tickmill-news

Tickmill Representative

- Messages

- 79

Negative Headlines Grab Markets’ Attention as Equity Rally Stalls

There are convincing signs that the rally on equity markets has stalled in the second half of this week. European indices gained less than 1% on Friday attempting to price in some early positive developments in coronavirus trends. There is not much to rally on in the short term, while increasing number of negative headlines feeds cautious state of the markets. The NYC authorities are mulling over extension of restrictions after closing schools as the mayor of the city de Blasio said that restaurants could be closed within the next week or two. Another heavy blow of economic activity in the US which the markets have not yet fully absorbed.

US Treasury Chief Mnuchin said that the $ 4.5 trillion emergency lending programs, which expire at the end of this year, won’t be extended. The Fed loses significant potential to absorb toxic debt in the event of a new shock, while medium-sized businesses lose access to direct loans from the Central Bank (through the Main Street lending program). However, it is possible that the proceeds will be used by Congress to fund other programs.

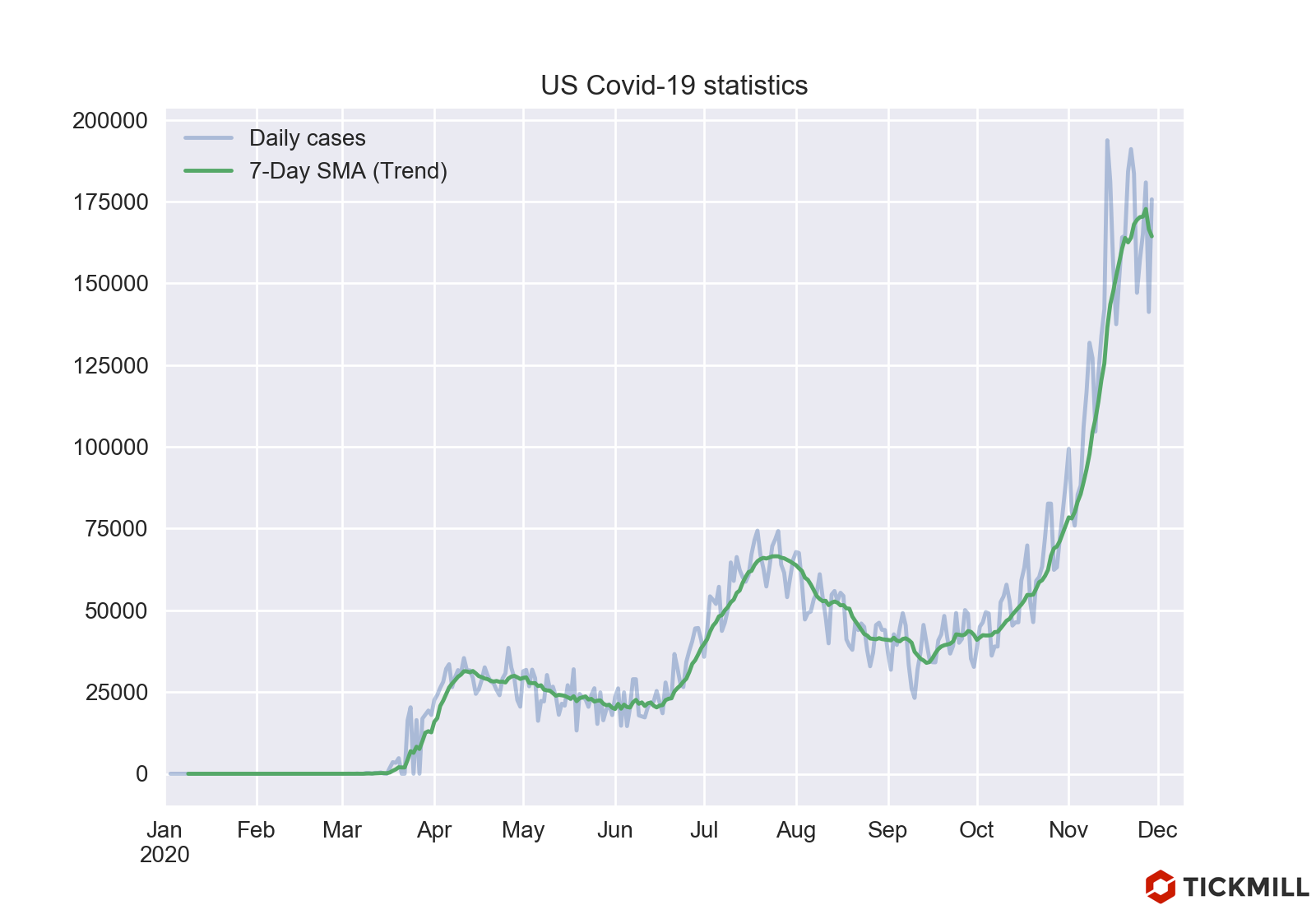

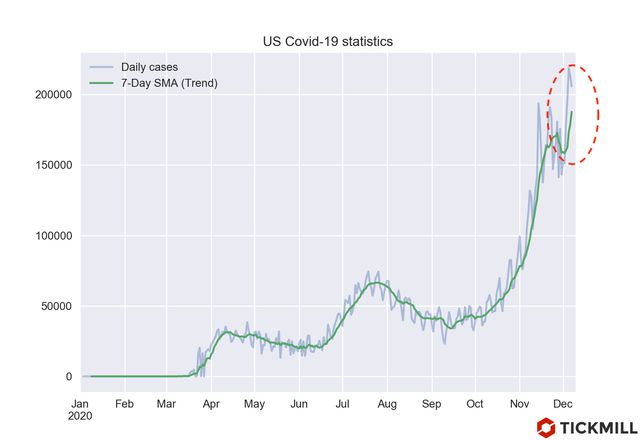

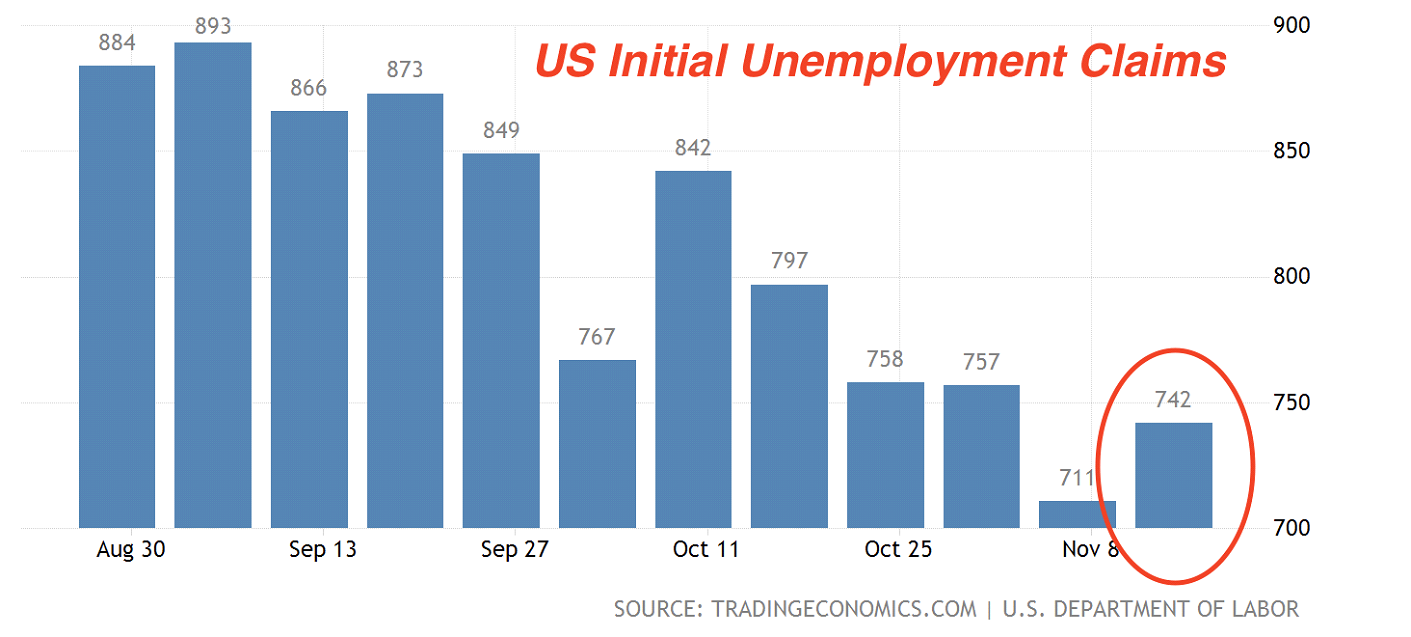

Initial jobless claims in the US fell short of forecasts for the first time in four weeks. Really bad signal. The increase in the unemployed amounted to 742K against the forecast of 707K, which likely reflects the impact of coronavirus restrictions, which are increasing in the US:

The negative print in the data point can be an early flare of slack in labor market recovery which warrants more attention to the data update in the next week. To continue the upward trend, equity markets would need a breakthrough in the fiscal deal negotiations which seemed like the only thing that can offer broad-based help to bullish sentiment.

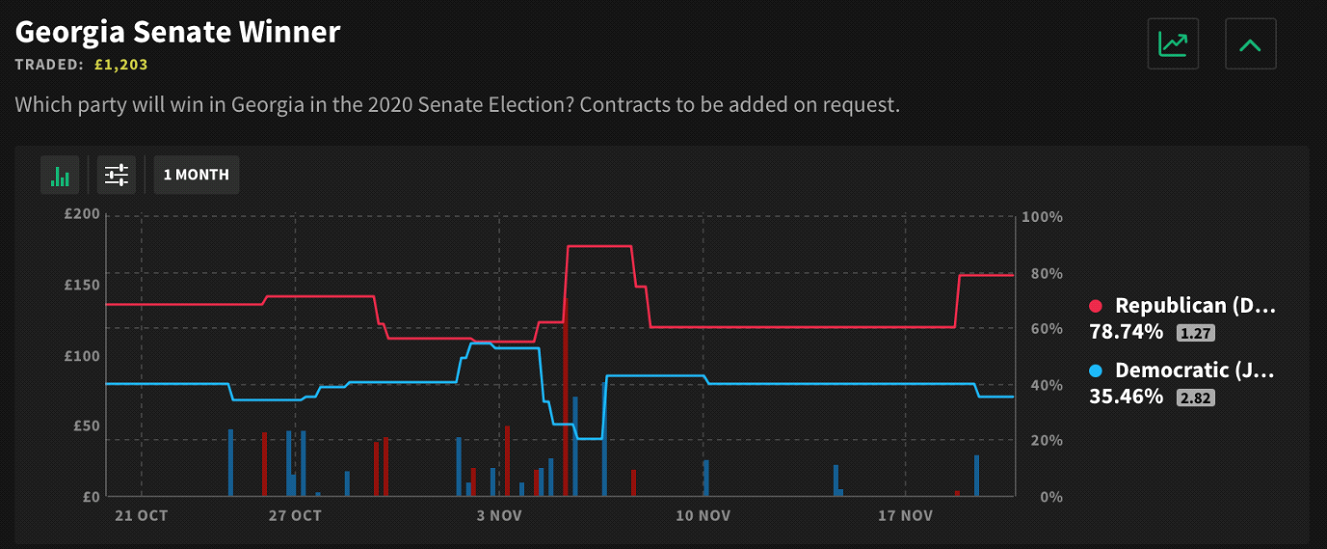

However, it makes sense to expect a breakthrough not earlier than in January 2021 as runoff elections to the Senate in Georgia will take place then and determine who will get majority in the Senate. Based on the following chart, the Republicans should have a negotiating advantage with Democrats:

Source:Smarkets.com

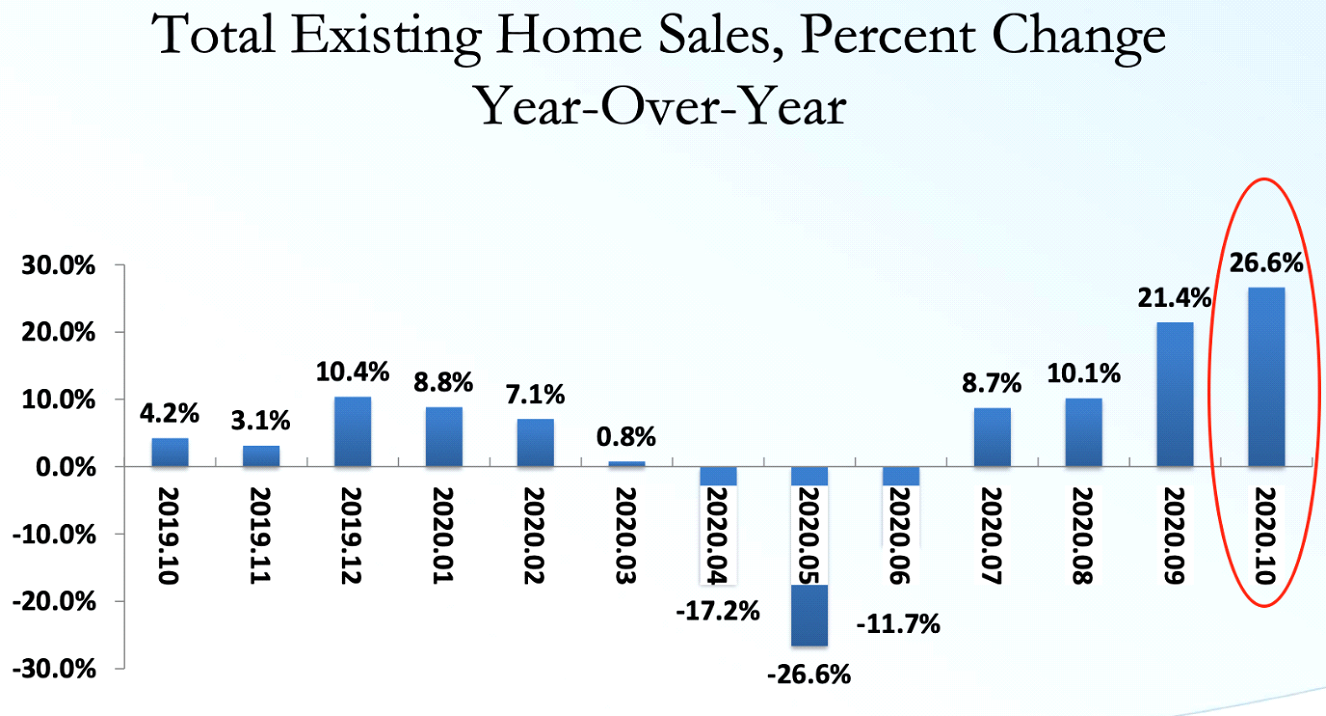

The growth of existing home sales in the United States left many forecasters bewildered. In October, sales increased by 4.3% versus September (-1.2% forecast), while the monthly growth in September was revised to 9.9%. Thus, in annual terms, sales increased by as much as 26.61%. Interestingly, the median price of home sold also increased - by 15.5%. Demand grew despite pandemic restrictions, falling incomes, high unemployment, to the extent that 2020 turned out to be the best year for the secondary market since 2009:

Source: NAHB

Obviously, the sales dynamics should offer some prolonged demand for goods and services of companies in home-improvement market.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.