Sive Morten

Special Consultant to the FPA

- Messages

- 18,644

Fundamentals

Gold this week shows stronger performance than any currency, even on background of positive US statistics. This just confirms some specific features of the gold metal that currently stands in most favorite position. Whatever happens in the US in near term - both scenarios will not make any devastating effect on gold demand. Keeping rates at high level supports deterioration of the US economy conditions with near negative real rates at the same time. Recession spooks investors, rising demand for the gold. While starting of new Fed easing policy on a background of still high inflation will spin it up, pushing real rates even lower. Thus, whatever negative effect might happen when decisions will be made - it probably will be short lasting.

Market overview

Gold steadied on Friday with gains capped by a stronger dollar, but the metal was still set for a sixth straight weekly rise ahead of the U.S. Federal Reserve's rate decision next week. Spot gold edged up 0.1% to $1,931.61 per ounce, yet gave up gains earlier in the session after data showed U.S. consumer spending fell in December, even as the core personal consumer expenditure index gained 0.3% month-on-month.

Data on Thursday showed the U.S. economy grew faster than expected, causing gold to retreat more than 1%. The weak handover to 2023 raises the risks of a recession by the second half of the year, but also reduces the need for the Fed to maintain its overly aggressive monetary policy. Fed policymakers have signalled they expect rates ultimately to go a bit higher - to just over 5% - while traders are looking out for a terminal rate of 4.9% in June. A quarter-basis-point rate hike has been priced in by most.

In our recent FX report we've considered 3rd side look at the US economy situation, compared it with our long-term analysis and made corresponding conclusions. Here, just to not repeat the same things, we take a look at two important events. First is - whether recent positive shifts are enough to avoid "hard landing" and could decrease of M2 money supply provide improvement in economy.

You do know our view, that strong job market (which is mostly inflationary), decreasing of CPI/PPI numbers, stable consumption currently are not enough to make conclusion that US has avoided recession. Many indicators are lagging behind current situation. The total effect of 5% Fed rate will come only closer to the summer. Decreasing of inflation means as slowdown of economy (as we see in Real Estate sector) as its restructuring when nominal level is converging to core inflation. Other indicators by our view point that recession is inevitable.

Meantime, we're not alone with this view. Not only big banks, such as Black Rock, Nomura and some others point on this thing, but take a look, Fathom consulting tells the same.

With headline and core inflation now slowing, it seems as if the worst of the first-round inflationary shocks are probably over. Investors concur, with positive returns on bonds and equities so far this year, and lower market-implied risks of crises. Nevertheless, Fathom’s central forecast is still that the UK, euro area (EA) and the US will experience mild recessions in the coming year.

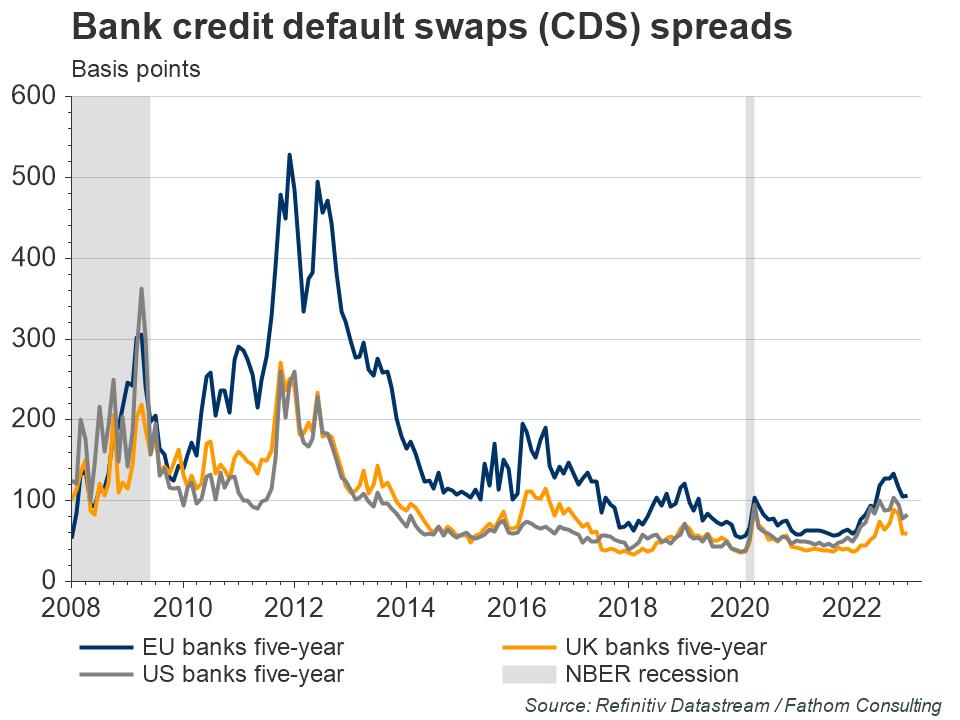

Indeed, long-only portfolios, which are especially volatile during economic downturns, were hit badly in 2022, but have since recovered as markets have grown more optimistic about the future. This is based upon an expectation that we have now passed the worst of the trade-off between growth and the inflation. Fathom’s Financial Vulnerability Indicator, a comprehensive measure of financial risk across 176 countries, shows that the risk of a global outbreak of banking crises peaked in 2022 Q3. Credit default swap spreads are also narrowing, reflecting lower risk of default.

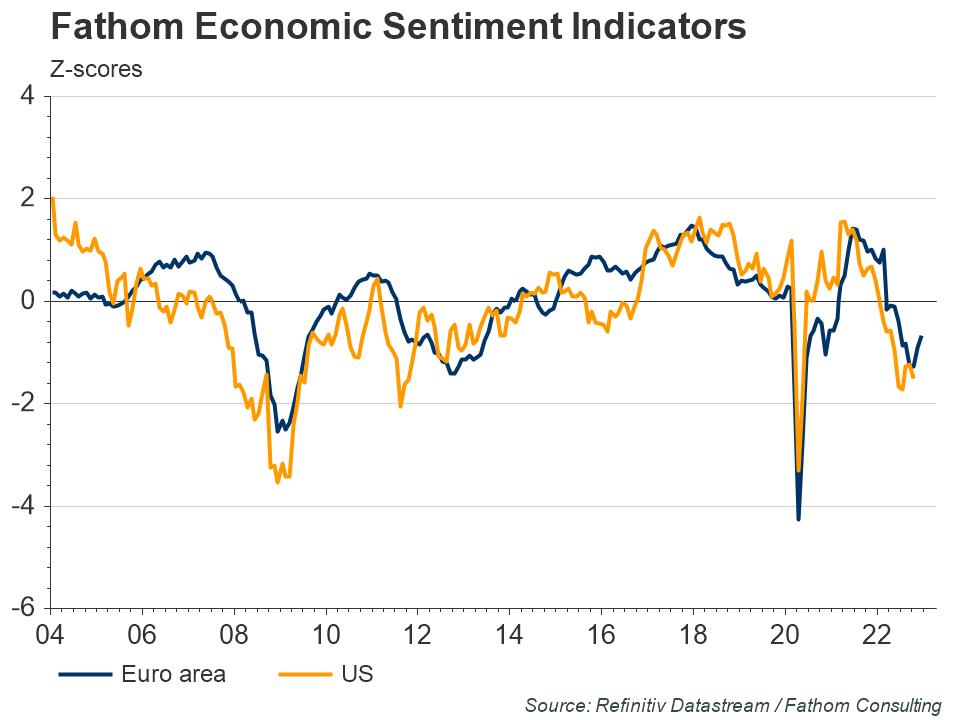

Fathom’s economic sentiment indicators have improved too but remain at low levels. Furthermore, the euro area composite PMI was above 50 for the first time since last June (a level above 50 indicates an expansion in business activity).

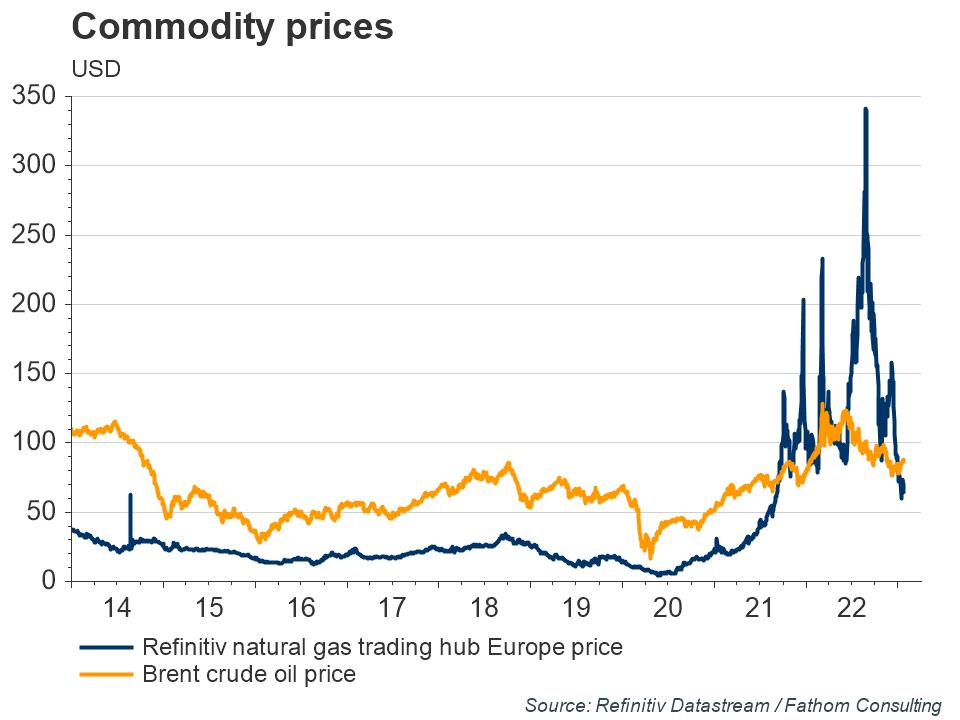

The optimistic news laid out above partly stems from lower oil and natural gas prices. Both remain elevated, but are decreasing. If European natural gas stocks hold, which according to Fathom’s central case they will, the worst of the first-round effects are now behind us. Indeed, the extent and speed of Europe’s substitution away from Russian gas generally exceeded expectations last year.

Although inflation rates are elevated across the OECD, in Fathom’s central forecast both headline and core inflation will slow this year. Indeed, headline outturns in both the US and euro area have surprised to the downside compared to the Reuters poll of professional forecasters’ expectations for the last few months.

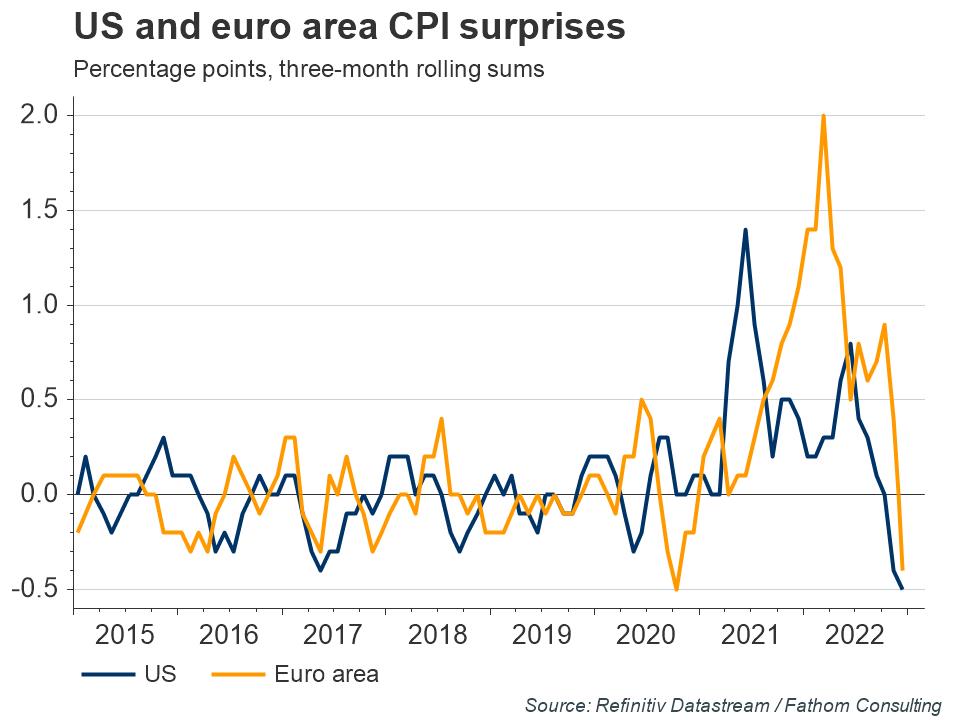

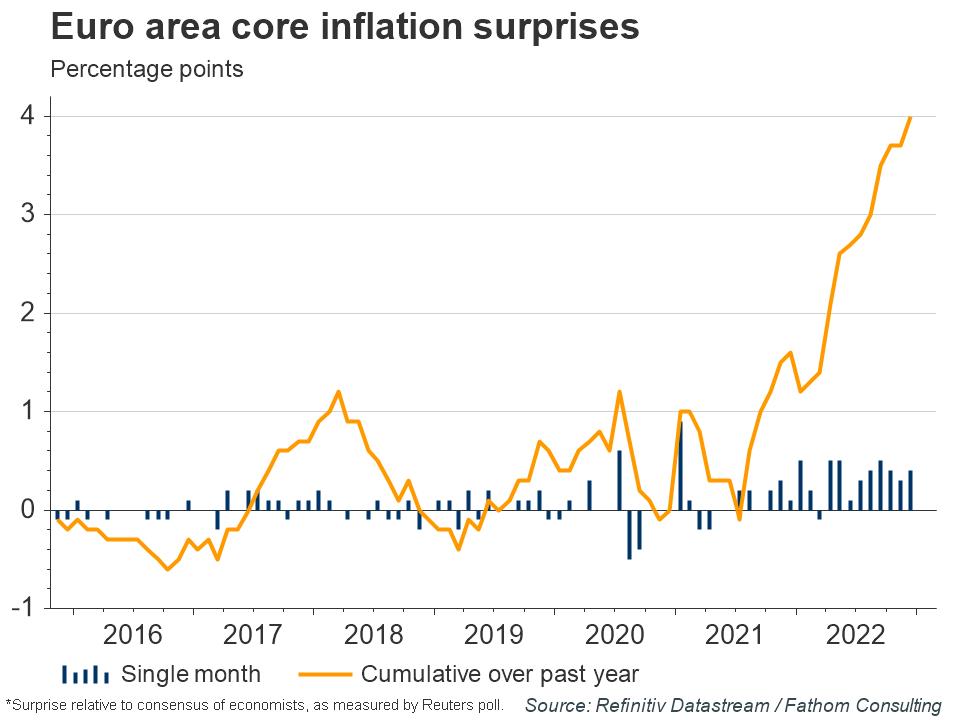

However, the core CPI surprises indicator is still elevated in the euro area, with little sign of waning yet. This could indicate that second-round effects are greater than anticipated by forecasters, and it points to a risk that inflation may prove more persistent than many expect. If this proves true, then policy may have to be tightened by more than is currently priced in.

There is a time lag of up to a year, or more, from when monetary tightening is implemented to the full effects being seen on economic activity; thus, monetary tightening in 2022 will still be acting as a brake on economic activity in 2023. Additionally, data suggest there is a chance of rising second-round effects through wages, profits and other nominal quantities, particularly in the euro area.

To summarise, the worst of the first-round effects seem to be in the past, market sentiments are looking brighter and inflation is slowing, but risks still persist. Fathom’s central case remains that the euro area will experience a recession within the coming two quarters, and the US later in the year. On the bright side, the downturn will not be near the levels seen during COVID.

M2 Supply effect

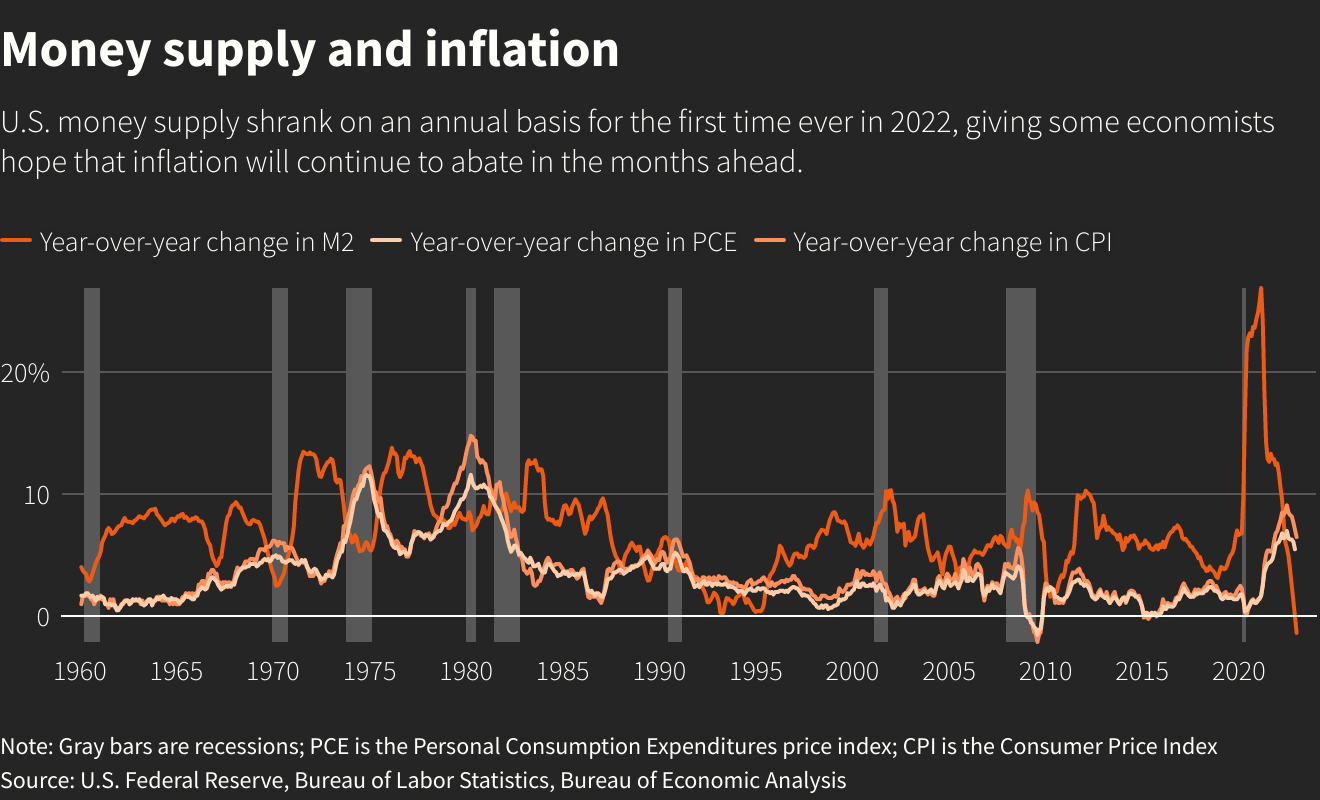

Now it is widely discussing effect of nominal M2 decreasing, which has happened for the first time since 1930. M2 has contracted for 1.3%. The question is could it have positive effect on inflation and boost Fed rate effect to let him defeat inflation faster. Let's start first with our personal view. We think that hardly this will happen by few reasons. First is, money supply is just a single component, we need to take a look at money turnover ratio to make conclusion on how it impacts on economy. Because decrease of money supply might be an effect of faster money turnover.

Second - M2 money supply is a pure fiscal measure. If, say, money supply indeed was cut by Fed, it could be replaced with loans, which is not monetary but credit emission. In this case it will have no impact on inflation. We're tending to this latter opinion. Previously we already have shown you the distortion in banking sector, where commercial deposit rates are few times lower than Fed rate. This is because banks have accumulated huge excess liquidity during Covid period, on multi -trillion government stimulus to population. At the final point they come to deposit accounts in banks. These low rates deposit let banks to accelerate loans providing with rates below Fed ones and replace bond issues. Which actually we see in reality. That's why we have doubts that contraction of M2 will make any visible effect on inflation rate any time soon.

Still, here is the common idea. Historically M2 has relation with CPI Index:

M2 took off in March 2020 as the Fed slashed rates and started buying trillions of dollars in bonds to help support the economy as the coronavirus pandemic started, ultimately mushrooming by $6.3 trillion - a 40% increase - from its level right before the start of the crisis. The recent decline in the money supply comes as the Fed has been aggressively raising rates to push inflation back to its 2% target. Since last June, it has also cut its holdings of Treasury and mortgage bonds by $400 billion to roughly $8.5 trillion to augment that process, further stripping the economy of financial liquidity.

Money-supply purists have long argued that the country's ever-growing stock of money was an inflation powder keg. It's an argument that lost credibility with policymakers in the record-long economic expansion before the pandemic when M2 rose by more than 80% but inflation never rose sustainably above the Fed's 2% target and spent much of that decade notably below it.

That dynamic changed in the last two years, though, with money supply trends moving in roughly the same direction as inflation pressures: As money supply rose rapidly into early 2022, so did inflation; since M2 started a persistent decline last summer, inflation pressures have also receded.

Economists, meanwhile, are still taking on board whether money supply is something they need to pay greater mind to as they contemplate monetary policy and inflation.

Conclusion

As you do know our fundamental view, let's not repeat it once again here but better let's focus on Fathom consulting view and opinion of respectable economists who suggest longer term for high inflation. In particular - Wells Fargo:

Bank of America:

Nomura Securities:

BlackRock:

Neuberger Berman sees the S&P 500 dropping to as low as 3,000 this year - a decline of nearly 25% from its current level - as rebounding inflation forces the Fed to become more aggressive.

Finally, statistically according to the ECB, the impact on inflation of a 1% increase in rates reaches its peak in the second year after the policy change. Therefore, interest rate hikes in 2022 will continue to affect economic activity into 2023 and beyond.

Somehow nobody speaks about decreasing of CPI, strong job market, consumption and other positive issues but point on stubborn inflation and longer-term for high rates. Compares to Fathom view, I see only single agreement, where they said -

Big banks mostly speak about this phenomenon, (as we do). It could mean only one thing - speaking conservatively, core inflation remains above 2% for a long time. Although in 2023 we suggest it should be above 4%. This inflation level doesn't let Fed to cut the rate any time soon. In turn, it means that we get more signs of economy depression, because high rates depress economical activity. There are three painful points in economy exist that could not hold the burden of high rates for too long. First is Real Estate market that is already crushing, second - US consumer loans and real wages that already behind the inflation ratio and third - Fed cash reserves that are melting very fast.

But, as Fathom consulting as mentioned big banks clearly hint on stronger and longer inflation than widely anticipated. Using just a simple logic, it leads to only one possible condition - Fed 100% should come to the moment when it can't hold high interest rates any more (painful points above) but inflation remains high. And this combination puts Gold market in advantage condition. Thus, we anticipate great time for gold market in nearest few years and wouldn't be surprised too much if it rises 1.5-2 times in price. And here we do not take into consideration political and other issues.

Technicals

Monthly

It seems that monthly trend has turned bullish on gold. Market has to close above $1848 level in January to confirm it. And probably it will be done. Here we see achievement of our major point - reaching of monthly overbought area. As a rule this level could delay upward trend for a long time. And only some big either political or economical event could push gold through this level. Financial markets are more sensitive to OB/OS condition, while gold and other commodities could stay at overbought or even slightly penetrate it for longer time - just take a look at previous peak around 2035$. So it is yet to see how gold response to $1945-1950 aea.

The one conclusion that we could make - no new longs on daily and higher time frames by far. As market has no Fib levels above, after overbought level will be normalized, 2057 YPR1 seems as most probable next target here.

Weekly

Trend is bullish here, no overbought. Market has formed indecision trading week, mostly the same like on EUR. It has clear XOP target around 2002$ area, but something really important has to happen to let market to reach it and to ignore monthly OB area. Because on calm market, monthly overbought doesn't let price to pass this 50$. Upside thrust looks great, so, as on EUR, here we also could watch for possible DiNapoli directional patterns.

Daily

Nothing interesting by far. Trend has turned bearish, so we do not consider new longs here. But buyers activity is still strong - take a look at downside spikes through the previous week. Any minor retracement was bought out. Here we consider 1900 area and Oversold as nearest destination point.

Intraday

Here we could either watch for some bigger scale pattern, such as potential H&S pattern on 4H chart. Divergence stands in place and suggests drop down to 1900$ area by the way:

Or, try to catch minor bearish continuation pattern on 1H chart. This could significantly minimize the risk. For example, we have bullish grabber, so upward bounce could be either in shape of AB-CD pattern or butterfly. So, potentially around 1940 area:

Gold this week shows stronger performance than any currency, even on background of positive US statistics. This just confirms some specific features of the gold metal that currently stands in most favorite position. Whatever happens in the US in near term - both scenarios will not make any devastating effect on gold demand. Keeping rates at high level supports deterioration of the US economy conditions with near negative real rates at the same time. Recession spooks investors, rising demand for the gold. While starting of new Fed easing policy on a background of still high inflation will spin it up, pushing real rates even lower. Thus, whatever negative effect might happen when decisions will be made - it probably will be short lasting.

Market overview

Gold steadied on Friday with gains capped by a stronger dollar, but the metal was still set for a sixth straight weekly rise ahead of the U.S. Federal Reserve's rate decision next week. Spot gold edged up 0.1% to $1,931.61 per ounce, yet gave up gains earlier in the session after data showed U.S. consumer spending fell in December, even as the core personal consumer expenditure index gained 0.3% month-on-month.

"[The Fed] needs to be convinced and their favourite indicators are showing inflation is cooling, but I think there still needs to be a bit more work done," said Edward Moya, senior market analyst at OANDA. The market was still good for gold as a recession would be bullish, and bullion could still thrive in a smaller-rate-hike environment, Moya added.

Data on Thursday showed the U.S. economy grew faster than expected, causing gold to retreat more than 1%. The weak handover to 2023 raises the risks of a recession by the second half of the year, but also reduces the need for the Fed to maintain its overly aggressive monetary policy. Fed policymakers have signalled they expect rates ultimately to go a bit higher - to just over 5% - while traders are looking out for a terminal rate of 4.9% in June. A quarter-basis-point rate hike has been priced in by most.

In our recent FX report we've considered 3rd side look at the US economy situation, compared it with our long-term analysis and made corresponding conclusions. Here, just to not repeat the same things, we take a look at two important events. First is - whether recent positive shifts are enough to avoid "hard landing" and could decrease of M2 money supply provide improvement in economy.

You do know our view, that strong job market (which is mostly inflationary), decreasing of CPI/PPI numbers, stable consumption currently are not enough to make conclusion that US has avoided recession. Many indicators are lagging behind current situation. The total effect of 5% Fed rate will come only closer to the summer. Decreasing of inflation means as slowdown of economy (as we see in Real Estate sector) as its restructuring when nominal level is converging to core inflation. Other indicators by our view point that recession is inevitable.

Meantime, we're not alone with this view. Not only big banks, such as Black Rock, Nomura and some others point on this thing, but take a look, Fathom consulting tells the same.

With headline and core inflation now slowing, it seems as if the worst of the first-round inflationary shocks are probably over. Investors concur, with positive returns on bonds and equities so far this year, and lower market-implied risks of crises. Nevertheless, Fathom’s central forecast is still that the UK, euro area (EA) and the US will experience mild recessions in the coming year.

Indeed, long-only portfolios, which are especially volatile during economic downturns, were hit badly in 2022, but have since recovered as markets have grown more optimistic about the future. This is based upon an expectation that we have now passed the worst of the trade-off between growth and the inflation. Fathom’s Financial Vulnerability Indicator, a comprehensive measure of financial risk across 176 countries, shows that the risk of a global outbreak of banking crises peaked in 2022 Q3. Credit default swap spreads are also narrowing, reflecting lower risk of default.

Fathom’s economic sentiment indicators have improved too but remain at low levels. Furthermore, the euro area composite PMI was above 50 for the first time since last June (a level above 50 indicates an expansion in business activity).

The optimistic news laid out above partly stems from lower oil and natural gas prices. Both remain elevated, but are decreasing. If European natural gas stocks hold, which according to Fathom’s central case they will, the worst of the first-round effects are now behind us. Indeed, the extent and speed of Europe’s substitution away from Russian gas generally exceeded expectations last year.

Although inflation rates are elevated across the OECD, in Fathom’s central forecast both headline and core inflation will slow this year. Indeed, headline outturns in both the US and euro area have surprised to the downside compared to the Reuters poll of professional forecasters’ expectations for the last few months.

However, the core CPI surprises indicator is still elevated in the euro area, with little sign of waning yet. This could indicate that second-round effects are greater than anticipated by forecasters, and it points to a risk that inflation may prove more persistent than many expect. If this proves true, then policy may have to be tightened by more than is currently priced in.

There is a time lag of up to a year, or more, from when monetary tightening is implemented to the full effects being seen on economic activity; thus, monetary tightening in 2022 will still be acting as a brake on economic activity in 2023. Additionally, data suggest there is a chance of rising second-round effects through wages, profits and other nominal quantities, particularly in the euro area.

To summarise, the worst of the first-round effects seem to be in the past, market sentiments are looking brighter and inflation is slowing, but risks still persist. Fathom’s central case remains that the euro area will experience a recession within the coming two quarters, and the US later in the year. On the bright side, the downturn will not be near the levels seen during COVID.

M2 Supply effect

Now it is widely discussing effect of nominal M2 decreasing, which has happened for the first time since 1930. M2 has contracted for 1.3%. The question is could it have positive effect on inflation and boost Fed rate effect to let him defeat inflation faster. Let's start first with our personal view. We think that hardly this will happen by few reasons. First is, money supply is just a single component, we need to take a look at money turnover ratio to make conclusion on how it impacts on economy. Because decrease of money supply might be an effect of faster money turnover.

Second - M2 money supply is a pure fiscal measure. If, say, money supply indeed was cut by Fed, it could be replaced with loans, which is not monetary but credit emission. In this case it will have no impact on inflation. We're tending to this latter opinion. Previously we already have shown you the distortion in banking sector, where commercial deposit rates are few times lower than Fed rate. This is because banks have accumulated huge excess liquidity during Covid period, on multi -trillion government stimulus to population. At the final point they come to deposit accounts in banks. These low rates deposit let banks to accelerate loans providing with rates below Fed ones and replace bond issues. Which actually we see in reality. That's why we have doubts that contraction of M2 will make any visible effect on inflation rate any time soon.

Still, here is the common idea. Historically M2 has relation with CPI Index:

M2 took off in March 2020 as the Fed slashed rates and started buying trillions of dollars in bonds to help support the economy as the coronavirus pandemic started, ultimately mushrooming by $6.3 trillion - a 40% increase - from its level right before the start of the crisis. The recent decline in the money supply comes as the Fed has been aggressively raising rates to push inflation back to its 2% target. Since last June, it has also cut its holdings of Treasury and mortgage bonds by $400 billion to roughly $8.5 trillion to augment that process, further stripping the economy of financial liquidity.

Money-supply purists have long argued that the country's ever-growing stock of money was an inflation powder keg. It's an argument that lost credibility with policymakers in the record-long economic expansion before the pandemic when M2 rose by more than 80% but inflation never rose sustainably above the Fed's 2% target and spent much of that decade notably below it.

That dynamic changed in the last two years, though, with money supply trends moving in roughly the same direction as inflation pressures: As money supply rose rapidly into early 2022, so did inflation; since M2 started a persistent decline last summer, inflation pressures have also receded.

M2 “exploded during the pandemic, and correctly predicted that we would get inflation,” Federal Reserve Bank of St. Louis President James Bullard, an early proponent of policy tightening, said earlier this month. “Inflation is certainly a monetary phenomenon” and “when you get a huge movement in money, then you do get the movement in inflation,” as was seen in the 1960s, ‘70s and ‘80s.

Economists, meanwhile, are still taking on board whether money supply is something they need to pay greater mind to as they contemplate monetary policy and inflation.

"I think that what we are finding is that the relationship between changes in the money supply and inflation is far less linear" than had been previously understood, said Thomas Simons, economist with investment bank Jefferies. It appears the Fed’s aggressive balance sheet expansion during the pandemic did have a bigger impact on inflation relative to recent decades.

Conclusion

As you do know our fundamental view, let's not repeat it once again here but better let's focus on Fathom consulting view and opinion of respectable economists who suggest longer term for high inflation. In particular - Wells Fargo:

“Money is dying to get back into this market but we still think you get an economic slowdown and that earnings expectations are still too high,” said Paul Christopher, head of global investment strategy at the Wells Fargo Investment Institute.

Bank of America:

The outlook of dovish Fed policy that rate peaks under 5% is not shared by BoFA’s strategists, who recommended positions that would benefit from a “grind lower” in U.S. equities, noting that Fed "cutting cycles in history have almost exclusively been associated with either a recession ... or a financial accident," they said.

Nomura Securities:

"You are now getting the disinflationary impulse that the Fed has been seeking and it's moving ahead of schedule. Now the challenge is that people are under-positioned and are ... absolutely being forced into a painful trade because the Fed hasn't won the fight yet."

BlackRock:

The current stock rally “hints at how markets will likely react once inflation eases and rate hikes pause,” wrote analysts at BlackRock, the world’s largest asset manager, earlier this week. “Before this outlook becomes reality, we see (developed market) stocks falling when recessions we expect manifest.”

Neuberger Berman sees the S&P 500 dropping to as low as 3,000 this year - a decline of nearly 25% from its current level - as rebounding inflation forces the Fed to become more aggressive.

Finally, statistically according to the ECB, the impact on inflation of a 1% increase in rates reaches its peak in the second year after the policy change. Therefore, interest rate hikes in 2022 will continue to affect economic activity into 2023 and beyond.

Somehow nobody speaks about decreasing of CPI, strong job market, consumption and other positive issues but point on stubborn inflation and longer-term for high rates. Compares to Fathom view, I see only single agreement, where they said -

the core CPI surprises indicator is still elevated in the euro area, with little sign of waning yet. This could indicate that second-round effects are greater than anticipated by forecasters, and it points to a risk that inflation may prove more persistent than many expect. If this proves true, then policy may have to be tightened by more than is currently priced in.

Big banks mostly speak about this phenomenon, (as we do). It could mean only one thing - speaking conservatively, core inflation remains above 2% for a long time. Although in 2023 we suggest it should be above 4%. This inflation level doesn't let Fed to cut the rate any time soon. In turn, it means that we get more signs of economy depression, because high rates depress economical activity. There are three painful points in economy exist that could not hold the burden of high rates for too long. First is Real Estate market that is already crushing, second - US consumer loans and real wages that already behind the inflation ratio and third - Fed cash reserves that are melting very fast.

But, as Fathom consulting as mentioned big banks clearly hint on stronger and longer inflation than widely anticipated. Using just a simple logic, it leads to only one possible condition - Fed 100% should come to the moment when it can't hold high interest rates any more (painful points above) but inflation remains high. And this combination puts Gold market in advantage condition. Thus, we anticipate great time for gold market in nearest few years and wouldn't be surprised too much if it rises 1.5-2 times in price. And here we do not take into consideration political and other issues.

Technicals

Monthly

It seems that monthly trend has turned bullish on gold. Market has to close above $1848 level in January to confirm it. And probably it will be done. Here we see achievement of our major point - reaching of monthly overbought area. As a rule this level could delay upward trend for a long time. And only some big either political or economical event could push gold through this level. Financial markets are more sensitive to OB/OS condition, while gold and other commodities could stay at overbought or even slightly penetrate it for longer time - just take a look at previous peak around 2035$. So it is yet to see how gold response to $1945-1950 aea.

The one conclusion that we could make - no new longs on daily and higher time frames by far. As market has no Fib levels above, after overbought level will be normalized, 2057 YPR1 seems as most probable next target here.

Weekly

Trend is bullish here, no overbought. Market has formed indecision trading week, mostly the same like on EUR. It has clear XOP target around 2002$ area, but something really important has to happen to let market to reach it and to ignore monthly OB area. Because on calm market, monthly overbought doesn't let price to pass this 50$. Upside thrust looks great, so, as on EUR, here we also could watch for possible DiNapoli directional patterns.

Daily

Nothing interesting by far. Trend has turned bearish, so we do not consider new longs here. But buyers activity is still strong - take a look at downside spikes through the previous week. Any minor retracement was bought out. Here we consider 1900 area and Oversold as nearest destination point.

Intraday

Here we could either watch for some bigger scale pattern, such as potential H&S pattern on 4H chart. Divergence stands in place and suggests drop down to 1900$ area by the way:

Or, try to catch minor bearish continuation pattern on 1H chart. This could significantly minimize the risk. For example, we have bullish grabber, so upward bounce could be either in shape of AB-CD pattern or butterfly. So, potentially around 1940 area: