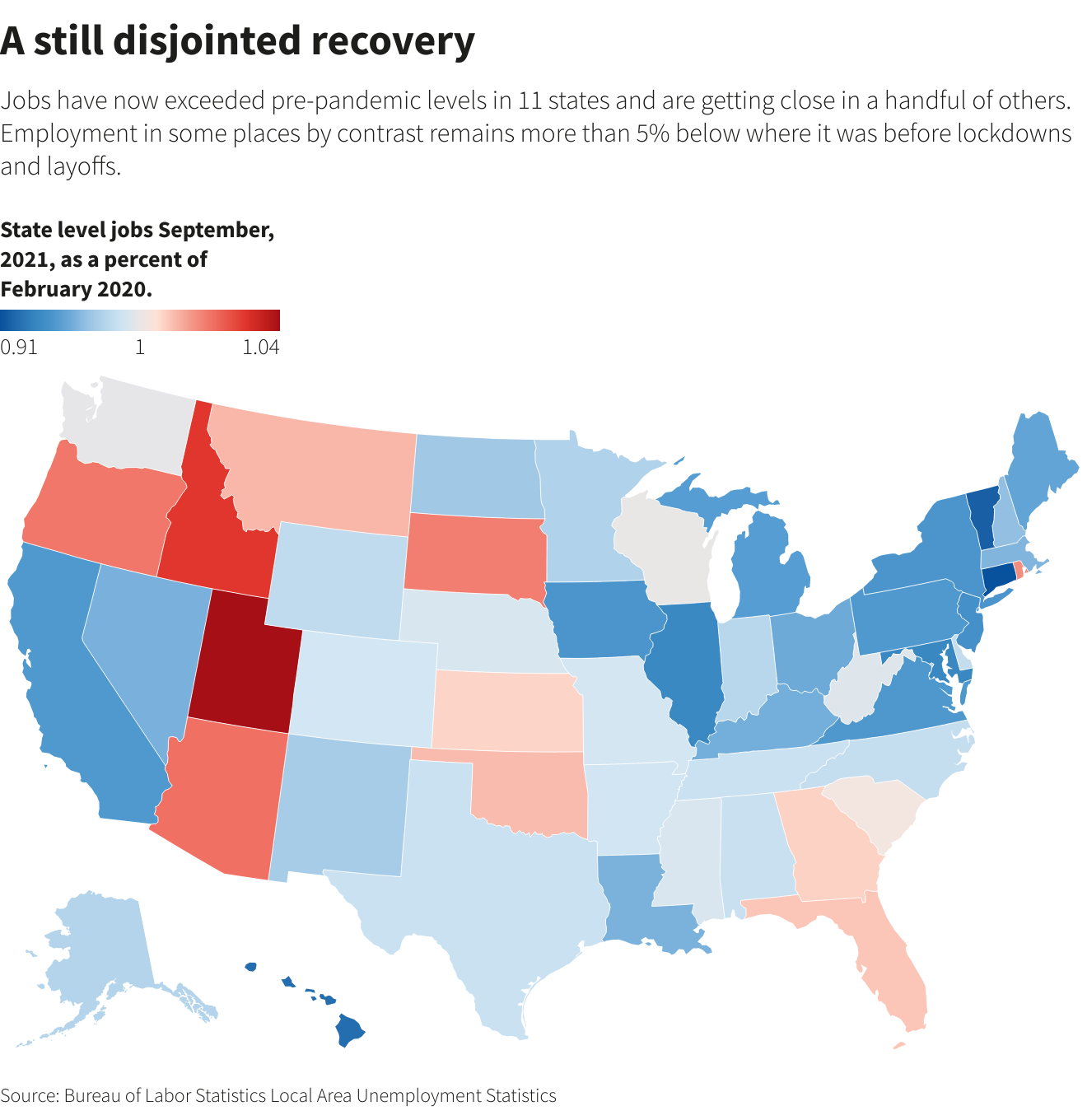

Hopes to restore U.S. employment to its pre-pandemic level, an aim of the Federal Reserve and the Biden administration, now rest on a recovery of jobs in New England and California. Data released on Friday show that through October employment in states with Republican governors was close to 99% of what it was in February of 2020, while Democratic-led states lagged, at roughly 96%.

While state-level estimates can be volatile, particularly month to month, the apparently larger remaining job shortfall in Democratic-leaning areas echoes the choices - and political divisions - that emerged early in the pandemic.

Recovery has come faster than many expected, but it remains uneven. Of 10 states that had more jobs in October of this year than in February 2020, seven had Republican governors and another six GOP-led states were within 1 percentage point of their pre-pandemic job level.

The level of jobs alone doesn't tell the full story, and on key measures like the overall employment-to-population ratio - considered a more complete measure of job market health than the unemployment rate - Republican strongholds like Texas and Florida remained well below levels seen before the pandemic crisis.

Until recently it seemed the Fed was intent on keeping monetary policy loose and borrowing costs easy for as long as it took to claw those jobs back. That aim may now be in conflict with the Fed's other goal of stable prices, challenged by a run of inflation that is prompting central bank policymakers to discuss a faster move to tighter policy - which could slow job growth before areas central to Biden's political chances are able to catch up.

Federal Reserve policymakers are publicly debating whether to withdraw support for the U.S. economy more quickly to deal with surging inflation, with one of the central bank's most influential officials signaling on Friday that the idea will be on the table at the Fed's next meeting. Since the previous meeting, the economy has gained speed, with reports showing more than half a million jobs added in October, retail sales surging, and consumer inflation notching its biggest annual increase in 31 years.

Earlier Friday, Fed Governor Christopher Waller called for a the Fed to double up on its wind-down of bond purchases, finishing it by April to make way for a possible interest-rate hike in the second quarter of next year.

Waller and St. Louis Fed President James Bullard, who earlier this week called for the Fed to end its bond purchases by March, have been at the forefront of policymakers pushing for an accelerated timeline for tightening.

After his remarks, interest-rate futures trading reflected rising bets that the Fed will begin to raise rates by June and lift them twice more by the end of the year. There is still no consensus within the Fed to quicken the taper.

Separately, Atlanta Federal Reserve President Raphael Bostic said Thursday he believes the U.S. central bank could start raising interest rates by the middle of next year, based on his outlook that the economy will be back to full employment by then. The tension over Fed policy comes as President Joe Biden nears a decision on whether to keep Jerome Powell as Fed chair for another term, or to elevate Governor Lael Brainard to the position. A decision is expected by Thanksgiving.

COT Report

The table below stands for the beginning of this week, and mostly reflects that big shift in sentiment due recent inflation, consumption and other US statistics. Currently we see just the initial reaction and it is mostly speculative. It is definitely bearish but take a look - the major change stands in non-commercial part, which means speculators. While among "commercials", i.e. hedgers we do not see clear tendency as positions were opened in both direction. Overall reaction provides the power for further downside action but it is important to see changes in hedgers' positions within coming few weeks as well. This just gives more confidence with new tendency that we have on the market.

Next week to watch

#1 Fed minutes release

Minutes from the Federal Reserve's November meeting on Wednesday should provide clues on its take on inflation. U.S. consumer prices rising at the fastest pace in more than three decades in October and accelerating inflation expectations have lifted expectations that the Fed will need to speed up tapering of asset purchases and hike rates faster-than-expected.

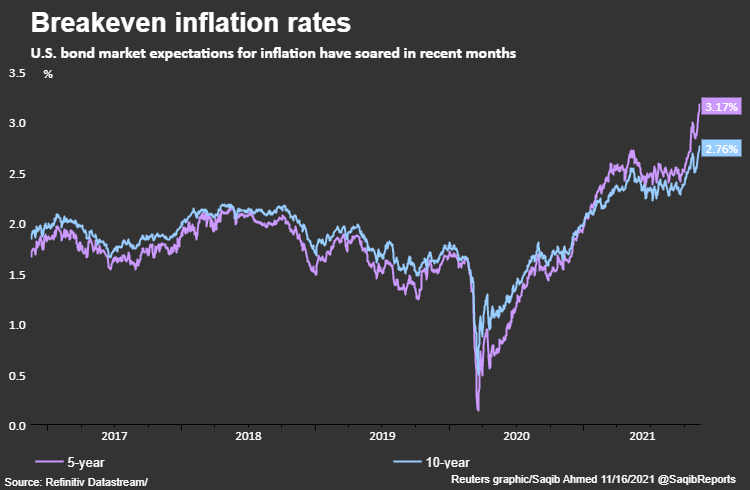

The 5-year and 10-year breakeven rate - the yield spread between inflation protected and normal Treasuries - stand at record highs. More fodder comes from Wednesday's reading of the October personal consumption expenditures (PCE) price index - the Fed’s preferred inflation gauge - expected to rise to 0.4%, according to a Reuters poll.

# 2 PMI release

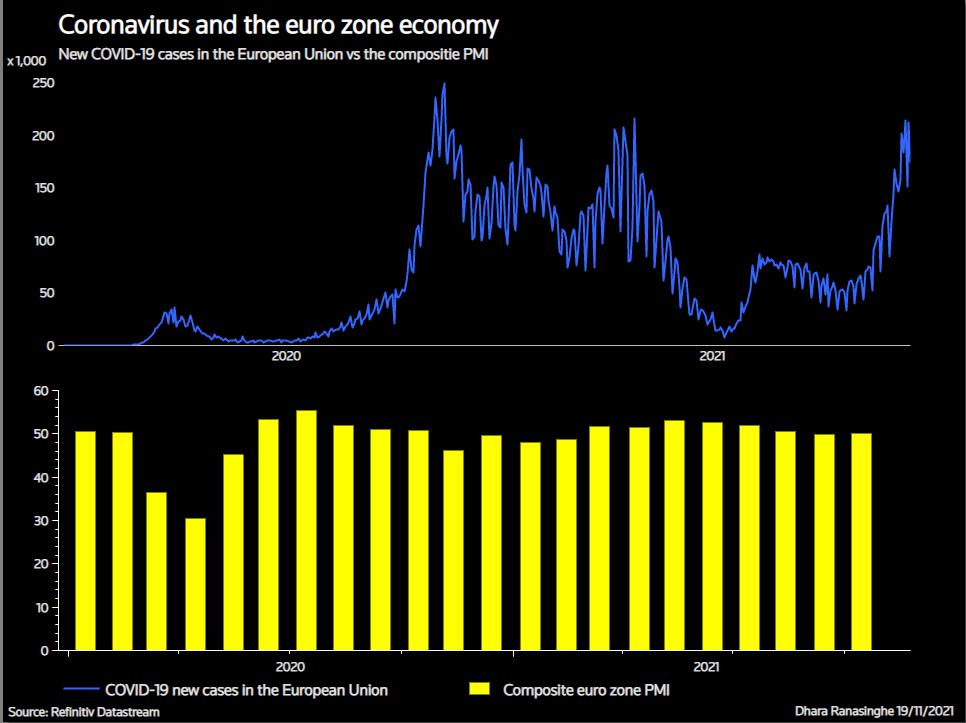

The flash November purchasing managers' index (PMI), a key forward looking economic indicator, is due out from a host of major economies in coming days -- the United States, Australia, Britain and the euro area.

Market focus is on what impact price pressures and supply bottlenecks are having on business activity and whether these are abating. Euro area PMIs, which have held up well, could provide a sense of what toll a resurgent COVID-19 is taking.

Germany's Angela Merkel warns the coronavirus situation in the powerhouse economy is dramatic, the Netherlands is in partial lockdown and pressure is mounting on Austria to do more. But vaccine rollouts and the reassuring - and hefty - presence of ECB stimulus ease some of those worries.

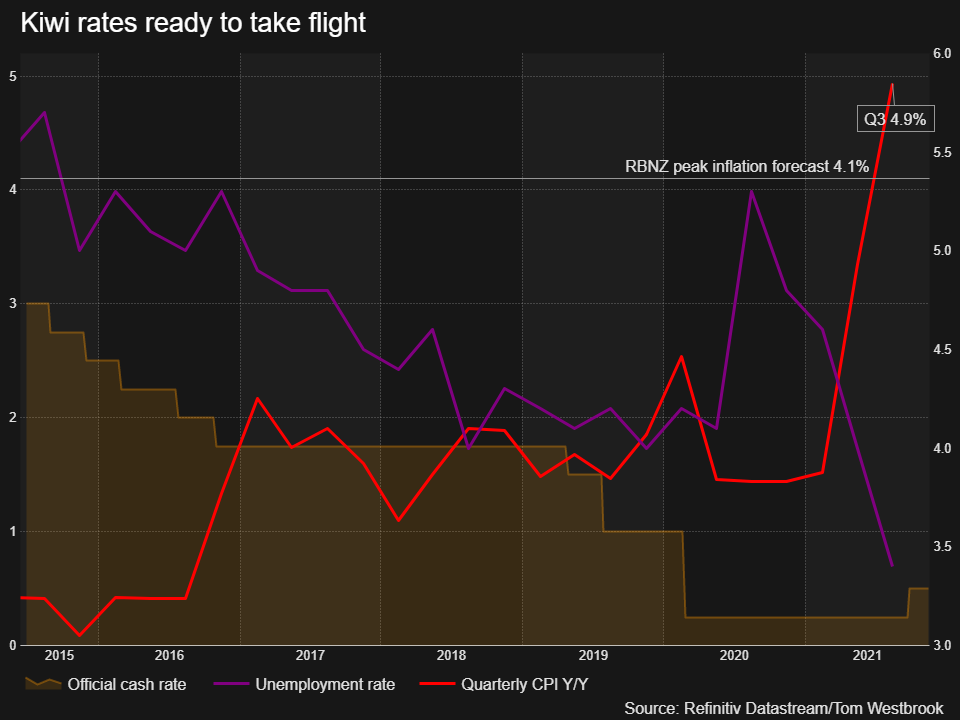

#3 RBNZ meeting

The Reserve Bank of New Zealand is expected to move deeper into the vanguard of inflation fighters on Wednesday, and deliver a second rate hike in as many months. Since October, when the RBNZ joined Norway as developed markets' first hikers, inflation has surged to a decade high and the unemployment rate has sunk to record lows.

Traders are sure rates will go up, and are focused on two hawkish risks: A roughly 40% chance that the hike is a chunky 50 bps one, and the bank lifts its long-term rates outlook. Either could hoist the kiwi higher, though both bring risks to local borrowers already squeezed by the fastest pace of mortgage rate rises in 15 years.

Conclusion

This week brings no big shifts in overall sentiment. Technical picture has not changed either as EUR has dropped more and comes close to major weekly support area. Overall market consensus stands in favor of longer period of high inflation that should furlong into 1Q of 2022 and start to normalize after. At least, this is common suggestion right now. Fed minutes hardly could make strong impact as meeting was prior the decisive CPI data release. Until December meeting pressure should grow as coming PCE, NFP wage data and PPI/CPI in the beginning of December should creep even higher, as it is widely suggested. All these aspects warm up US Dollar demand and push Fed to more aggressive steps, at least in tapering process. As a secondary factor we could point on some geopolitical affairs in Eastern Europe and Taiwan that also indirectly support dollar demand.

The fact that the US has printed another 3% Global GDP (1 Trln approved pack and new 1.75 Trln that has passed the Congress) only rises the inflation expectations. This is background explains why we do not see any reasons to change our mid term view on EUR/USD. Also we see signs that supply chains' bottlenecks are forming artificially as well as gas price rally to dump China and EU economies. But this is too wide subject for discussion here in details.

Technicals

Monthly

On monthly time frame everything remains the same, as market confirms our plan and keep going lower. Downside tendency has good momentum with multiple tail closed months, including November by far.

In general, currently trend stands bearish. Once market hits all-time OP around 1.06 area it turns to consolidation that now is taking the shape of extended triangle. Last week we've considered upside scenario based on potential change in long-term sentiment of major Central Banks, but now, in the light of recent events, we leave this scenario for now. As price breaks minor pennant, forming bearish reversal action in September, and dropping below YPP - the nearest target stands around 1.10-1.12 area. The same target is mentioned above by Société Générale. Here is we have monthly COP, YPS1 and trend line support, while on weekly and daily time frames some other objects exist in this area. For now, the reaching of this area seems probable as it is not big distance till this level.

As market is not at oversold here and target is not hit yet, we expect downside continuation within few weeks with minor local breaks for retracements.

Weekly

This week market has made big step toward our major destination point here which is Agreement of XOP 1.1220 target and major 1.1290 Fib support. We do not expect the pullback until market hits XOP level, despite it stands oversold right now. This week you could see that upside reaction is muted and market turns down again as soon as possible. So, we do not consider any long positions on daily/intraday charts, until XOP is hit.

Daily

So, market fills the trading plan pretty accurately this time. Downside action starts right from pre-defined intraday K-area. As you can see, despite oversold level, upward bounce was just minor harmonic swing. Now market stands not too far from weekly XOP, which is around 1.1218-1.1220 area. The first sign that we get upside reaction should be appearing of some bullish pattern on daily/ 4H time frame. Currently is nothing to do on daily chart as market stands near support area. Until XOP is hit and bullish pattern is formed we could consider setups only on intraday charts.

Intraday

The general idea, when market tends to major target and stands at oversold on weekly chart is to take scalp short positions and out at around recent lows. This setup could repeat few times, until price hits weekly XOP.

Of course, market could keep going lower, directly to XOP. In this case we just do not get trading setup at all. In a case of pullback though, we could watch for something like that - "222" Sell" around some resistance level.

So, another week of new inflationary environment is passed. Market was keeping the same direction as it was set after stunning inflation data last week. With good US Retail Sales release, the USD power is increased. Now all eyes are on coming Fed meeting minutes and December meeting. Initially it was suggested that hardly next meeting becomes decisive but, with new inflationary sentiment, Fed could adjust its vision on the future and on its policy. Another moment that fear is coming slowly on the markets. Stock investors are reduce their portfolios, while big banks expect humble return in next year. Big bond trading funds start to see signs of the bubble.

Market overview

The dollar was set to post a second week of chunky gains against the euro on Friday as traders wager on interest rates rising faster and further on the North Atlantic's western shore, while sterling and the kiwi have also firmed with rate hike bets.

"Previous post-GFC occasions when the euro traded below $1.10 were accompanied by a big euro short position," said Societe Generale strategist Kit Juckes. If the question is 'will the market now get very short euros' then I think the answer is that it will unless data improve dramatically."

This week U.S. retail sales beat expectations on the heels of last week's inflation surprise. In Europe, meanwhile, COVID-19 is surging again, car sales slipped for a fourth consecutive month and central bankers are vowing to hold rates low.

President Joe Biden's $1.75 trillion bill to bolster the social safety net and fight climate change passed the U.S. House of Representatives on Friday and headed to the Senate, where divided moderates and liberals still need to reach agreement.

"Now, the Build Back Better Act goes to the United States Senate, where I look forward to it passing as soon as possible so I can sign it into law," Biden said in a statement following the vote.

Senate Democrats hope to reach agreement by the end of December with centrist Democrats Joe Manchin and Kyrsten Sinema, who have raised concerns about the bill's size and some of its provisions.

The talking down of speeding inflation as a temporary phenomenon by many central banks poses risks of a more intense monetary adjustment at a later date than would otherwise be needed, Credit Suisse Chairman Antonio Horta-Osorio said.

"Markets have been giving a lot of credit to central banks... but the latest indicators are that the temporary is perhaps less temporary," he told a banking conference in Lisbon, calling the central banks' discourse "somewhat courageous". The risk for central banks here is that if inflation proves not to be temporary, it could trigger a much more intense monetary adjustment than would otherwise be necessary," the Portuguese former Lloyds Bank chief executive added.

The U.S. Federal Reserve adopted in 2020 a flexible average inflation target (FAIT) designed to be more forgiving of price pressures than before, a major shift in the Fed's dual approach towards achieving maximum employment and stable prices. The European Central Bank followed this year, setting a 2% medium-term inflation target and ditching its long-established "below but close to 2%" goal. Although both dismiss current price pressures as "transitory", they are facing the first real test of these new frameworks.

Euro area annual inflation is above 4%, while the U.S. consumer price index exceeded 6% last month, stoked by supply bottlenecks and red-hot commodity prices.

PIMCO expects that "in Europe, supply chain breakdowns have contributed to deceleration in the Industrial Production measure and an acceleration in headline CPI. Volatility will likely remain elevated in the months ahead, with inflation expected to peak at close to double the European Central Bank’s (ECB) target, and then start to normalize – conditional on energy impacts weakening and a mild winter. ECB President Christine Lagarde recently acknowledged that rate hikes are very unlikely in the next year."

"In the U.S., our base case is for headline CPI inflation to peak around year-end and into Q1 2022, and remain elevated through Q3 2022 when some moderation is likely as the handoff from goods to services consumption returns to more normal levels. However, consensus inflation forecasts have been playing catch up with inflation, signaling that risks to the base case skew to the upside"

Inflation expectations, both market and survey-based, have been trending higher. Even though they remain generally contained, risks to the upside have risen, given stubbornly high inflation data and inflationary pressures. Simultaneously, central bankers’ confidence in labor slack has been a key factor in their patient approach to policy. As the employment gap narrows and closes in many regions, as we expect, the path of wages and the ability of individuals to bargain for higher wages to keep up with mounting price pressures will be critical assessments in forecasting inflation, and could be a game changer for inflation expectations.

While central banks cannot control such factors, they often act early to ensure consumers' expectations of future inflation do not translate into significantly higher wages. At the ECB, a move may not come for years.

If the ECB does raise rates next year, it would violate its guidance or mean that inflation has busted all forecasts, BofA analysts note.

Bubble warnings are ringing louder after a week of dovish central bank bombshells fueled the easiest financial conditions in nearly four decades.

BlackRock Inc.’s Rick Rieder and Allianz SE’s Mohamed El-Erian are among those warning that systemic risks will only multiply, unless monetary officials take more decisive measures to pare extraordinary pandemic stimulus. While policy makers are acutely aware of the dangers in the easy-money era, their accommodative stances are encouraging ever-increasing flows to the riskiest markets.

The crypto industry just hit over $3 trillion in value, the biggest junk bond exchange-traded fund is booming after getting the most cash since March, and major stock indexes are sitting near records. No wonder a cross-asset gauge shows the easy U.S. investing climate is one for the history books.

The risk binge is intensifying worries over market froth and lax central bank watchdogs. The world’s biggest, the Federal Reserve, signaled last week a delay in interest-rate increases until the labor market is in better shape after it announced a widely expected reduction in asset purchases.

“The risk is you’re creating overheating prices,” Rieder, BlackRock’s CIO of global fixed income, told Bloomberg TV on Friday. “The risk to the system is you get too much liquidity in the system creating excess. At the same time while policy makers have been slow to turn off the liquidity hose, they’re at least making a start, said Rieder. Could they do it a bit faster? Yeah I think so,” he said. “But at least the door is open and we’re moving in the right direction.”

Last week the Bank of England shocked markets with a decision not to raise rates. Meanwhile European Central Bank President Christine Lagarde pushed back against wagers on a rate hike in 2022.

With supply-side pressures threatening growth, central bankers risk either acting too fast and derailing recoveries or being too slow and letting inflation get out of control. Officials are therefore taking a measured approach, despite some investors pressing for a more decisive end to pandemic stimulus.

“It’s not clear to me why we need to continue to run monetary policy so hot,” El-Erian, a Bloomberg Opinion columnist, said on Bloomberg TV on Friday. “The economy is doing just fine. But the collateral damage it’s creating, the unintended consequences that are resulting, are spreading. This is a Fed that’s going to wait and I fear is going to fall behind and we risk a pretty big policy mistake.”

US "Inflation - Jobs" balance

Hopes to restore U.S. employment to its pre-pandemic level, an aim of the Federal Reserve and the Biden administration, now rest on a recovery of jobs in New England and California. Data released on Friday show that through October employment in states with Republican governors was close to 99% of what it was in February of 2020, while Democratic-led states lagged, at roughly 96%.

While state-level estimates can be volatile, particularly month to month, the apparently larger remaining job shortfall in Democratic-leaning areas echoes the choices - and political divisions - that emerged early in the pandemic.

Recovery has come faster than many expected, but it remains uneven. Of 10 states that had more jobs in October of this year than in February 2020, seven had Republican governors and another six GOP-led states were within 1 percentage point of their pre-pandemic job level.

The level of jobs alone doesn't tell the full story, and on key measures like the overall employment-to-population ratio - considered a more complete measure of job market health than the unemployment rate - Republican strongholds like Texas and Florida remained well below levels seen before the pandemic crisis.

Until recently it seemed the Fed was intent on keeping monetary policy loose and borrowing costs easy for as long as it took to claw those jobs back. That aim may now be in conflict with the Fed's other goal of stable prices, challenged by a run of inflation that is prompting central bank policymakers to discuss a faster move to tighter policy - which could slow job growth before areas central to Biden's political chances are able to catch up.

Federal Reserve policymakers are publicly debating whether to withdraw support for the U.S. economy more quickly to deal with surging inflation, with one of the central bank's most influential officials signaling on Friday that the idea will be on the table at the Fed's next meeting. Since the previous meeting, the economy has gained speed, with reports showing more than half a million jobs added in October, retail sales surging, and consumer inflation notching its biggest annual increase in 31 years.

Earlier Friday, Fed Governor Christopher Waller called for a the Fed to double up on its wind-down of bond purchases, finishing it by April to make way for a possible interest-rate hike in the second quarter of next year.

"The rapid improvement in the labor market and the deteriorating inflation data have pushed me towards favoring a faster pace of tapering and a more rapid removal of accommodation in 2022," Waller said at the Center for Financial Stability in New York. All shocks tend to be transitory and fade away. By this logic the Fed should never respond to any shocks, but sometimes it does, as it should... appropriate monetary policy responds to these inflation movements," Waller added.

Waller and St. Louis Fed President James Bullard, who earlier this week called for the Fed to end its bond purchases by March, have been at the forefront of policymakers pushing for an accelerated timeline for tightening.

After his remarks, interest-rate futures trading reflected rising bets that the Fed will begin to raise rates by June and lift them twice more by the end of the year. There is still no consensus within the Fed to quicken the taper.

Separately, Atlanta Federal Reserve President Raphael Bostic said Thursday he believes the U.S. central bank could start raising interest rates by the middle of next year, based on his outlook that the economy will be back to full employment by then. The tension over Fed policy comes as President Joe Biden nears a decision on whether to keep Jerome Powell as Fed chair for another term, or to elevate Governor Lael Brainard to the position. A decision is expected by Thanksgiving.

COT Report

The table below stands for the beginning of this week, and mostly reflects that big shift in sentiment due recent inflation, consumption and other US statistics. Currently we see just the initial reaction and it is mostly speculative. It is definitely bearish but take a look - the major change stands in non-commercial part, which means speculators. While among "commercials", i.e. hedgers we do not see clear tendency as positions were opened in both direction. Overall reaction provides the power for further downside action but it is important to see changes in hedgers' positions within coming few weeks as well. This just gives more confidence with new tendency that we have on the market.

Next week to watch

#1 Fed minutes release

Minutes from the Federal Reserve's November meeting on Wednesday should provide clues on its take on inflation. U.S. consumer prices rising at the fastest pace in more than three decades in October and accelerating inflation expectations have lifted expectations that the Fed will need to speed up tapering of asset purchases and hike rates faster-than-expected.

The 5-year and 10-year breakeven rate - the yield spread between inflation protected and normal Treasuries - stand at record highs. More fodder comes from Wednesday's reading of the October personal consumption expenditures (PCE) price index - the Fed’s preferred inflation gauge - expected to rise to 0.4%, according to a Reuters poll.

# 2 PMI release

The flash November purchasing managers' index (PMI), a key forward looking economic indicator, is due out from a host of major economies in coming days -- the United States, Australia, Britain and the euro area.

Market focus is on what impact price pressures and supply bottlenecks are having on business activity and whether these are abating. Euro area PMIs, which have held up well, could provide a sense of what toll a resurgent COVID-19 is taking.

Germany's Angela Merkel warns the coronavirus situation in the powerhouse economy is dramatic, the Netherlands is in partial lockdown and pressure is mounting on Austria to do more. But vaccine rollouts and the reassuring - and hefty - presence of ECB stimulus ease some of those worries.

#3 RBNZ meeting

The Reserve Bank of New Zealand is expected to move deeper into the vanguard of inflation fighters on Wednesday, and deliver a second rate hike in as many months. Since October, when the RBNZ joined Norway as developed markets' first hikers, inflation has surged to a decade high and the unemployment rate has sunk to record lows.

Traders are sure rates will go up, and are focused on two hawkish risks: A roughly 40% chance that the hike is a chunky 50 bps one, and the bank lifts its long-term rates outlook. Either could hoist the kiwi higher, though both bring risks to local borrowers already squeezed by the fastest pace of mortgage rate rises in 15 years.

Conclusion

This week brings no big shifts in overall sentiment. Technical picture has not changed either as EUR has dropped more and comes close to major weekly support area. Overall market consensus stands in favor of longer period of high inflation that should furlong into 1Q of 2022 and start to normalize after. At least, this is common suggestion right now. Fed minutes hardly could make strong impact as meeting was prior the decisive CPI data release. Until December meeting pressure should grow as coming PCE, NFP wage data and PPI/CPI in the beginning of December should creep even higher, as it is widely suggested. All these aspects warm up US Dollar demand and push Fed to more aggressive steps, at least in tapering process. As a secondary factor we could point on some geopolitical affairs in Eastern Europe and Taiwan that also indirectly support dollar demand.

The fact that the US has printed another 3% Global GDP (1 Trln approved pack and new 1.75 Trln that has passed the Congress) only rises the inflation expectations. This is background explains why we do not see any reasons to change our mid term view on EUR/USD. Also we see signs that supply chains' bottlenecks are forming artificially as well as gas price rally to dump China and EU economies. But this is too wide subject for discussion here in details.

Technicals

Monthly

On monthly time frame everything remains the same, as market confirms our plan and keep going lower. Downside tendency has good momentum with multiple tail closed months, including November by far.

In general, currently trend stands bearish. Once market hits all-time OP around 1.06 area it turns to consolidation that now is taking the shape of extended triangle. Last week we've considered upside scenario based on potential change in long-term sentiment of major Central Banks, but now, in the light of recent events, we leave this scenario for now. As price breaks minor pennant, forming bearish reversal action in September, and dropping below YPP - the nearest target stands around 1.10-1.12 area. The same target is mentioned above by Société Générale. Here is we have monthly COP, YPS1 and trend line support, while on weekly and daily time frames some other objects exist in this area. For now, the reaching of this area seems probable as it is not big distance till this level.

As market is not at oversold here and target is not hit yet, we expect downside continuation within few weeks with minor local breaks for retracements.

Weekly

This week market has made big step toward our major destination point here which is Agreement of XOP 1.1220 target and major 1.1290 Fib support. We do not expect the pullback until market hits XOP level, despite it stands oversold right now. This week you could see that upside reaction is muted and market turns down again as soon as possible. So, we do not consider any long positions on daily/intraday charts, until XOP is hit.

Daily

So, market fills the trading plan pretty accurately this time. Downside action starts right from pre-defined intraday K-area. As you can see, despite oversold level, upward bounce was just minor harmonic swing. Now market stands not too far from weekly XOP, which is around 1.1218-1.1220 area. The first sign that we get upside reaction should be appearing of some bullish pattern on daily/ 4H time frame. Currently is nothing to do on daily chart as market stands near support area. Until XOP is hit and bullish pattern is formed we could consider setups only on intraday charts.

Intraday

The general idea, when market tends to major target and stands at oversold on weekly chart is to take scalp short positions and out at around recent lows. This setup could repeat few times, until price hits weekly XOP.

Of course, market could keep going lower, directly to XOP. In this case we just do not get trading setup at all. In a case of pullback though, we could watch for something like that - "222" Sell" around some resistance level.

") , but anyway, tomorrow the situation is promised to be the same as US markets are closed now. So FX probably will be thin as well.

, but anyway, tomorrow the situation is promised to be the same as US markets are closed now. So FX probably will be thin as well.