IvanGlobalPrime

Company Representative

- Messages

- 36

Find my latest market thoughts

Bond Yields Fall As Focus Back To Easing Cycles

POSTED ON: 03 JUL, 2019

The tormented state of affairs in global bond yields just days after the US and China agreed to a trade truce is a clear indication that it's going to take a lot more than just promises of a resumption in trade talks if the market is to keep buying into the idea of risk trades.

The Daily Edge is authored by Ivan Delgado, Market Insights Commentator at Global Prime. The purpose of this content is to provide an assessment of the market conditions. The report takes an in-depth look of market dynamics, factoring in fundamentals, technicals, inter-market in order to determine daily biases and assist one’s decisions on a regular basis. Feel free to follow Ivan on Twitter & Youtube.

Quick Take

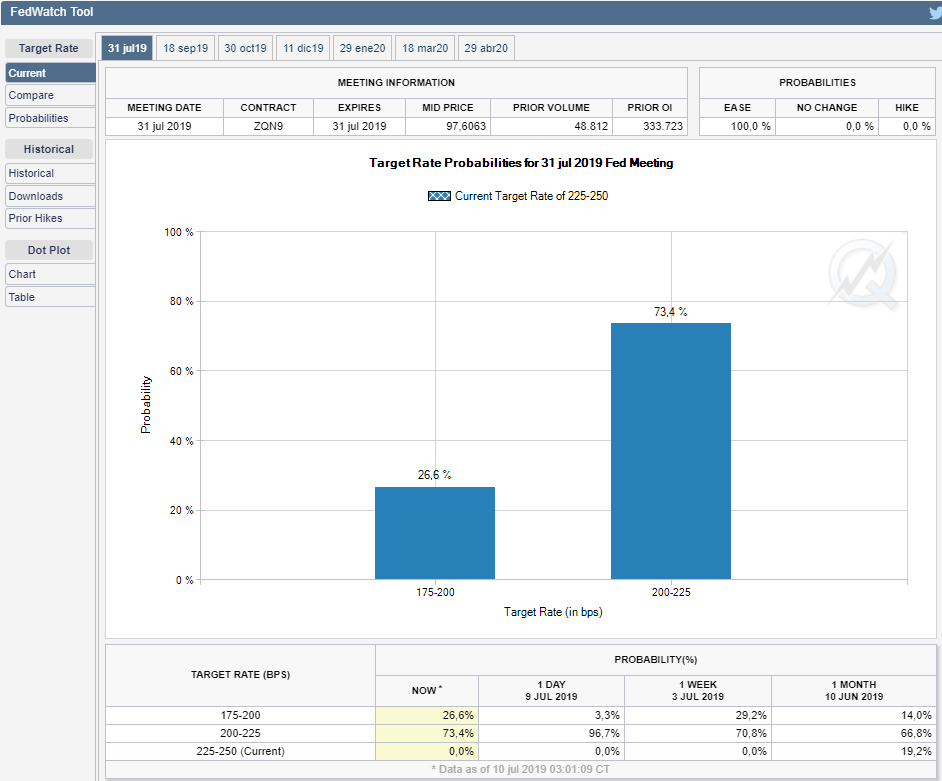

The tormented state of affairs in global bond yields just days after the US and China agreed to a trade truce is a clear indication that it's going to take a lot more than just promises of a resumption in trade talks if the market is to keep buying into the idea of risk trades. BoE's Governor Carney was the last key actor to warn, rightly so, that as the tactics of protectionist policies by the US pans out, the global economy not only is on tenterhooks but if tensions continue it may "shipwreck" prospects for growth. It is also clear that the reversal in global yields back in line with the main macro trend means the market has 'moved on' from any G20-induced paraphernalia to be fixated back to the path of global central bank easing. The Japanese Yen's strong appreciation against most currencies is the proof in the pudding that risk is far from conducive, as is the sell-off in Crude Oil despite OPEC agreed to extend production cuts for nine months tells, which us a similar story. Meanwhile, the ballistic move back up in Gold, tells us global easing cycles remain the true catalyst to keep the bull run going strong. Interestingly, the two most heavily traded currencies, the EUR, and USD, both performed poorly, even if it was the Sterling that had the worst daily run as the market comes to terms about the pessimistic outlook by BoE's Governor Carney. The diversification of flows favored the AUD and CAD although aggregated tick volume in both indices does not suggest further continuation with Intermarket flows not backing up the trends (Lower Yuan and Oil).

Narratives In Financial Markets

* The Information is gathered after scanning top publications including the FT, WSJ, Reuters, Bloomberg, ForexLive, Institutional Bank Research reports.

RORO (Risk On, Risk Off Conditions)

Recent Economic Indicators & Events Ahead

Source: Forexfactory

A Dive Into Developments In FX (Technicals, Fundamentals, Intermarket)

EUR/USD: 100% Proj Target Pauses Move Down, Sellers Step In At Resistance

GBP/USD: Bearish Outlook Persists, Cluster Of Bids Found at Proj Target

AUD/USD: Looking Rather Expensive Based On Intermarket Flows

USD/JPY: Bullish Outlook Negated, Testing Critical Support

Crude Oil: Focus Clearly Shifts To Sell Rallies

Gold: Upside Breakout Of Descending Trendline In-Line w/ Main Technical Trend

Important Footnotes

Bond Yields Fall As Focus Back To Easing Cycles

POSTED ON: 03 JUL, 2019

The tormented state of affairs in global bond yields just days after the US and China agreed to a trade truce is a clear indication that it's going to take a lot more than just promises of a resumption in trade talks if the market is to keep buying into the idea of risk trades.

The Daily Edge is authored by Ivan Delgado, Market Insights Commentator at Global Prime. The purpose of this content is to provide an assessment of the market conditions. The report takes an in-depth look of market dynamics, factoring in fundamentals, technicals, inter-market in order to determine daily biases and assist one’s decisions on a regular basis. Feel free to follow Ivan on Twitter & Youtube.

Quick Take

The tormented state of affairs in global bond yields just days after the US and China agreed to a trade truce is a clear indication that it's going to take a lot more than just promises of a resumption in trade talks if the market is to keep buying into the idea of risk trades. BoE's Governor Carney was the last key actor to warn, rightly so, that as the tactics of protectionist policies by the US pans out, the global economy not only is on tenterhooks but if tensions continue it may "shipwreck" prospects for growth. It is also clear that the reversal in global yields back in line with the main macro trend means the market has 'moved on' from any G20-induced paraphernalia to be fixated back to the path of global central bank easing. The Japanese Yen's strong appreciation against most currencies is the proof in the pudding that risk is far from conducive, as is the sell-off in Crude Oil despite OPEC agreed to extend production cuts for nine months tells, which us a similar story. Meanwhile, the ballistic move back up in Gold, tells us global easing cycles remain the true catalyst to keep the bull run going strong. Interestingly, the two most heavily traded currencies, the EUR, and USD, both performed poorly, even if it was the Sterling that had the worst daily run as the market comes to terms about the pessimistic outlook by BoE's Governor Carney. The diversification of flows favored the AUD and CAD although aggregated tick volume in both indices does not suggest further continuation with Intermarket flows not backing up the trends (Lower Yuan and Oil).

Narratives In Financial Markets

* The Information is gathered after scanning top publications including the FT, WSJ, Reuters, Bloomberg, ForexLive, Institutional Bank Research reports.

- Global bond yields implode after BoE’s Carney warns of trade tensions as the main source of concern that may further evaporate the prospects for momentum in the global economy. Carney used alarming words such as trade strifes mat “shipwreck the global economy.”

- The market has also shifted its view on the BOE policy prospects by assigning a 50% chance of a rate cut by the BoE before the end of the year. As a result, long-term UK yields took a hit that has sent them below the BOE benchmark interest rate in the first inversion in a decade. A sharp fall in the UK construction PMI, lowest since April 2009, added to the sour sentiment.

- Further evidence of the protracted bullish macro trend in lower global yields was music to the ears of Gold bulls, taking the precious metal significantly higher against a basket of G10 FX.

- Oil suffers a major slide even as OPEC agrees to extend production cuts for nine months to prevent 100 mil barrels build-up. All countries promised to improve on compliance with cuts. The dark clouds hovering over the outlook for the global economy outweighed any positives as the trade truce between the US and China is rapidly fading away amid lack of concrete details.

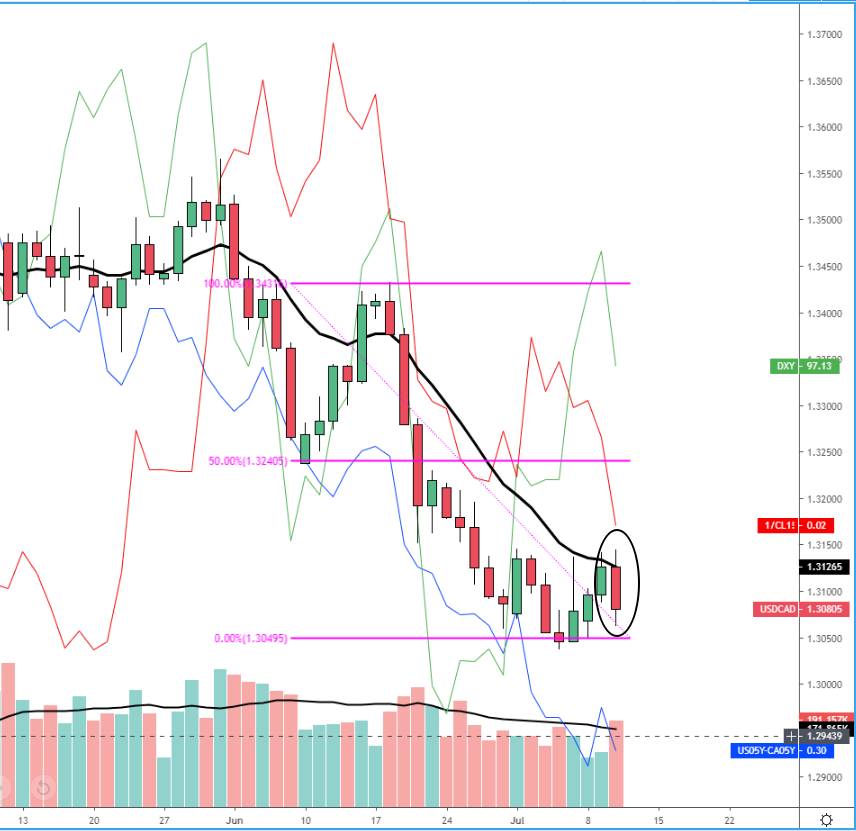

- The AUD holds firm undeterred by the decision by the RBA Board to slash interest rates for the second month in a row to a record low policy rate of 1.00% and signaled that the labour market continues to play a key role in adjusting monetary policy further if needed. The Central Bank didn’t rule out further rate cuts but it frankly did not provide sufficient evidence that it aims to cut again in the short-term, making its decision more labour data-dependant.

- RBA's Governor Philip Lowe, in Darwin, said that the recent rate cuts will help lower unemployment, reduce spare capacity while the Bank will closely monitor how things evolve over the coming months. Essentially sticking to the RBA statement script that further rate cuts will only come on a conditional basis if the labour market does not improve as envisioned. All else being equal, meaning no further deterioration in the economy or global trade conditions, the RBA’s back-to-back cuts may provide a cushion to stand pat until Q4 2019.

- Germany’s May retail sales fell by 0.6% vs +0.5% m/m expected, a major negative deviation that only comes to show the fragile state of affairs in the engine of growth for Europe.

- A report via Bloomberg notes that the ECB sees no need to rush into a July rate cut, preferring instead to wait for more data on the economy, citing officials familiar with the matter. Acting during the September meeting appears to be the options most endorsed as updated economic forecasts will be updated even if the report also speculates that tweak in the language may exist during the July meeting to set the stage for further easing as an imminent outcome.

- White House's trade advisor Navarro notes the US is headed in a very good direction on China. However, his language indicates no rush to readdress the key sticking points. Navarro said talks are the basis of current negotiations, but again, it will take time to get it right.

- Fed's Mester, who happens to defend a hawkish stance, told reports in London that she prefers not to cut rates proactively even if recognizing that recent mixed data suggest downside risks have risen with international trade policy a new source of uncertainty.

- EU leaders agreed to appoint Christine Lagarde to an 8-year term as next ECB President by replacing Mario Draghi, whose term at the helm of the Central Bank ends by the end of October. EU's Tusk also confirmed an agreement to appoint the EU Commission President to Ursula Von Der Leyen while Charles Michel for Council President Foreign policy chief.

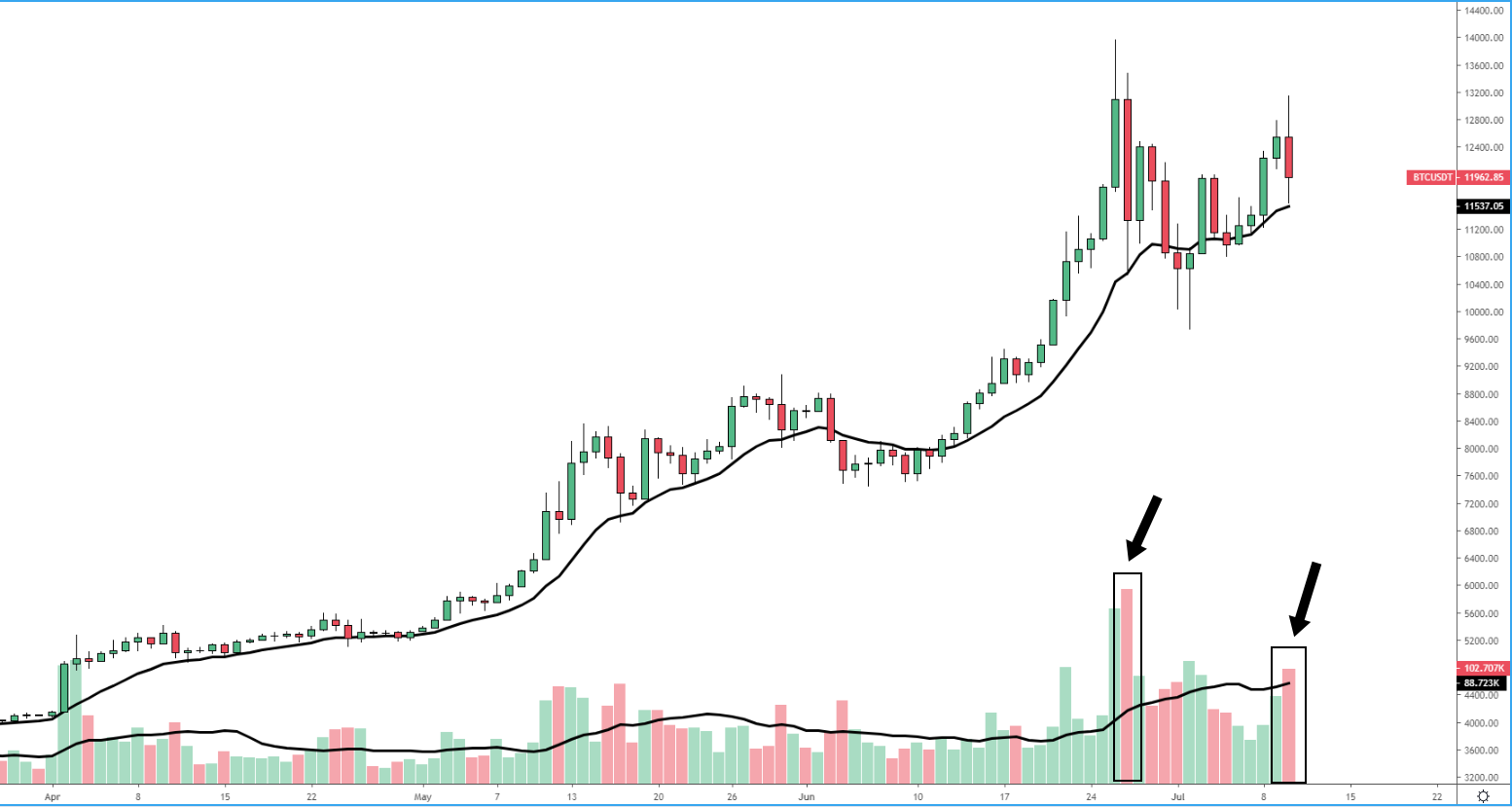

- Prime Factor Capital has been given the green light by the UK watchdog to become the first crypto hedge fund approved as a full-scope alternative investment fund manager. According to the report, the firm will be allowed to hold over 100m euros in assets under management. The price of Bitcoin has recovered back above 11k after the traders learned the bullish news.

- Despite news of a trade truce, including Trump now allowing on a strictly restrictive basis, for the Chinese tech giant Huawei to purchase equipment from US companies, news emerged that US government staff are still told to treat Huawei as blacklisted, Reuters reports.

RORO (Risk On, Risk Off Conditions)

Recent Economic Indicators & Events Ahead

Source: Forexfactory

A Dive Into Developments In FX (Technicals, Fundamentals, Intermarket)

EUR/USD: 100% Proj Target Pauses Move Down, Sellers Step In At Resistance

GBP/USD: Bearish Outlook Persists, Cluster Of Bids Found at Proj Target

AUD/USD: Looking Rather Expensive Based On Intermarket Flows

USD/JPY: Bullish Outlook Negated, Testing Critical Support

Crude Oil: Focus Clearly Shifts To Sell Rallies

Gold: Upside Breakout Of Descending Trendline In-Line w/ Main Technical Trend

Important Footnotes

- Risk model: The fact that financial markets have become so intertwined and dynamic makes it essential to stay constantly in tune with market conditions and adapt to new environments. This prop model will assist you to gauge the context that you are trading so that you can significantly reduce the downside risks. To understand the principles applied in the assessment of this model, refer to the tutorial How to Unpack Risk Sentiment Profiles

- Cycles: Markets evolve in cycles followed by a period of distribution and/or accumulation. To understand the principles applied in the assessment of cycles, refer to the tutorial How To Read Market Structures In Forex

- POC: It refers to the point of control. It represents the areas of most interest by trading volume and should act as walls of bids/offers that may result in price reversals. The volume profile analysis tracks trading activity over a specified time period at specified price levels. The study reveals the constant evolution of the market auction process. If you wish to find out more about the importance of the POC, refer to the tutorial How to Read Volume Profile Structures

- Tick Volume: Price updates activity provides great insights into the actual buy or sell-side commitment to be engaged into a specific directional movement. Studies validate that price updates (tick volume) are highly correlated to actual traded volume, with the correlation being very high, when looking at hourly data. If you wish to find out more about the importance tick volume, refer to the tutorial on Why Is Tick Volume Important To Monitor?

- Horizontal Support/Resistance: Unlike levels of dynamic support or resistance or more subjective measurements such as fibonacci retracements, pivot points, trendlines, or other forms of reactive areas, the horizontal lines of support and resistance are universal concepts used by the majority of market participants. It, therefore, makes the areas the most widely followed and relevant to monitor. The Ultimate Guide To Identify Areas Of High Interest In Any Market

- Trendlines: Besides the horizontal lines, trendlines are helpful as a visual representation of the trend. The trendlines are drawn respecting a series of rules that determine the validation of a new cycle being created. Therefore, these trendline drawn in the chart hinge to a certain interpretation of market structures.

- Correlations: Each forex pair has a series of highly correlated assets to assess valuations. This type of study is called inter-market analysis and it involves scoping out anomalies in the ever-evolving global interconnectivity between equities, bonds, currencies, and commodities. If you would like to understand more about this concept, refer to the tutorial How Divergence In Correlated Assets Can Help You Add An Edge.

- Fundamentals: It’s important to highlight that the daily market outlook provided in this report is subject to the impact of the fundamental news. Any unexpected news may cause the price to behave erratically in the short term.

- Projection Targets: The usefulness of the 100% projection resides in the symmetry and harmonic relationships of market cycles. By drawing a 100% projection, you can anticipate the area in the chart where some type of pause and potential reversals in price is likely to occur, due to 1. The side in control of the cycle takes profits 2. Counter-trend positions are added by contrarian players 3. These are price points where limit orders are set by market-makers. You can find out more by reading the tutorial on The Magical 100% Fibonacci Projection