IvanGlobalPrime

Company Representative

- Messages

- 36

Find my latest market thoughts

ECB Preview: Gauging QE2 Timing Is Key

Posted on: 25 Jul, 2019

The ECB monetary policy meeting takes center stage this Thursday. The real debate comes down to whether the Central Bank will take pre-emptive precautionary actions by slashing the deposit rate by 10bp to -50bp in today’s meeting or will prudence ensue by not getting involved in further easing until the new ECB macro projections are published.

The Daily Edge is authored by Ivan Delgado, Market Insights Commentator at Global Prime. The purpose of this content is to provide an assessment of the market conditions. The report takes an in-depth look of market dynamics, factoring in fundamentals, technicals, inter-market in order to determine daily biases and assist one’s decisions on a regular basis. Feel free to follow Ivan on Twitter & Youtube. You can also subscribe to the mailing list to receive Ivan’s Daily wrap.

The ECB monetary policy meeting takes center stage today. There are two debates at play. The first comes down to whether the Central Bank will take pre-emptive precautionary actions by slashing the deposit rate or will prudence ensue by not getting involved in further easing until the new ECB macro projections are published.

The second discourse, perhaps not as urgent to be delivered as the steps to properly formalize its commencement are yet to be telegraphed, involves the re-activation of asset purchases as part of a new stimulus package aimed at re-invigorating growth in the EU.

Rate cut: Will the ECB wait until Sept?

Out of all the bank research reports I get to scan daily, in particular, those concerning the ECB previews, the rationale I’ve observed by those calling for no explicit action this month is that historically, the ECB has had the tendency to act once new economic updates come due.

However, the preponderance of evidence is overwhelming in that macroeconomic conditions for further easing seem to have already been met. The question becomes if the ECB front-runs an anticipated downgrade in the Sept macroeconomic revisions, which at this point, stand rather unrealistic with the central bank models forecasting an acceleration in the pace of growth from the 2nd half of the year with a notable acceleration in core inflation.

Keeping in mind that the few forward-looking indicators for QE such as the ZEW survey in Germany have come weaker, that Wednesday’s miss in EZ PMIs became yet another warning, alongside this week’s ECB report highlighting credit standards for loans to firms as well as consumer credit and other lendings to households tightening in Q2, it continues to clearly flag the state of uncertainty in the Euro area as fears over the economic outlook mount.

The obvious deterioration in the EU economic conditions, surprisingly, has barely budged the survey published by Bloomberg, where over 87% of all the economists polled expect the ECB to hold rates unchanged even as the case for ECB to signal further easing has increased.

If one takes a look at the price action in the EUR index (equally-weighted vs G8 FX), we head into the ECB with a loss in the valuation of the currency of over 2% vs its main peers. This translates into a market that has aggressively discounted action by the ECB today.

There is no doubt that ECB President Draghi could cater a stance that would still resonate with further downside momentum, but whenever a critical event is due with such a consistent selling for over a month in the EUR index, we need to ask ourselves where the bar has been set.

I am personally of the opinion that the bar has been set quite high, in other words, Draghi should overdeliver unless the risk of a ‘sell the rumor, buy the fact’ in this case ensues. So, what exactly does the market need to see from the ECB to avoid a run to the exits in EUR shorts?

The ECB should get ahead of the curve by cutting its deposit rate by 10bp. Failure to do so would be an outcome I can’t see sellers latching on to sustain the downside even if Draghi does telegraph a change in the forward guidance on policy rates for an actual cut come Sept. That’s the first clear risk for the so far committed EUR sellers to have a rethink.

As part of the ECB’s policy rate guidance, if the bank cuts and still open the door for extra cuts, essentially hinting at a rate-cutting cycle, which I highly doubt they will commit to set a path, then there is definitely quite a lot to chew on for sellers to wash, rinse and repeat its bias.

To pre-announce that the rate cut coming is not a one-and-done, the ECB should message its forward guidance by removing the reference to mid-2020 and adding the possibility or lower levels. This is what it may sound like if the ECB is serious about hinting at a cycle of cuts.

"The Council now expects the key ECB interest rates to remain at present or lower levels for as long as necessary to ensure the continued sustained convergence of inflation…".

The timing of QE2 a key factor

A second debate that may not be as pressing as per the timing of delivery yet will have a major influence on EUR price action today orbits around the rhetoric to restart QE. This will involve an exercise by market speculators to immediately update the views on when the resumption of a stimulus package is likely. The more its proximity to be re-activated, the greater the case for the macro trade to still be selling EURs at attractive levels.

For the ECB to speed up its efforts towards QE II, there needs to be broad-based recognition that the protracted epidemic of chronic low inflation since the GFC is set to extend in time. The more it acknowledges this problem, the higher the risk that the ECB will restart net asset purchases earlier rather than later. The key question thus would be, how soon and how much?

On the hypothetical estimate of the size of the stimulus, my fear is that even if the ECB aims to bring the option to the table, the amount could be limited for now because consensus on a new round of net asset purchases won’t be easy to come by. The Presidency transition is another limitation to how much Draghi can commit before Lagarde takes the reins.

Before moving on, it’s important to remind the readership that a moment of reckoning for the ECB inflation mandate came to my attention last week. It was precisely this revelation, cited by Bloomberg, that makes me think the ECB has recognized the problem of persistently low inflation.

The moment I read that the ECB is considering to study a potential revamp of its inflation goal framework, with some of the ECB staff seemingly critics of the 'below, but close to 2%' definition as part of the mandate, my reaction was to think that the Central Bank is starting to make the admission to potentially pursue longer stimulus programs based on the acceptance of lower inflation projections. The immediate markdown in the EUR last week supports this notion.

Even if core inflationary measures have bounced of cyclical lows, the recovery has so far been marginal at best, and even more important, which is what may be causing this shift above, during the times when the EU GDP rose above trend, CPI was still low by historical standards.

What’s more, in September, the new projections by the ECB, set to be revised down, will most likely match suppressed growth levels and inflation to those before QE I in late 2014. Besides, market-based inflation expectations remain very low, which means that any long pause by the ECB without any immediate action to address this problem also raises concerns about its credibility

Granted, the market consensus, by reading over a dozen bank research reports, appears to be Q4 at the earliest or worst case, Q1 next year. This essentially gives some room (July or Sept) as the months the ECB could aim for to start implementing the new buying program.

But quite frankly, since the ECB has not been characterized to make such bold decisions without a prior formalized hint to the markets, it boils down to whether or not Draghi can give a sufficiently strong indication that QE2 is coming in September. This would still be music to the ears of EUR bears, who won’t get disappointed, as it’d come ahead of most views at this point.

If instead, QE2 is left to the newly appointed ECB President Lagarde to formalize and implement, which would not be an aberration to think about as she is the one set to take charge, it means the market may find that disappointing as that can’t happen until the November meeting.

I’ve skipped the October meeting as a strong consideration as I can’t sincerely picture Draghi inking the legal format of a QE2 program the same month he departs.

If history is any indication, while a marginal rate cut deeper into the negative plays a role in how the EUR can react to the ECB announcement today, the messaging around the likely future policy accommodation should prove more relevant as an influencer of the EUR pricing.

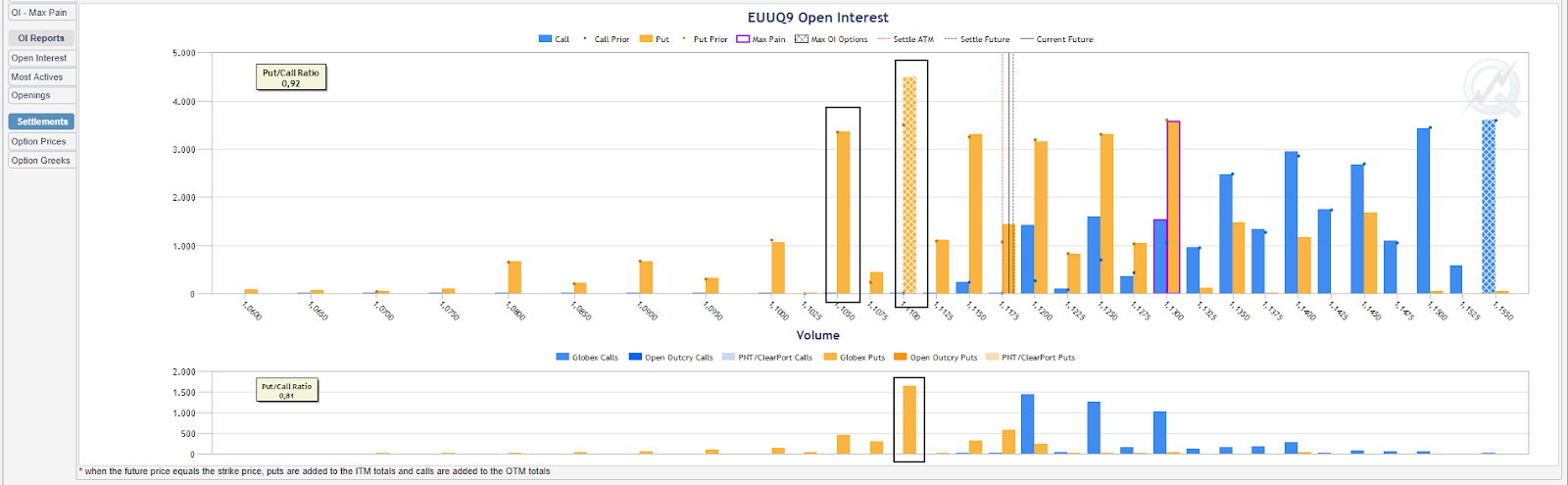

In terms of the key areas in the EUR/USD chart to keep in mind, find the chart below. The highlighted green refers to the areas where market participants in the EUR futures have allocated their maximum options exposure through OTM (out the money) Puts.

The area from 1.1050-1.11 in the Euro futures contract represents the line in the sand where the most bets have been placed, which suggests an increasing number of long EURUSD spot traders requite cheap protection as a dynamic stop loss in case long plays succumb.

Wrap up: Risk of disappointment runs high

A lot in today’s EUR price fluctuation will hinge on the prospects for a restart of QE2, with Sept the make or break month to kickstart the program to minimize disappointments. I have my reservations that the ECB can be prompt enough to recalibrate its communication to have QE2 it implemented by such date even if the evidence to act is mounting. I’ve always perceived the ECB like a slow-moving whale also tasked to properly prepare the market for when there is a critical sea change.

So, if today’s outcome offers strong hints that it won’t be until Lagarde is in command in November as I highly doubt the month of the Presidency transition (Oct) will be appropriate, I again have my doubts that a rate cut in July, let alone a pre-announcement for Sept, can avoid the unwinding of EUR shorts. So, as you can see, the hurdles to favor EUR shorts are there. Alternatively, if Draghi comes forward with a rate cut of 10bp to -50bp in the deposit rate and clarification ensues that QE2 is due by Sept, then EUR shorts remain a logic play.

ECB Preview: Gauging QE2 Timing Is Key

Posted on: 25 Jul, 2019

The ECB monetary policy meeting takes center stage this Thursday. The real debate comes down to whether the Central Bank will take pre-emptive precautionary actions by slashing the deposit rate by 10bp to -50bp in today’s meeting or will prudence ensue by not getting involved in further easing until the new ECB macro projections are published.

The Daily Edge is authored by Ivan Delgado, Market Insights Commentator at Global Prime. The purpose of this content is to provide an assessment of the market conditions. The report takes an in-depth look of market dynamics, factoring in fundamentals, technicals, inter-market in order to determine daily biases and assist one’s decisions on a regular basis. Feel free to follow Ivan on Twitter & Youtube. You can also subscribe to the mailing list to receive Ivan’s Daily wrap.

The ECB monetary policy meeting takes center stage today. There are two debates at play. The first comes down to whether the Central Bank will take pre-emptive precautionary actions by slashing the deposit rate or will prudence ensue by not getting involved in further easing until the new ECB macro projections are published.

The second discourse, perhaps not as urgent to be delivered as the steps to properly formalize its commencement are yet to be telegraphed, involves the re-activation of asset purchases as part of a new stimulus package aimed at re-invigorating growth in the EU.

Rate cut: Will the ECB wait until Sept?

Out of all the bank research reports I get to scan daily, in particular, those concerning the ECB previews, the rationale I’ve observed by those calling for no explicit action this month is that historically, the ECB has had the tendency to act once new economic updates come due.

However, the preponderance of evidence is overwhelming in that macroeconomic conditions for further easing seem to have already been met. The question becomes if the ECB front-runs an anticipated downgrade in the Sept macroeconomic revisions, which at this point, stand rather unrealistic with the central bank models forecasting an acceleration in the pace of growth from the 2nd half of the year with a notable acceleration in core inflation.

Keeping in mind that the few forward-looking indicators for QE such as the ZEW survey in Germany have come weaker, that Wednesday’s miss in EZ PMIs became yet another warning, alongside this week’s ECB report highlighting credit standards for loans to firms as well as consumer credit and other lendings to households tightening in Q2, it continues to clearly flag the state of uncertainty in the Euro area as fears over the economic outlook mount.

The obvious deterioration in the EU economic conditions, surprisingly, has barely budged the survey published by Bloomberg, where over 87% of all the economists polled expect the ECB to hold rates unchanged even as the case for ECB to signal further easing has increased.

If one takes a look at the price action in the EUR index (equally-weighted vs G8 FX), we head into the ECB with a loss in the valuation of the currency of over 2% vs its main peers. This translates into a market that has aggressively discounted action by the ECB today.

There is no doubt that ECB President Draghi could cater a stance that would still resonate with further downside momentum, but whenever a critical event is due with such a consistent selling for over a month in the EUR index, we need to ask ourselves where the bar has been set.

I am personally of the opinion that the bar has been set quite high, in other words, Draghi should overdeliver unless the risk of a ‘sell the rumor, buy the fact’ in this case ensues. So, what exactly does the market need to see from the ECB to avoid a run to the exits in EUR shorts?

The ECB should get ahead of the curve by cutting its deposit rate by 10bp. Failure to do so would be an outcome I can’t see sellers latching on to sustain the downside even if Draghi does telegraph a change in the forward guidance on policy rates for an actual cut come Sept. That’s the first clear risk for the so far committed EUR sellers to have a rethink.

As part of the ECB’s policy rate guidance, if the bank cuts and still open the door for extra cuts, essentially hinting at a rate-cutting cycle, which I highly doubt they will commit to set a path, then there is definitely quite a lot to chew on for sellers to wash, rinse and repeat its bias.

To pre-announce that the rate cut coming is not a one-and-done, the ECB should message its forward guidance by removing the reference to mid-2020 and adding the possibility or lower levels. This is what it may sound like if the ECB is serious about hinting at a cycle of cuts.

"The Council now expects the key ECB interest rates to remain at present or lower levels for as long as necessary to ensure the continued sustained convergence of inflation…".

The timing of QE2 a key factor

A second debate that may not be as pressing as per the timing of delivery yet will have a major influence on EUR price action today orbits around the rhetoric to restart QE. This will involve an exercise by market speculators to immediately update the views on when the resumption of a stimulus package is likely. The more its proximity to be re-activated, the greater the case for the macro trade to still be selling EURs at attractive levels.

For the ECB to speed up its efforts towards QE II, there needs to be broad-based recognition that the protracted epidemic of chronic low inflation since the GFC is set to extend in time. The more it acknowledges this problem, the higher the risk that the ECB will restart net asset purchases earlier rather than later. The key question thus would be, how soon and how much?

On the hypothetical estimate of the size of the stimulus, my fear is that even if the ECB aims to bring the option to the table, the amount could be limited for now because consensus on a new round of net asset purchases won’t be easy to come by. The Presidency transition is another limitation to how much Draghi can commit before Lagarde takes the reins.

Before moving on, it’s important to remind the readership that a moment of reckoning for the ECB inflation mandate came to my attention last week. It was precisely this revelation, cited by Bloomberg, that makes me think the ECB has recognized the problem of persistently low inflation.

The moment I read that the ECB is considering to study a potential revamp of its inflation goal framework, with some of the ECB staff seemingly critics of the 'below, but close to 2%' definition as part of the mandate, my reaction was to think that the Central Bank is starting to make the admission to potentially pursue longer stimulus programs based on the acceptance of lower inflation projections. The immediate markdown in the EUR last week supports this notion.

Even if core inflationary measures have bounced of cyclical lows, the recovery has so far been marginal at best, and even more important, which is what may be causing this shift above, during the times when the EU GDP rose above trend, CPI was still low by historical standards.

What’s more, in September, the new projections by the ECB, set to be revised down, will most likely match suppressed growth levels and inflation to those before QE I in late 2014. Besides, market-based inflation expectations remain very low, which means that any long pause by the ECB without any immediate action to address this problem also raises concerns about its credibility

Granted, the market consensus, by reading over a dozen bank research reports, appears to be Q4 at the earliest or worst case, Q1 next year. This essentially gives some room (July or Sept) as the months the ECB could aim for to start implementing the new buying program.

But quite frankly, since the ECB has not been characterized to make such bold decisions without a prior formalized hint to the markets, it boils down to whether or not Draghi can give a sufficiently strong indication that QE2 is coming in September. This would still be music to the ears of EUR bears, who won’t get disappointed, as it’d come ahead of most views at this point.

If instead, QE2 is left to the newly appointed ECB President Lagarde to formalize and implement, which would not be an aberration to think about as she is the one set to take charge, it means the market may find that disappointing as that can’t happen until the November meeting.

I’ve skipped the October meeting as a strong consideration as I can’t sincerely picture Draghi inking the legal format of a QE2 program the same month he departs.

If history is any indication, while a marginal rate cut deeper into the negative plays a role in how the EUR can react to the ECB announcement today, the messaging around the likely future policy accommodation should prove more relevant as an influencer of the EUR pricing.

In terms of the key areas in the EUR/USD chart to keep in mind, find the chart below. The highlighted green refers to the areas where market participants in the EUR futures have allocated their maximum options exposure through OTM (out the money) Puts.

The area from 1.1050-1.11 in the Euro futures contract represents the line in the sand where the most bets have been placed, which suggests an increasing number of long EURUSD spot traders requite cheap protection as a dynamic stop loss in case long plays succumb.

Wrap up: Risk of disappointment runs high

A lot in today’s EUR price fluctuation will hinge on the prospects for a restart of QE2, with Sept the make or break month to kickstart the program to minimize disappointments. I have my reservations that the ECB can be prompt enough to recalibrate its communication to have QE2 it implemented by such date even if the evidence to act is mounting. I’ve always perceived the ECB like a slow-moving whale also tasked to properly prepare the market for when there is a critical sea change.

So, if today’s outcome offers strong hints that it won’t be until Lagarde is in command in November as I highly doubt the month of the Presidency transition (Oct) will be appropriate, I again have my doubts that a rate cut in July, let alone a pre-announcement for Sept, can avoid the unwinding of EUR shorts. So, as you can see, the hurdles to favor EUR shorts are there. Alternatively, if Draghi comes forward with a rate cut of 10bp to -50bp in the deposit rate and clarification ensues that QE2 is due by Sept, then EUR shorts remain a logic play.