tickmill-news

Tickmill Representative

- Messages

- 79

Oil’s retest of key resistance levels leaves USD vulnerable to attack

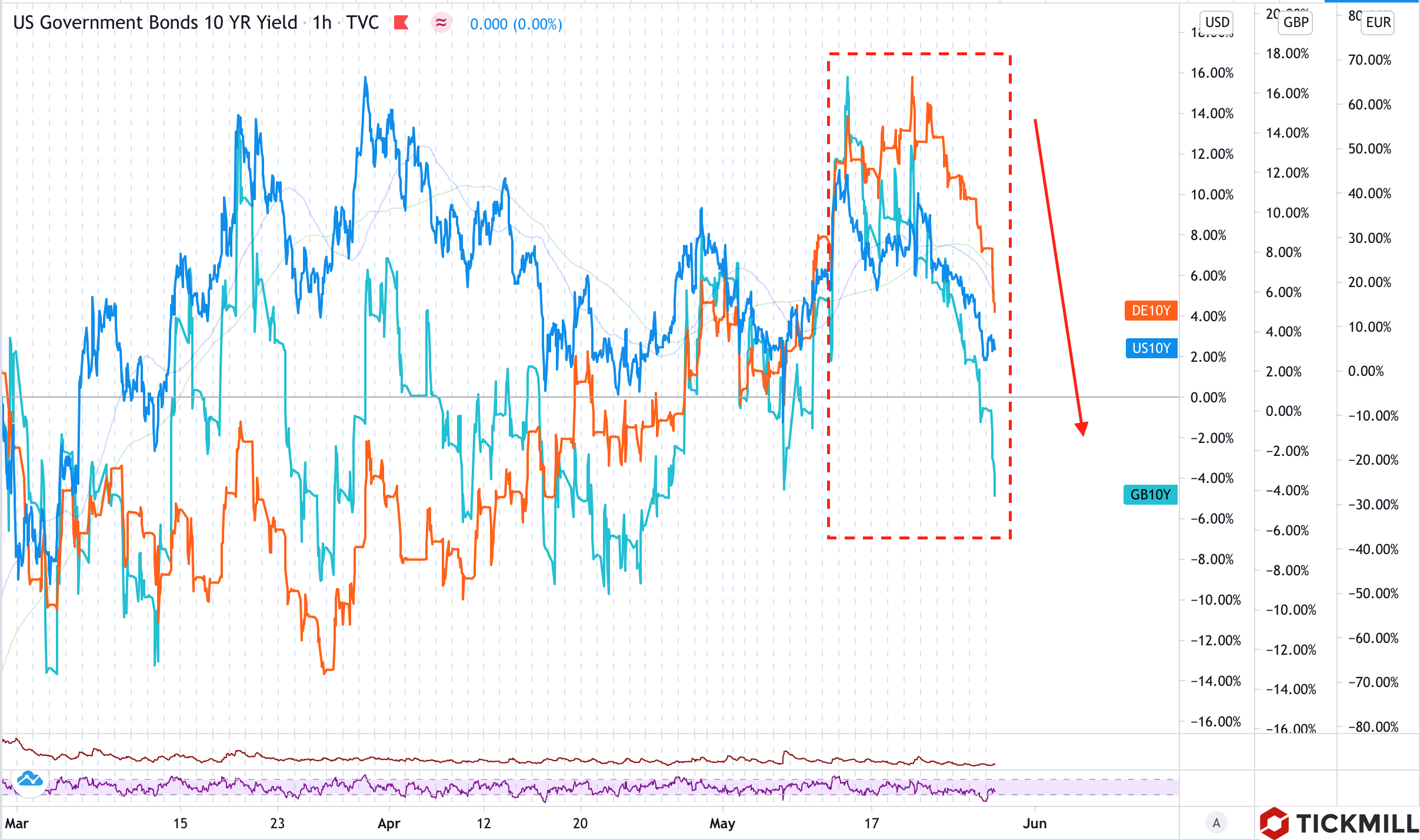

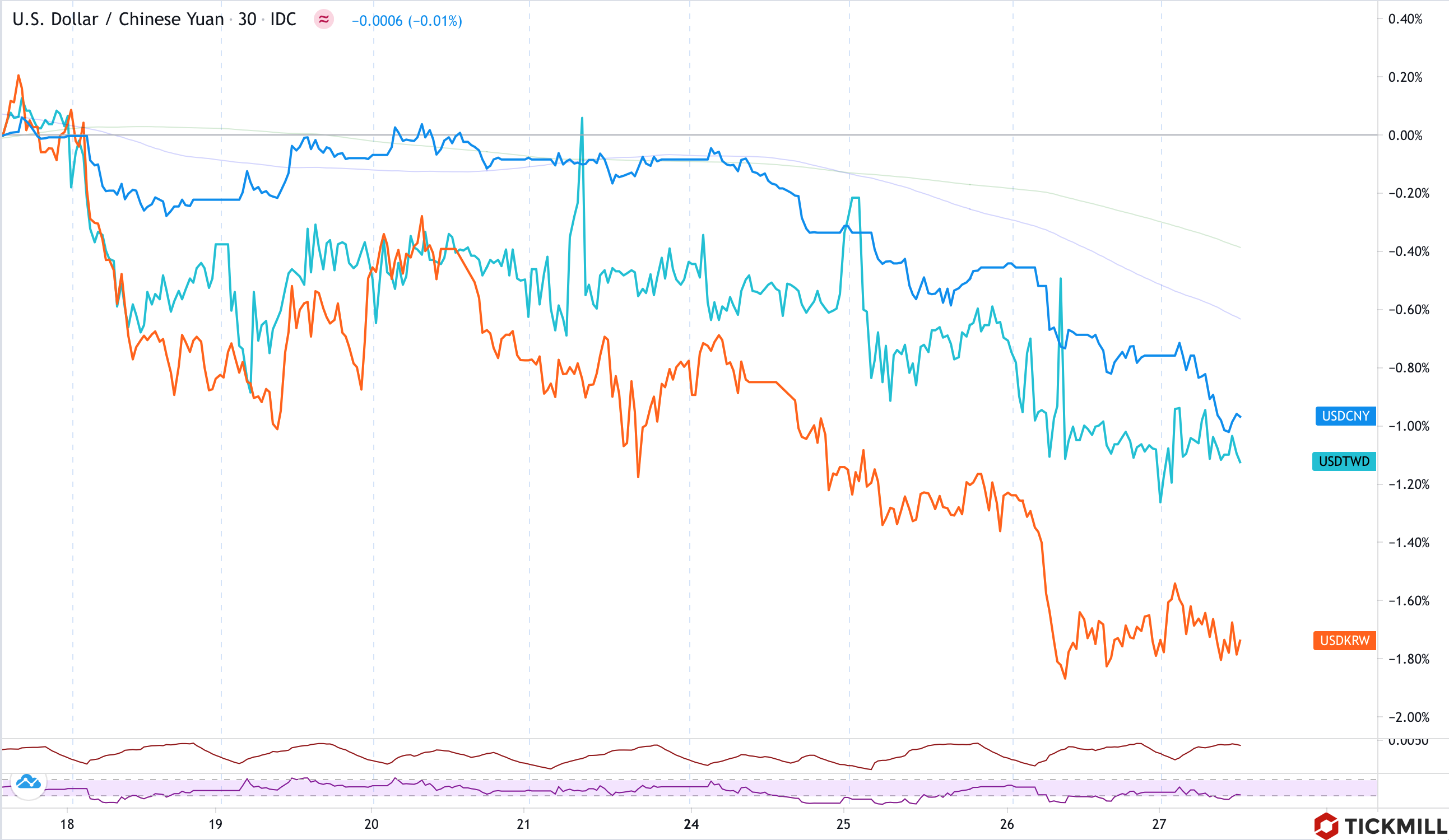

The rally in Asian equity markets, positive news flow regarding the virus as well as oil move towards key levels, sparking momentum in the rest of commodity complex, put USD under great pressure on Tuesday. The FOMC Minutes release today may secure the breakout below 90 points in the DXY as the Fed will most likely reiterate its uber-dovish stance that they remain committed to easing. In Europe, the progress in easing of social restrictions lifted bullish sentiment in the Euro.

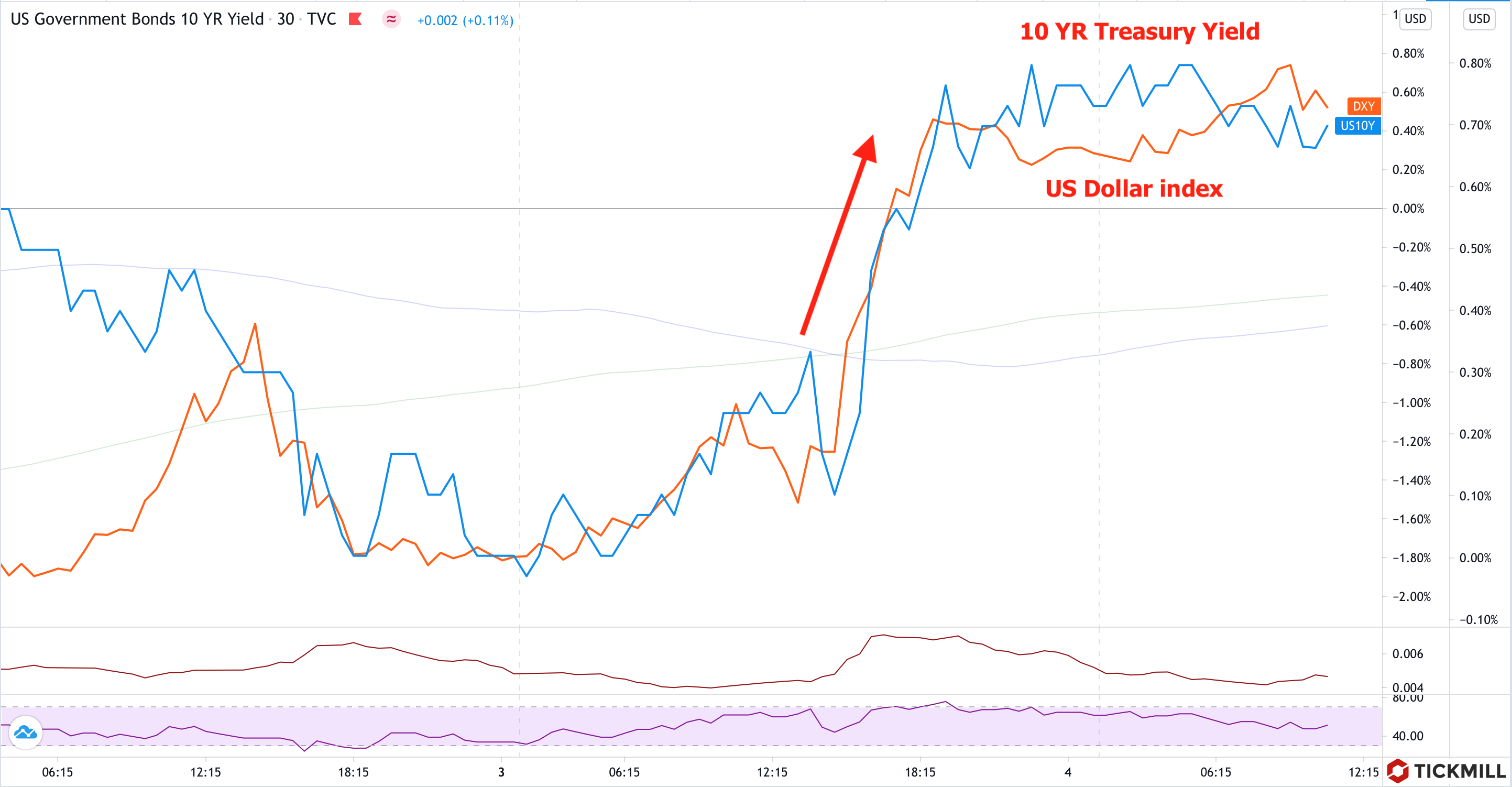

The next target in USD index is the area of 89.72-89.50, where a medium-term low was formed in the end of February:

In terms of momentum, the move was clearly excessive as seen from the RSI dropping to extreme levels (<20 points). This fact increases chances for a technical pullback from the support area towards 90 level before we could resumption of the medium-term downside.

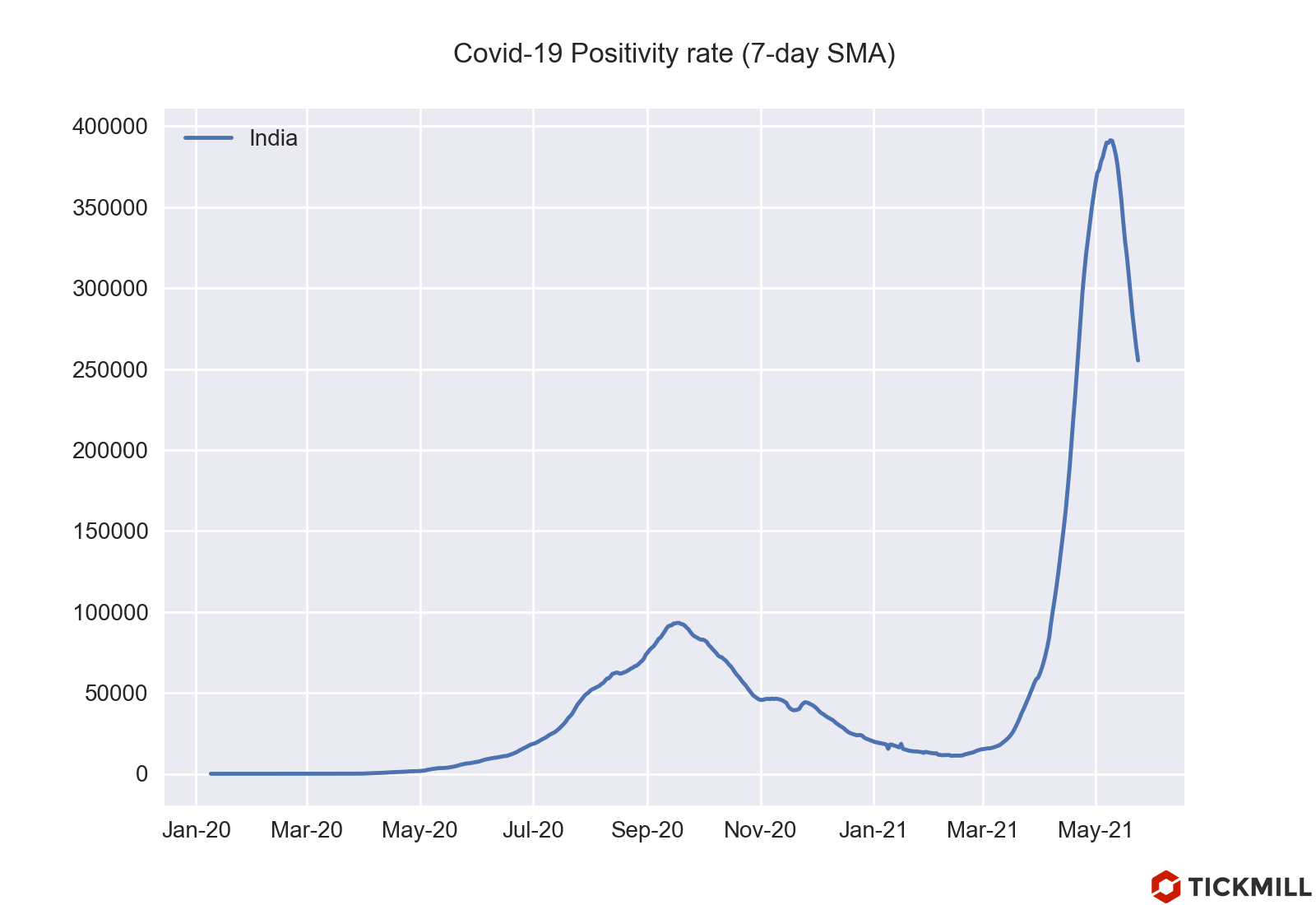

Brent crude oil benchmark pierced through $70/bbl resistance for the first time since mid-March amid signs of declining global inventories as reopening of economies fuels a boom in demand, including demand for basic commodities like oil. An important signal that sets the stage for bullish oil move is a welcomed decrease in daily cases growth in India which is one of the largest oil consumers in the world. The virus situation in Asia is improving despite a spate of negative headlines hitting the wires in the second half of the past week, as governments managed to avoid worst-case scenario - continued increase in positivity rates and harsher social distancing measures.

Last week, the IEA reported that the oil glut accumulated during the pandemic had been cleared thanks to fast recovery in demand. The news fueled rumors that the market can face deficit in supplies in which lifted prices of near-term contracts compared to longer ones. Futures spreads in the oil market widened signaling that backwardation state intensified.

On the technical front, oil keeps developing a bullish picture. This week we saw a retest of the previous resistance level at $70 while the uptrend remained intact. If quotes manage to close above $70 per barrel, the next target is the level of 71.22 which is the intersection of the upper bound of current uptrend and the prices peak in 2021:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

The rally in Asian equity markets, positive news flow regarding the virus as well as oil move towards key levels, sparking momentum in the rest of commodity complex, put USD under great pressure on Tuesday. The FOMC Minutes release today may secure the breakout below 90 points in the DXY as the Fed will most likely reiterate its uber-dovish stance that they remain committed to easing. In Europe, the progress in easing of social restrictions lifted bullish sentiment in the Euro.

The next target in USD index is the area of 89.72-89.50, where a medium-term low was formed in the end of February:

In terms of momentum, the move was clearly excessive as seen from the RSI dropping to extreme levels (<20 points). This fact increases chances for a technical pullback from the support area towards 90 level before we could resumption of the medium-term downside.

Brent crude oil benchmark pierced through $70/bbl resistance for the first time since mid-March amid signs of declining global inventories as reopening of economies fuels a boom in demand, including demand for basic commodities like oil. An important signal that sets the stage for bullish oil move is a welcomed decrease in daily cases growth in India which is one of the largest oil consumers in the world. The virus situation in Asia is improving despite a spate of negative headlines hitting the wires in the second half of the past week, as governments managed to avoid worst-case scenario - continued increase in positivity rates and harsher social distancing measures.

Last week, the IEA reported that the oil glut accumulated during the pandemic had been cleared thanks to fast recovery in demand. The news fueled rumors that the market can face deficit in supplies in which lifted prices of near-term contracts compared to longer ones. Futures spreads in the oil market widened signaling that backwardation state intensified.

On the technical front, oil keeps developing a bullish picture. This week we saw a retest of the previous resistance level at $70 while the uptrend remained intact. If quotes manage to close above $70 per barrel, the next target is the level of 71.22 which is the intersection of the upper bound of current uptrend and the prices peak in 2021:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.