Sive Morten

Special Consultant to the FPA

- Messages

- 18,655

Fundamentals

So it was terrible wake up after the Thanksgiving. Personally, I'm dealing with stock derivatives, and yesterday was very tough session as EU DAX index has dropped for 5% in single session. S&P performance also hardly could be called as optimistic. Of course, here we have emotional component as well. As you know fear is much stronger than greed and this explains why markets drop faster than rising. With some degree the same performance happens every time when new variant appears. Scientists need some time to examine it and within week or two we should get more clarity. Hopefully recent reaction will short term and not lead to massive globe shut down again. Besides, if worst scenario turns to reality - it drastically changes the financial background as well, cancelling rate hikes, starting of deflation again. Hopefully it won't run to that. At current moment we should have flexible view on ongoing situation just because it cares too much emotions and too few common sense. Markets are overreacting under fear impact.

Market overview

The discovery of a new coronavirus variant named Omicron triggered global alarm on Friday as countries rushed to suspend travel from southern Africa and stock markets on both sides of the Atlantic suffered their biggest falls in more than a year. The World Health Organization (WHO) said Omicron may spread more quickly than other forms, and preliminary evidence suggested there is an increased risk of reinfection.

Epidemiologists warned travel curbs may be too late to stop Omicron from circulating globally. The new mutations were first discovered in South Africa and have since been detected in Belgium, Botswana, Israel and Hong Kong. The United States will restrict travel from South Africa and neighboring countries effective Monday, a senior Biden administration official said. Going further, Canada said it was closing its borders to those countries, following bans on flights announced by Britain, the European Union and others.

But it could take weeks for scientists to fully understand the variant's mutations and whether existing vaccines and treatments are effective against it. Omicron is the fifth variant of concern designated by the WHO. The variant has a spike protein that is dramatically different than the one in the original coronavirus that vaccines are based on, the UK Health Security Agency said, raising fears about how current vaccines will fare. Scientists issued similar warnings.

One epidemiologist in Hong Kong said it may be too late to tighten travel curbs against the latest variant. "Most likely this virus is already in other places. And so if we shut the door now, it's going to be probably too late," said Ben Cowling of the University of Hong Kong.

New York Governor Kathy Hochul issued a COVID-19 "disaster emergency" declaration on Friday, citing increasing rates of infections and hospitalizations.

Speaking on earlier events, minutes from the Fed's Nov. 2-3 meeting boosted the dollar on Wednesday as they indicated the Fed had become more concerned about rising inflation. Various policymakers said they would be open to speeding up the taper of their bond-buying programme if high inflation held and move more quickly to raise interest rates

U.S. jobless claims were at a 52-year low, consumer spending increased more than expected in October and inflation was rising.

A surge in coronavirus infections in Germany and unusually high inflation rates are weighing on consumer morale in Europe's largest economy, a survey showed on Thursday. The Ifo institute said its business climate index fell to 96.5 from 97.7 in October.

Various Fed policymakers said they would be open to speeding up the elimination of their bond-buying program if high inflation held and move more quickly to raise interest rates, minutes of the bank's last policy meeting released on Wednesday showed.

San Francisco Fed President Mary Daly said in an interview with Yahoo Finance released the same day that she could see a case being made to speed up the Fed's tapering of its bond purchases.

Elsewhere, Sterling briefly weakened below $1.33 on Friday for the first time since December 2020 as a new COVID-19 variant described as the most concerning yet hit sentiment in global markets. Concerns it might be harder to combat the new variant found in southern Africa with vaccines also prompted investors to scale back their expectations for a Bank of England (BoE) interest rate rise in December, adding to downward pressure on the pound.

The European Central Bank is likely to stop further bond purchases under its pandemic-era support scheme from early next year but will still have other purchasing programmes in its toolkit, President Christine Lagarde was quoted as saying by a German daily.

Lagarde also said the ECB will act on interest rates when necessary and when price rises reach 2% on a sustained basis but she expected inflation to fall from January.

Her comments came as two ECB policymakers said the euro zone economy faced a fresh challenge from a rise in coronavirus cases and a new variant

New COVID scare sparks rate rethink in markets

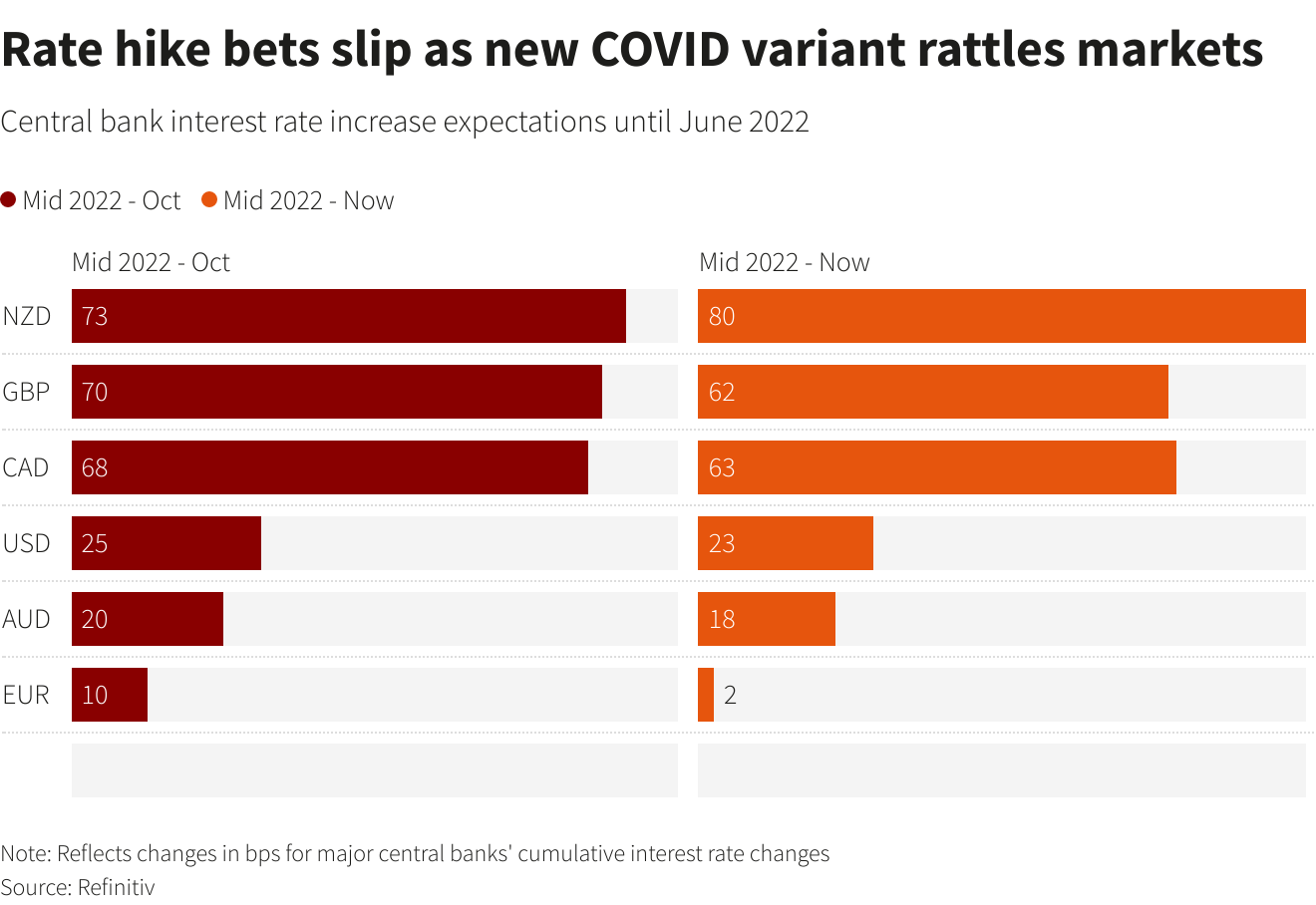

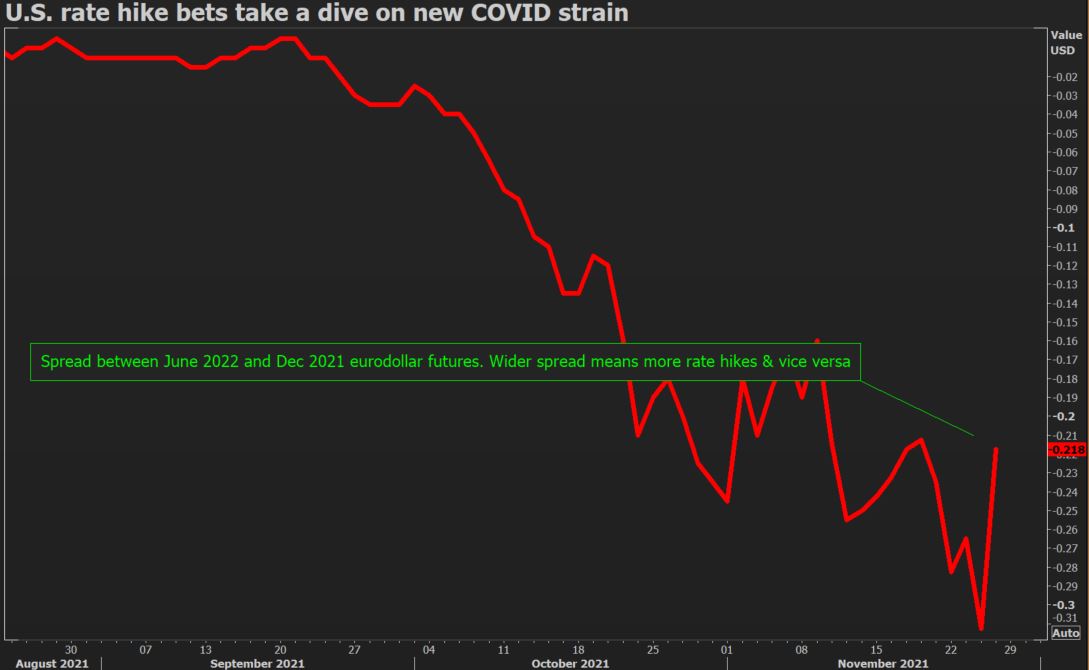

Risks of a new COVID hit to economic activity are clobbering expectations for rate hikes next year from the world's major central banks, a potential setback for the dollar and other currencies where wagers had been most aggressive.

Money markets no longer fully price a 25-basis-point interest rate rise by the Federal Reserve by June 2022, nor are they positioned for a full 10-bps hike from the European Central Bank by the end of 2022, as they were just a few days ago. And the chances of the Bank of England raising rates next month are seen around 53%, from 75% on Thursday.

In an echo of the panic that swept markets when COVID was spreading early last year, oil prices slid over 6% on Friday, travel industry shares notched up falls of 6% or more and two-year U.S. Treasury yields fell 12 bps in their biggest daily drop since March 2020.

Currency traders had been favoring the U.S. dollar and others where rate hike prospects appeared strong, driven by higher inflation and stronger economies. Now a shake-out appears on the cards.

The dollar index had hit 17-month highs after President Joe Biden said on Monday he would nominate Fed Chairman Jerome Powell to a second term. Then, minutes of the Fed's Nov. 2-3 meeting showed more policymakers open to speeding up the tapering of asset purchases and raising rates. So with three 25 basis-point Fed increases factored in for 2022, speculators accumulated a $20 billion "long" position in the dollar, data from the U.S. CFTC showed.

The new variant may also complicate the task for central banks if it worsens the supply chain delays that are partly blamed for stoking inflation. Britain, where inflation has hit 10-year highs, had some 70 bps of policy-tightening priced by mid-2022, despite a lackluster economic recovery.

In Europe, the new strain could strengthen the hand of doves on the ECB's Governing Council.

NEXT WEEK TO WATCH

#1 EU Inflation data

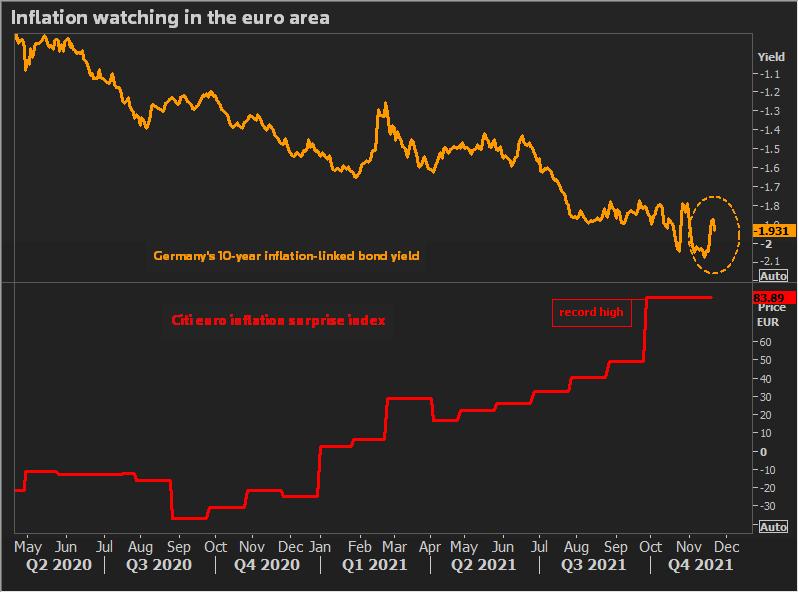

Tuesday brings November flash euro zone inflation. October's print was 4.1% and many see it staying above the ECB's 2% target next year. German, Spanish and French CPI data are out Monday and Tuesday. As inflation surges, ECB hawks warn against keeping monetary policy too loose for too long. A new German government meanwhile could raise the minimum wage by around 25%.

Their message has resonated with edgy markets. But resurgent COVID strengthens the ECB doves as Europe battles a fresh surge and news of new virus variant spreading across South Africa triggers alarm. Renewed economic uncertainty means investors are again scaling back rate-hike bets for the U.S., euro area and Britain. The doves, it appears, have fresh ammunition to push back against those clamoring for an early end to stimulus.

#2 US NFP Data

With the Federal Reserve's taper underway, a strong November employment report could bolster the case for those arguing its $120 billion-a-month bond-buying should be unwound faster.

While the Fed projects the unwinding to be complete in mid-2022, robust economic growth and inflation running at more than twice the 2% flexible average goal have sparked bets on a faster unwind and earlier rate rises.

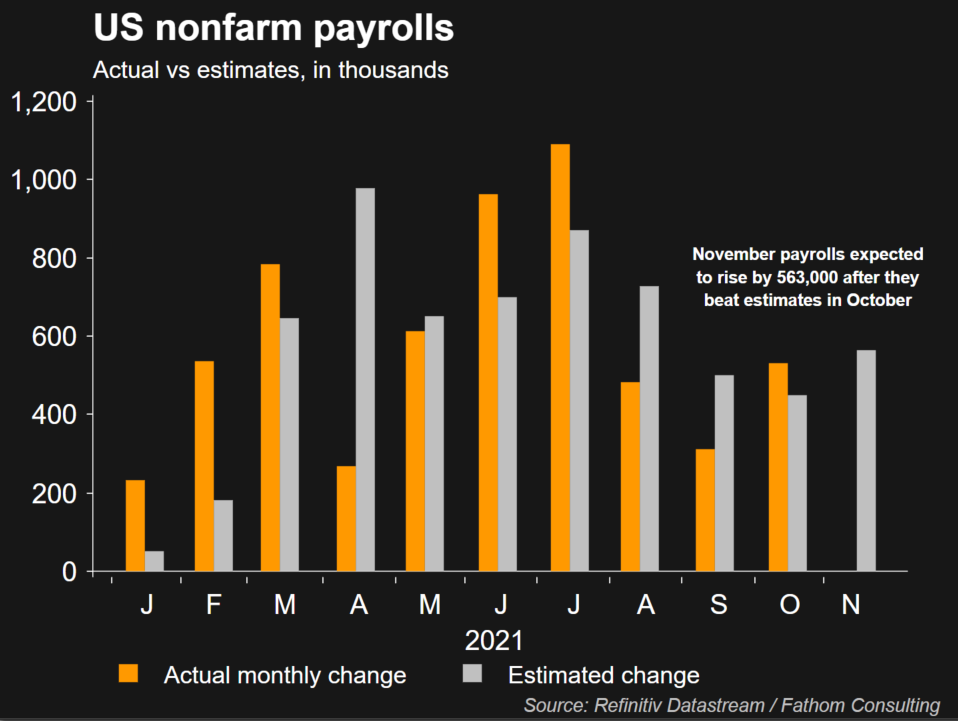

Payroll expectations were boosted by weekly data showing jobless benefits claims at the lowest since 1969. Employers are forecast to have added 563,000 jobs, and any figure more than that could revive recent bond market ructions and mean another leg higher for the dollar.

#3 J.Powell Congress speech

Investors will be watching Fed Chair Jerome Powell and U.S. Treasury Secretary Janet Yellen's appearance before Congress to discuss the government's COVID response on Nov. 30

#4 OPEC+ meeting and Chinese PMI release

The Bottom line

So, with the comments above you cold feel the overall atmosphere that stands on the markets and in minds of the investors. What we could say? The correct word is "uncertainty" and "overreaction". Big Investing banks and market makers easily could shake the boat, speculating on the fears of the investors, triggering the chain sell-off reaction up from institutional investors down to retail brokers. But, using the common sense we should ask - whether this is the first new variant, or maybe it is the last one? Do we know something about it or we already see the terrible effect of its spreading across the Globe? Another question is - whether this variant impacts differently on US and EU? All these questions suggest the same answer - "No". The new reality is we live with this new virus, whether we want it or not.

It means that status quo between US and EU policies should remain the same, in general. Here we should talk about just two scenarios - light and dark. With light scenario new variant fears should fade out as it was with "delta" variant and everything remains on its own. Dark scenario suggests returning to the lockdowns across the Globe and pre-vaccine era. But what does it change?

As with the first scenario US Dollar should keep the dominant role as the US stands closer to rate change and economy performance is much better than in EU, as with the 2nd scenario negative effect in EU will be tougher. Besides, new lockdown suggests more bottlenecks, more money printing, stimulus packs. With this environment safe haven demand should push interest rates down and keep high demand for US Dollar anyway.

This leads us to conclusion that whatever negative effect we get from "Omicron" - it triggers short-term rebalancing and pullback on US Dollar, just because the change of interest rates adjustments terms. The bulk of this event is already priced-in. With bad scenario it should be postponed on later time, which could trigger short-term correction on US Dollar to set it in proper place in relation to EUR (and other currencies). But, once it happens - demand for USD should remain. That's being said. We suggest that light scenario should make no impact on currency markets, while "dark" scenario triggers short-term retracement. Once it will be over - dollar should keep rising again, just because of better fundamentals compares to its rivals.

Finally the pullback perfectly fits to our technical picture as EUR and DXY comes to strong support areas. So we better to be aimed on facts and the nearest ones are inflation data and NFP in December. Once fundamental will be released, emotions should take the backseat.

Technicals

Monthly

So, our COP target has been hit pretty accurately on Thursday. Now EUR is ready to start technical pullback - the response on few extension targets and weekly support area. This is actually what we see right now. Still, as we've said above, the downward continuation seems the question of time, even based only on technical signs. Take a look that the action to COP is direct. CD leg of AB-CD pattern is much faster. Besides, with coming military escalation on Eastern Europe, this becomes additional bearish factor for EUR. So, our central scenario here is the same - once pullback is over, we expect downside continuation to YPS1 first and potentially to OP around 1.0430.

Weekly

Here is we see natural response to support area with hammer pattern. So, reaction just has started. Normally market should not show any new dive below the lows as all targets around have been hit already. Thus, current low is our invalidation point and we build following trading tactics around it. In fact, here we have DiNapoli bullish "Stretch" pattern as well.

The problem stands with trend direction, as it is bearish on all time frames, that doesn't let us to consider extended upside targets.

Daily

Here we see first upside reaction, while we still have no bullish patterns on daily chart. FX Choice chart shows nice combination of 3/8 Fib resistance and daily Overbought level. But, if you take a look at CME Futures - we have none of them. Trend still stands bearish and chances on appearing bearish grabber exist as well. So, currently we do not see any background for long entry. Scalp short position could be considered based on intraday charts as well:

Intraday

Currently we could consider short-term bearish setup only, in a row with daily a kind of B&B "Sell" setup. Our 3-Drive works perfect. While previous bearish momentum is strong, EUR needs some time to fade it down. Thus, downside 1/2-6/8 retracement has good chances to happen. While it brings nothing important to daily setup, where we still waiting for something more extended, here, intraday traders could consider scalp short scenario, as EUR has completed upside 1.618 extension and formed something like DRPO "Sell" top with reversal candle:

So it was terrible wake up after the Thanksgiving. Personally, I'm dealing with stock derivatives, and yesterday was very tough session as EU DAX index has dropped for 5% in single session. S&P performance also hardly could be called as optimistic. Of course, here we have emotional component as well. As you know fear is much stronger than greed and this explains why markets drop faster than rising. With some degree the same performance happens every time when new variant appears. Scientists need some time to examine it and within week or two we should get more clarity. Hopefully recent reaction will short term and not lead to massive globe shut down again. Besides, if worst scenario turns to reality - it drastically changes the financial background as well, cancelling rate hikes, starting of deflation again. Hopefully it won't run to that. At current moment we should have flexible view on ongoing situation just because it cares too much emotions and too few common sense. Markets are overreacting under fear impact.

Market overview

The discovery of a new coronavirus variant named Omicron triggered global alarm on Friday as countries rushed to suspend travel from southern Africa and stock markets on both sides of the Atlantic suffered their biggest falls in more than a year. The World Health Organization (WHO) said Omicron may spread more quickly than other forms, and preliminary evidence suggested there is an increased risk of reinfection.

Epidemiologists warned travel curbs may be too late to stop Omicron from circulating globally. The new mutations were first discovered in South Africa and have since been detected in Belgium, Botswana, Israel and Hong Kong. The United States will restrict travel from South Africa and neighboring countries effective Monday, a senior Biden administration official said. Going further, Canada said it was closing its borders to those countries, following bans on flights announced by Britain, the European Union and others.

But it could take weeks for scientists to fully understand the variant's mutations and whether existing vaccines and treatments are effective against it. Omicron is the fifth variant of concern designated by the WHO. The variant has a spike protein that is dramatically different than the one in the original coronavirus that vaccines are based on, the UK Health Security Agency said, raising fears about how current vaccines will fare. Scientists issued similar warnings.

Several other countries including India, Japan, Israel, Turkey, Switzerland and the United Arab Emirates also toughened travel curbs."This new variant of the COVID-19 virus is very worrying. It is the most heavily mutated version of the virus we have seen to date," said Lawrence Young, a virologist at Britain's University of Warwick. "Some of the mutations that are similar to changes we've seen in other variants of concern are associated with enhanced transmissibility and with partial resistance to immunity induced by vaccination or natural infection."

One epidemiologist in Hong Kong said it may be too late to tighten travel curbs against the latest variant. "Most likely this virus is already in other places. And so if we shut the door now, it's going to be probably too late," said Ben Cowling of the University of Hong Kong.

New York Governor Kathy Hochul issued a COVID-19 "disaster emergency" declaration on Friday, citing increasing rates of infections and hospitalizations.

Speaking on earlier events, minutes from the Fed's Nov. 2-3 meeting boosted the dollar on Wednesday as they indicated the Fed had become more concerned about rising inflation. Various policymakers said they would be open to speeding up the taper of their bond-buying programme if high inflation held and move more quickly to raise interest rates

U.S. jobless claims were at a 52-year low, consumer spending increased more than expected in October and inflation was rising.

Neil Jones, head of FX sales at Mizuho, said that he expects the dollar's move lower to be a "temporary blip". Post-Thanksgiving next week and into December I’m looking for further dollar strength, albeit at a fairly subdued pace," he said. Jones said that towards the end of the year seasonal demand for dollars would also contribute to its strength.

"Given that this particular trade-weighted measure of the dollar is heavily skewed to European currencies, the combination of a bullish Fed and fourth waves in Europe is making the DXY (dollar index) look very bid," wrote ING currency strategists in a note to clients.

A surge in coronavirus infections in Germany and unusually high inflation rates are weighing on consumer morale in Europe's largest economy, a survey showed on Thursday. The Ifo institute said its business climate index fell to 96.5 from 97.7 in October.

Various Fed policymakers said they would be open to speeding up the elimination of their bond-buying program if high inflation held and move more quickly to raise interest rates, minutes of the bank's last policy meeting released on Wednesday showed.

San Francisco Fed President Mary Daly said in an interview with Yahoo Finance released the same day that she could see a case being made to speed up the Fed's tapering of its bond purchases.

"The U.S. economy retained its titanium status," while "slightly hawkish comments from the normally dovish Daly" also helped to lift the dollar, Tapas Strickland, a director of economics at National Australia Bank, wrote in a research note.

Elsewhere, Sterling briefly weakened below $1.33 on Friday for the first time since December 2020 as a new COVID-19 variant described as the most concerning yet hit sentiment in global markets. Concerns it might be harder to combat the new variant found in southern Africa with vaccines also prompted investors to scale back their expectations for a Bank of England (BoE) interest rate rise in December, adding to downward pressure on the pound.

"London is naturally highly exposed to new strains (of the coronavirus) given its high volume of travellers, and markets will be on the lookout in the coming days for any evidence the new variant has already reached the UK, with obvious downside risks for the pound," said ING analysts.

“After the fed minutes it seems likely everybody was expecting an accelerated Fed taper. If we continue to hear more of a greater spreading of this new variant, you might start to see that the argument will be made that no, we need to gradually exit stimulus here and we’re not completely sure how the vaccines will hold up against this and possibly more variants down the road as we’re nowhere near getting the rest of the world vaccinated. What has really complicated today was that we have options expiration day and extremely thin conditions, so I think ultimately when everybody is back next week, if this variant concern continues to dominate the headlines, then you’ll start to see the dollar resume its safe-haven trade, said Edward Moya, OANDA.

"A new Covid wave is leading investors to fly to safety, provoking yields to drop roughly 10 bps across the whole US yield curve. However, we expect the bond rally to be short-lived for several reasons. First, the market has learnt through earlier new strains that Covid is temporary. Secondly, a renewal of lockdown measures would make supply chain bottlenecks worse, introducing even more inflationary pressures to the economy. Therefore, it’s necessary for central banks to stop stimulating demand, keeping intact the recent Fed’s hawkish tilt, said Steen Jakobsen, from SaxoBank.

"Markets were celebrating the end of the pandemic. Slam. It isn't over," said David Kotok, chairman and chief investment officer at Cumberland Advisors. "All policy issues, meaning monetary policy, business trajectories, GDP growth estimates, leisure and hospitality recovery, the list goes on, are on hold."

The European Central Bank is likely to stop further bond purchases under its pandemic-era support scheme from early next year but will still have other purchasing programmes in its toolkit, President Christine Lagarde was quoted as saying by a German daily.

"Given current circumstances, I expect that we will not carry out any further (PEPP) bond purchases from early next year," Lagarde was quoted by the Frankfurter Allgemeine Zeitung as saying. That doesn't mean that PEPP will be totally ended because we have to replace the expiring bonds. And do not forget that we have other purchase programmes in our toolkit.

Lagarde also said the ECB will act on interest rates when necessary and when price rises reach 2% on a sustained basis but she expected inflation to fall from January.

It's eye-catching at the moment and is worrying a lot of people but we do not expect this rise in inflation to last," Lagarde said. "Next year it will calm down again. Already from January onwards, we expect the inflation rate to begin falling."

Her comments came as two ECB policymakers said the euro zone economy faced a fresh challenge from a rise in coronavirus cases and a new variant

New COVID scare sparks rate rethink in markets

Risks of a new COVID hit to economic activity are clobbering expectations for rate hikes next year from the world's major central banks, a potential setback for the dollar and other currencies where wagers had been most aggressive.

Money markets no longer fully price a 25-basis-point interest rate rise by the Federal Reserve by June 2022, nor are they positioned for a full 10-bps hike from the European Central Bank by the end of 2022, as they were just a few days ago. And the chances of the Bank of England raising rates next month are seen around 53%, from 75% on Thursday.

"While central bank commentary has been focused on upside risks to inflation, this (new COVID variant) highlights that there are significant downside risks and we are in a significant phase of uncertainty for the economy," said Chris Scicluna, head of economic research at Daiwa.

In an echo of the panic that swept markets when COVID was spreading early last year, oil prices slid over 6% on Friday, travel industry shares notched up falls of 6% or more and two-year U.S. Treasury yields fell 12 bps in their biggest daily drop since March 2020.

Currency traders had been favoring the U.S. dollar and others where rate hike prospects appeared strong, driven by higher inflation and stronger economies. Now a shake-out appears on the cards.

The dollar index had hit 17-month highs after President Joe Biden said on Monday he would nominate Fed Chairman Jerome Powell to a second term. Then, minutes of the Fed's Nov. 2-3 meeting showed more policymakers open to speeding up the tapering of asset purchases and raising rates. So with three 25 basis-point Fed increases factored in for 2022, speculators accumulated a $20 billion "long" position in the dollar, data from the U.S. CFTC showed.

If the new COVID variant has indeed disrupted Fed policy, "the dollar may be a bit more vulnerable than the euro because we are already talking of two-three rate hikes next year from the Fed," Francesco Pesole, FX strategist at ING Bank said.

UBS Investment Bank chief economist Arend Kapteyn said while confidence in improving U.S. labour markets could fade if a new variant takes hold, it was still early days in terms of gauging the impact. But he added that "the market had gotten too far ahead of itself in terms of pricing a shortened taper window and multiple hikes next year".

The new variant may also complicate the task for central banks if it worsens the supply chain delays that are partly blamed for stoking inflation. Britain, where inflation has hit 10-year highs, had some 70 bps of policy-tightening priced by mid-2022, despite a lackluster economic recovery.

In Europe, the new strain could strengthen the hand of doves on the ECB's Governing Council.

While the ECB is expected to wind down its 1.85 trillion euro ($2.08 trillion) pandemic emergency stimulus scheme, Mizuho strategist Peter McCallum now sees a greater chance the programme gets extended beyond the March deadline. They (ECB) were saying that the European situation doesn't change the PEPP outcome but if there is a new variant requiring new vaccines that surely does change the picture," said McCallum.

NEXT WEEK TO WATCH

#1 EU Inflation data

Tuesday brings November flash euro zone inflation. October's print was 4.1% and many see it staying above the ECB's 2% target next year. German, Spanish and French CPI data are out Monday and Tuesday. As inflation surges, ECB hawks warn against keeping monetary policy too loose for too long. A new German government meanwhile could raise the minimum wage by around 25%.

Their message has resonated with edgy markets. But resurgent COVID strengthens the ECB doves as Europe battles a fresh surge and news of new virus variant spreading across South Africa triggers alarm. Renewed economic uncertainty means investors are again scaling back rate-hike bets for the U.S., euro area and Britain. The doves, it appears, have fresh ammunition to push back against those clamoring for an early end to stimulus.

#2 US NFP Data

With the Federal Reserve's taper underway, a strong November employment report could bolster the case for those arguing its $120 billion-a-month bond-buying should be unwound faster.

While the Fed projects the unwinding to be complete in mid-2022, robust economic growth and inflation running at more than twice the 2% flexible average goal have sparked bets on a faster unwind and earlier rate rises.

Payroll expectations were boosted by weekly data showing jobless benefits claims at the lowest since 1969. Employers are forecast to have added 563,000 jobs, and any figure more than that could revive recent bond market ructions and mean another leg higher for the dollar.

#3 J.Powell Congress speech

Investors will be watching Fed Chair Jerome Powell and U.S. Treasury Secretary Janet Yellen's appearance before Congress to discuss the government's COVID response on Nov. 30

Investors held out hope that markets could stabilize. Jack Ablin, chief investment officer at Cresset Capital Management, said moves may have been exaggerated by lack of liquidity on Friday, with many participants out for the Thanksgiving holiday. My first reaction is anything we are going to see today is overdone," Ablin said.

#4 OPEC+ meeting and Chinese PMI release

The Bottom line

So, with the comments above you cold feel the overall atmosphere that stands on the markets and in minds of the investors. What we could say? The correct word is "uncertainty" and "overreaction". Big Investing banks and market makers easily could shake the boat, speculating on the fears of the investors, triggering the chain sell-off reaction up from institutional investors down to retail brokers. But, using the common sense we should ask - whether this is the first new variant, or maybe it is the last one? Do we know something about it or we already see the terrible effect of its spreading across the Globe? Another question is - whether this variant impacts differently on US and EU? All these questions suggest the same answer - "No". The new reality is we live with this new virus, whether we want it or not.

It means that status quo between US and EU policies should remain the same, in general. Here we should talk about just two scenarios - light and dark. With light scenario new variant fears should fade out as it was with "delta" variant and everything remains on its own. Dark scenario suggests returning to the lockdowns across the Globe and pre-vaccine era. But what does it change?

As with the first scenario US Dollar should keep the dominant role as the US stands closer to rate change and economy performance is much better than in EU, as with the 2nd scenario negative effect in EU will be tougher. Besides, new lockdown suggests more bottlenecks, more money printing, stimulus packs. With this environment safe haven demand should push interest rates down and keep high demand for US Dollar anyway.

This leads us to conclusion that whatever negative effect we get from "Omicron" - it triggers short-term rebalancing and pullback on US Dollar, just because the change of interest rates adjustments terms. The bulk of this event is already priced-in. With bad scenario it should be postponed on later time, which could trigger short-term correction on US Dollar to set it in proper place in relation to EUR (and other currencies). But, once it happens - demand for USD should remain. That's being said. We suggest that light scenario should make no impact on currency markets, while "dark" scenario triggers short-term retracement. Once it will be over - dollar should keep rising again, just because of better fundamentals compares to its rivals.

Finally the pullback perfectly fits to our technical picture as EUR and DXY comes to strong support areas. So we better to be aimed on facts and the nearest ones are inflation data and NFP in December. Once fundamental will be released, emotions should take the backseat.

Technicals

Monthly

So, our COP target has been hit pretty accurately on Thursday. Now EUR is ready to start technical pullback - the response on few extension targets and weekly support area. This is actually what we see right now. Still, as we've said above, the downward continuation seems the question of time, even based only on technical signs. Take a look that the action to COP is direct. CD leg of AB-CD pattern is much faster. Besides, with coming military escalation on Eastern Europe, this becomes additional bearish factor for EUR. So, our central scenario here is the same - once pullback is over, we expect downside continuation to YPS1 first and potentially to OP around 1.0430.

Weekly

Here is we see natural response to support area with hammer pattern. So, reaction just has started. Normally market should not show any new dive below the lows as all targets around have been hit already. Thus, current low is our invalidation point and we build following trading tactics around it. In fact, here we have DiNapoli bullish "Stretch" pattern as well.

The problem stands with trend direction, as it is bearish on all time frames, that doesn't let us to consider extended upside targets.

Daily

Here we see first upside reaction, while we still have no bullish patterns on daily chart. FX Choice chart shows nice combination of 3/8 Fib resistance and daily Overbought level. But, if you take a look at CME Futures - we have none of them. Trend still stands bearish and chances on appearing bearish grabber exist as well. So, currently we do not see any background for long entry. Scalp short position could be considered based on intraday charts as well:

Intraday

Currently we could consider short-term bearish setup only, in a row with daily a kind of B&B "Sell" setup. Our 3-Drive works perfect. While previous bearish momentum is strong, EUR needs some time to fade it down. Thus, downside 1/2-6/8 retracement has good chances to happen. While it brings nothing important to daily setup, where we still waiting for something more extended, here, intraday traders could consider scalp short scenario, as EUR has completed upside 1.618 extension and formed something like DRPO "Sell" top with reversal candle:

")