Sive Morten

Special Consultant to the FPA

- Messages

- 18,776

Fundamentals

In second report guys, we still take a look at GBP. Last time (it was two weeks ago) we've said that despite our long-term bearish view - in nearest few weeks we expect upside pullback:

"This combination of factors makes us suggest two things. First is, our long-term bearish scenario stands intact and GBP should continue dropping. BoE should match its policy to reality which also will be dovish factor for GBP, supporting bearish trend. Second - in coming 3-6 weeks solid upside retracement is possible, as investors will try to protect themselves from political uncertainty and oversold situation on GBP".

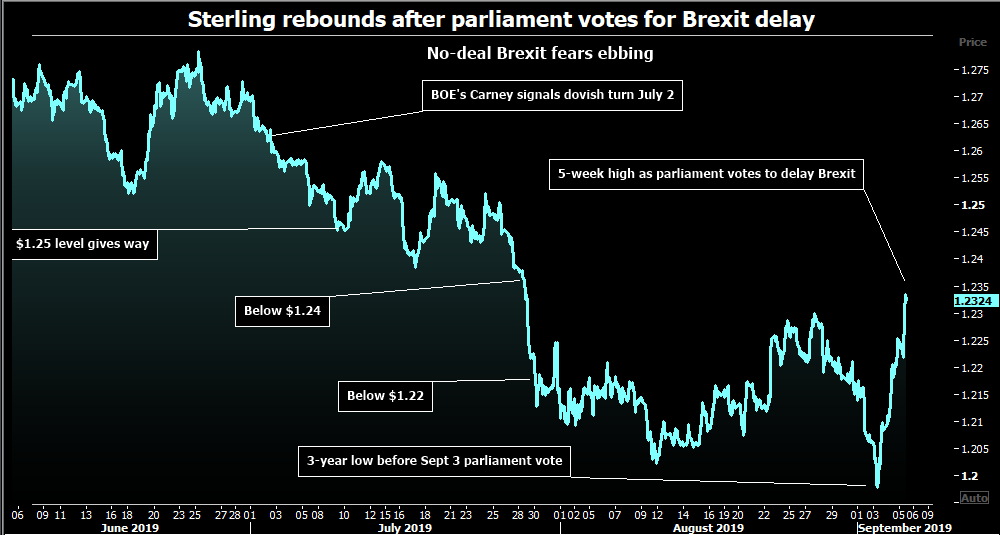

Since a lot of events have happened on Brexit topic and our suggestion starts to work, we need to update our analysis. As we've expected with starting of new session of UK Parliament after vacation, Prime Minister meets new problems on a way to complete Brexit at any way, but right to the term of 31st of October. No deal Brexit meets strong barrier among politicians. Boris Johnson has lost majority in Parliament and chances on hard Brexit has dropped, which triggered strong rally on GBP and our scenario has become a reality.

As Reuters reports - the pound surged to a five-week high on Thursday after lawmakers voted to prevent Prime Minister Boris Johnson taking Britain out of the European Union on Oct. 31 without a transition agreement and his brother Jo quit the government, citing national interest.

Political uncertainty remained high as the prime minister renewed his effort to seek an election on Oct. 15 after a first attempt was defeated on Wednesday. But sterling responded to a sense that a no-deal Brexit had been averted for now.

“Removing the immediate threat of a no-deal Brexit has helped the pound recover some of its recent weakness,” said Daniel Trum and Dean Turner, strategists at UBS Wealth Management.

The pound has been shunned in recent weeks as concerns grew that Britain would crash out of the EU without a deal on the scheduled date of Oct. 31. On Monday, it fell to below $1.20, a near-three-year low.

UBS analysts said that if Brexit were delayed until January, and an election were set for a date after Oct. 31, the pound could rise as high as $1.30, a four-month high.

“A delay for both Brexit and general election will continue to send the pound higher,” said Neil Jones, head of hedge fund currency sales at Mizuho Bank.

The rally reverberated through the derivative markets as well. Two-month implied volatility gauges for pound options, which cover the scheduled Oct. 31 Brexit date, fell.

The drop in expected price swings for the pound indicated markets were unwinding extreme short-term negative bets. Two-month implied volatility fell below 13 vol after rising to a three-year high of nearly 16 vol earlier this week.

Despite the rebound, the British currency remained more than 8% below its March highs of nearly $1.34, with many citing the uncertainty that an election would bring, whenever it is held.

“With the results from any election so hard to forecast and the difficulty of still fixing on a deal, we think further pound rallies are likely to be limited until we have clarity on outcomes,” said John Marley, a senior FX consultant at FX risk management specialist, SmartCurrencyBusiness.

Opposition parties will discuss on Friday how to respond to Boris Johnson’s bid to call a snap election after the prime minister said he would rather die in a ditch than delay the planned Oct. 31 departure from the European Union.

Lawmakers will on Monday hold another vote on a motion on whether to hold an early election. Opposition parties want to ensure that an election does not allow Johnson to lead the United Kingdom out of the EU without a deal next month.

“The main threat to sterling’s recovery is if Johnson’s Conservative party were to win with a majority in an early election. They could then overturn the legislation requiring them to ask for an extension, increasing the threat of leaving without a deal,” said Mark Haefele, Chief Investment Officer, UBS Global Wealth Management.

Haefele predicted that the pound would weaken to $1.15 or lower in the event of a no-deal Brexit.

While huge uncertainty about the political outlook in Britain remains, investors have taken solace from lawmakers’ determination to block a no-deal Brexit that economists say would be severly damaging for the UK economy.

Expectations for sterling price swings in the months ahead have fallen sharply as the risk of a no-deal exit from the EU receded, with implied volatility gauges back to levels of mid-August after spiking to their highest in 2019 earlier this week .

CFTC data shows that net short position moves out from extreme bearish position. In last 2-3 weeks it becomes smaller a bit and short-covering leads to upside action on GBP. This is totally match to our expectations.

Source: cftc.gov

Charting by Investing.com

There is no more expectations on any rate hike from MPC. Expectations stand stable around 0.75% and some chances stand for rate cut in November meeting:

Source: cmegroup.com

Since really big events stand around UK and GBP - Fathom consulting releases new research on UK economy. They take a view, what will happen if Labour party will head the government. Here is, as usual, we put some extractions from it:

With the turmoil in British politics reaching new heights this week, what happens next is anyone’s guess. One of the many possibilities — however unlikely — is an outright majority for a Corbyn-led Labour government. While the impact on the real economy may take months or even years to be seen, Fathom Consulting believes that financial markets will react immediately.

Having made every effort to distance itself from Tony Blair’s New Labour, today’s manifestation of the Labour Party looks increasingly like the old one. One that oversaw two domestically driven financial crises in the second half of the 20th century. The Wilson–Callaghan government of 1974–79 saw the public sector deficit, inflation, gilt yields and corporate spreads all reach peace-time highs, while growth stagnated and the value of sterling (post Bretton-Woods) reached a record low.

Mr Corbyn’s Labour Party has not engaged in creating a market-friendly narrative about what a Labour government would look like, and has instead dabbled in market-hostile narratives. Investors are worried, perhaps rightly, that Labour will follow through with some of the various policy ideas that have been floated, such as:

Sterling-denominated risk spreads rose sharply, with the investment-grade corporate spread in particular reaching an all-time high (since surpassed) of more than double its post-war average.

In Fathom’s central Corbyn scenario, these market impacts are replicated. Sterling depreciates by 15%, inflation increases by 2 percentage points, the level of GDP falls by 4% by 2023 and gilt yields spike by 250 basis points, all relative to the baseline forecast. These outcomes trigger an outright recession in 2021 and bring about the return of stagflation.

Such a government is unlikely to survive very long. So, the likeliest outcome in this world is a short-lived government with a weak mandate, destroyed by a market response that it has actively encouraged while in opposition.

However, Mr Corbyn and his advisers are aware of this. They have plans to prevent that set of outcomes — capital controls, control of monetary policy, and the rest. Part of their problem, though, is that the damage might be done before they take office, as markets judge the likelihood of that eventuality to be increasing. By the time Mr Corbyn walks into Number 10, if he ever does, it might already be too late.

As a bottom line:

So, guys, what conclusion we could make on new information. First is UK economy background and statistics is not impacted by parliamentary debates. We talked about it last time and expectations are moderately bearish.

The one thing stands clear - as markets come around after optimistic rush of "no-deal Brexit", the first euphoria starts to fade and everybody understand importance of possible early elections. This is the last bet that will resolve everything. But for us the answer will be simple - GBP will drop anyway. If Boris Johnson will take the majority - it will be too few time till 31st of October and hard Brexit will appear on horizon. Victory of Labour Party is a hazard of negative events in economy as Fathom tells above. The only positive result could be is postponing of Brexit for some time, at least till January. But postponing has to be agreed with EU, and it is not clear yet how EU will react. The odds balance stand not in favor of GBP. Actually, this will not be positive result per se, but it will keep intrigue a bit longer.

In shorter-term, at least till 15th of October, GBP could keep gradual upside action or turn to wide flat, showing furious reaction on any news that will be released. This is volatility time. It means that correct strategy is take short-term trades on clear patterns, and avoid to take longer-term positions on major trend continuation by far.

Technicals

Monthly

August and September months do not make strong impact on monthly picture. Monthly chart still shows no signs that could make us doubt on bearish long-term setup by far. Market has free space between 1.20 lows and our 1.1335 butterfly target. Breaking YPS1 confirms existence of long-term bear trend as well.

In longer-term perspective market stands with our all time AB-CD pattern. COP target and following retracement are done. Now CD leg continues and in long-term perspective, we have OP target at 0.95 level.

Retracement that we've anticipated around "1.20 lows" is started. While it holds, we mostly deal with shorter time frames - daily and intraday.

Weekly

Market barely has not reached 1.18 butterfly target, showing W&R of 1.20 lows that we've discussed as well. Weekly chart has the signs of short-term reversal and retracement - completed bullish butterfly and W&R around COP target as well. Last week also has a features of Reversal one, but it just near missed the close price as it should be above previous week's top.

Butterfly suggests at least 30% pullback which means that major level on coming week is 1.25, which is also recent lows. We also do not exclude reaching of 1.2830 K-resistance area, but GBP will need some additional external push from political factors to reach it.

Daily

All technical bullish signs are present here - MACD divergence, W&R of recent lows, fast acceleration. First 3/8 level was broken and market is stopped by Overbought only. MPR1 also stands there.

Here we could recognize the shape of Double Bottom pattern. It means that reaching of 1.25 area is just a question of time, second - it keeps door open to reach 1.28 level as well.

Intraday

So, as market at overbought, we start next week from retracement. Market has formed bullish reversal swing here. And we could get two different trades. First one is our major setup for taking long position, by-product trade, the secondary one is possible B&B "Buy" that could be formed at major 3/8 support of 1.22 level, accompanied by WPP.

In general, because of overbought and first reversal swing, retracement could be deeper, but it would be better to not ignore B&B as well. It creates great low risk setup and who knows, what if upside action will start from just 3/8 level. As usual, we could catch both trades, but it is possible to split total position in two parts and apply scale-in if market later will drop to 1.21 level.

Conclusion:

Analysis of fundamental factors this week confirms existing of bearish sentiment and we keep our long-term bearish view on GBP. In longer term perspective we expect that GBP will trade lower due Brexit culmination and more adopted BoE policy which now stands out of reality a bit. Technically, we have two targets - 1.13 and 0.95.

In shorter-term perspective, as we've expected fake 1.20 breakout and upside bounce due overextended speculative position on GBP which stands at all time lows and possible which is done already now all eyes stand on October "early voting" in UK Parliament. Until this moment, GBP could drift higher or turn to wide flat. But, overall situation, despite the results of voting provides narrow room to positive outcome to GBP.

The technical portion of Sive's analysis owes a great deal to Joe DiNapoli's methods, and uses a number of Joe's proprietary indicators. Please note that Sive's analysis is his own view of the market and is not endorsed by Joe DiNapoli or any related companies.

In second report guys, we still take a look at GBP. Last time (it was two weeks ago) we've said that despite our long-term bearish view - in nearest few weeks we expect upside pullback:

"This combination of factors makes us suggest two things. First is, our long-term bearish scenario stands intact and GBP should continue dropping. BoE should match its policy to reality which also will be dovish factor for GBP, supporting bearish trend. Second - in coming 3-6 weeks solid upside retracement is possible, as investors will try to protect themselves from political uncertainty and oversold situation on GBP".

Since a lot of events have happened on Brexit topic and our suggestion starts to work, we need to update our analysis. As we've expected with starting of new session of UK Parliament after vacation, Prime Minister meets new problems on a way to complete Brexit at any way, but right to the term of 31st of October. No deal Brexit meets strong barrier among politicians. Boris Johnson has lost majority in Parliament and chances on hard Brexit has dropped, which triggered strong rally on GBP and our scenario has become a reality.

As Reuters reports - the pound surged to a five-week high on Thursday after lawmakers voted to prevent Prime Minister Boris Johnson taking Britain out of the European Union on Oct. 31 without a transition agreement and his brother Jo quit the government, citing national interest.

Political uncertainty remained high as the prime minister renewed his effort to seek an election on Oct. 15 after a first attempt was defeated on Wednesday. But sterling responded to a sense that a no-deal Brexit had been averted for now.

“Removing the immediate threat of a no-deal Brexit has helped the pound recover some of its recent weakness,” said Daniel Trum and Dean Turner, strategists at UBS Wealth Management.

The pound has been shunned in recent weeks as concerns grew that Britain would crash out of the EU without a deal on the scheduled date of Oct. 31. On Monday, it fell to below $1.20, a near-three-year low.

UBS analysts said that if Brexit were delayed until January, and an election were set for a date after Oct. 31, the pound could rise as high as $1.30, a four-month high.

“A delay for both Brexit and general election will continue to send the pound higher,” said Neil Jones, head of hedge fund currency sales at Mizuho Bank.

The rally reverberated through the derivative markets as well. Two-month implied volatility gauges for pound options, which cover the scheduled Oct. 31 Brexit date, fell.

The drop in expected price swings for the pound indicated markets were unwinding extreme short-term negative bets. Two-month implied volatility fell below 13 vol after rising to a three-year high of nearly 16 vol earlier this week.

Despite the rebound, the British currency remained more than 8% below its March highs of nearly $1.34, with many citing the uncertainty that an election would bring, whenever it is held.

“With the results from any election so hard to forecast and the difficulty of still fixing on a deal, we think further pound rallies are likely to be limited until we have clarity on outcomes,” said John Marley, a senior FX consultant at FX risk management specialist, SmartCurrencyBusiness.

Opposition parties will discuss on Friday how to respond to Boris Johnson’s bid to call a snap election after the prime minister said he would rather die in a ditch than delay the planned Oct. 31 departure from the European Union.

Lawmakers will on Monday hold another vote on a motion on whether to hold an early election. Opposition parties want to ensure that an election does not allow Johnson to lead the United Kingdom out of the EU without a deal next month.

“The main threat to sterling’s recovery is if Johnson’s Conservative party were to win with a majority in an early election. They could then overturn the legislation requiring them to ask for an extension, increasing the threat of leaving without a deal,” said Mark Haefele, Chief Investment Officer, UBS Global Wealth Management.

Haefele predicted that the pound would weaken to $1.15 or lower in the event of a no-deal Brexit.

While huge uncertainty about the political outlook in Britain remains, investors have taken solace from lawmakers’ determination to block a no-deal Brexit that economists say would be severly damaging for the UK economy.

Expectations for sterling price swings in the months ahead have fallen sharply as the risk of a no-deal exit from the EU receded, with implied volatility gauges back to levels of mid-August after spiking to their highest in 2019 earlier this week .

CFTC data shows that net short position moves out from extreme bearish position. In last 2-3 weeks it becomes smaller a bit and short-covering leads to upside action on GBP. This is totally match to our expectations.

Source: cftc.gov

Charting by Investing.com

There is no more expectations on any rate hike from MPC. Expectations stand stable around 0.75% and some chances stand for rate cut in November meeting:

Source: cmegroup.com

Since really big events stand around UK and GBP - Fathom consulting releases new research on UK economy. They take a view, what will happen if Labour party will head the government. Here is, as usual, we put some extractions from it:

With the turmoil in British politics reaching new heights this week, what happens next is anyone’s guess. One of the many possibilities — however unlikely — is an outright majority for a Corbyn-led Labour government. While the impact on the real economy may take months or even years to be seen, Fathom Consulting believes that financial markets will react immediately.

Having made every effort to distance itself from Tony Blair’s New Labour, today’s manifestation of the Labour Party looks increasingly like the old one. One that oversaw two domestically driven financial crises in the second half of the 20th century. The Wilson–Callaghan government of 1974–79 saw the public sector deficit, inflation, gilt yields and corporate spreads all reach peace-time highs, while growth stagnated and the value of sterling (post Bretton-Woods) reached a record low.

Mr Corbyn’s Labour Party has not engaged in creating a market-friendly narrative about what a Labour government would look like, and has instead dabbled in market-hostile narratives. Investors are worried, perhaps rightly, that Labour will follow through with some of the various policy ideas that have been floated, such as:

- Modern Monetary Theory

- Revoking the operational independence of the Bank of England

- Taking direct control of the private banks that are partially or wholly owned by the public sector

- Imposing capital controls to prevent a run on the pound

- Redistributing a proportion of shares in large private companies to ‘the workers’ and insisting on worker representation on the boards of those companies

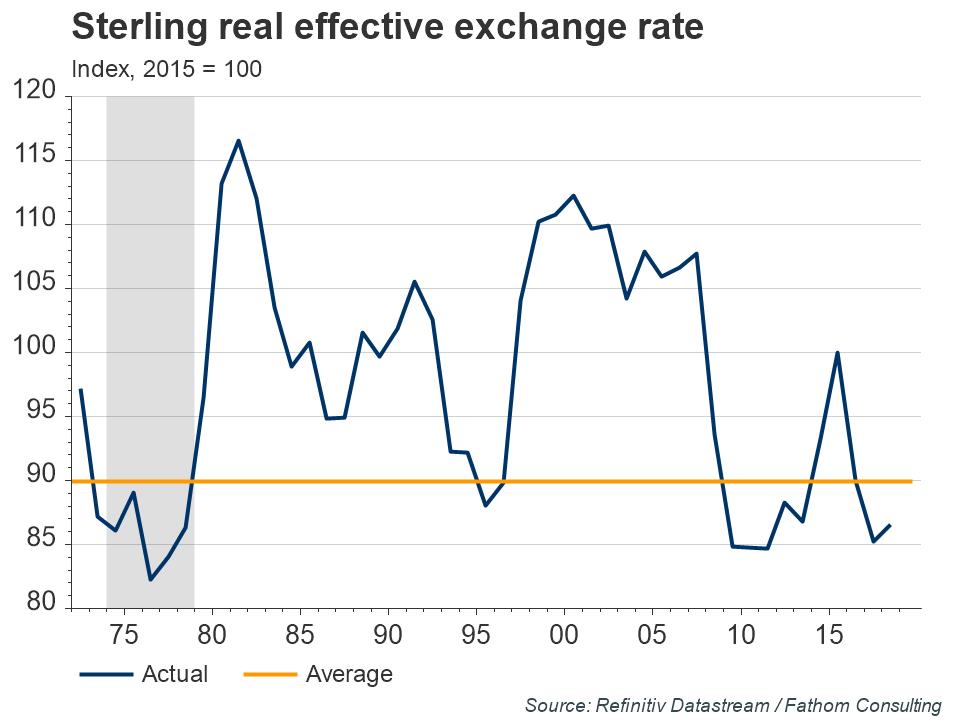

- Sterling fell by 15% in real effective terms ahead of and during the Wilson–Callaghan government. (see chart above)

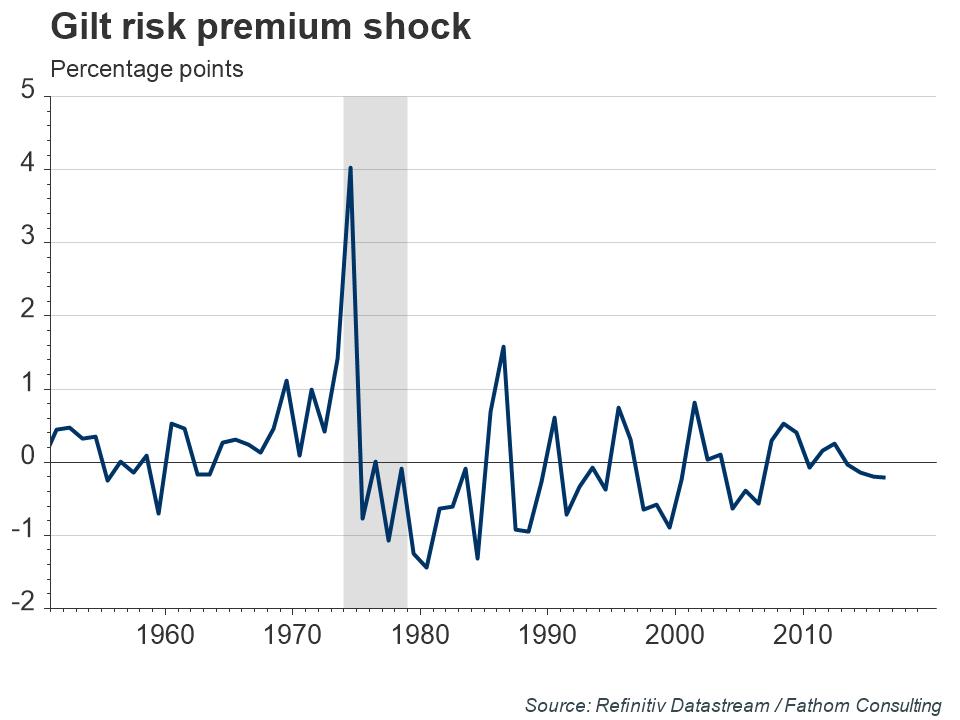

- Gilt yields rocketed by 400 basis points on the election of the Wilson–Callaghan government, controlling for all the other impacts on the gilt yield, arising from inflation, growth and short rates. The chart below measures this ‘risk premium shock’

Sterling-denominated risk spreads rose sharply, with the investment-grade corporate spread in particular reaching an all-time high (since surpassed) of more than double its post-war average.

In Fathom’s central Corbyn scenario, these market impacts are replicated. Sterling depreciates by 15%, inflation increases by 2 percentage points, the level of GDP falls by 4% by 2023 and gilt yields spike by 250 basis points, all relative to the baseline forecast. These outcomes trigger an outright recession in 2021 and bring about the return of stagflation.

Such a government is unlikely to survive very long. So, the likeliest outcome in this world is a short-lived government with a weak mandate, destroyed by a market response that it has actively encouraged while in opposition.

However, Mr Corbyn and his advisers are aware of this. They have plans to prevent that set of outcomes — capital controls, control of monetary policy, and the rest. Part of their problem, though, is that the damage might be done before they take office, as markets judge the likelihood of that eventuality to be increasing. By the time Mr Corbyn walks into Number 10, if he ever does, it might already be too late.

As a bottom line:

So, guys, what conclusion we could make on new information. First is UK economy background and statistics is not impacted by parliamentary debates. We talked about it last time and expectations are moderately bearish.

The one thing stands clear - as markets come around after optimistic rush of "no-deal Brexit", the first euphoria starts to fade and everybody understand importance of possible early elections. This is the last bet that will resolve everything. But for us the answer will be simple - GBP will drop anyway. If Boris Johnson will take the majority - it will be too few time till 31st of October and hard Brexit will appear on horizon. Victory of Labour Party is a hazard of negative events in economy as Fathom tells above. The only positive result could be is postponing of Brexit for some time, at least till January. But postponing has to be agreed with EU, and it is not clear yet how EU will react. The odds balance stand not in favor of GBP. Actually, this will not be positive result per se, but it will keep intrigue a bit longer.

In shorter-term, at least till 15th of October, GBP could keep gradual upside action or turn to wide flat, showing furious reaction on any news that will be released. This is volatility time. It means that correct strategy is take short-term trades on clear patterns, and avoid to take longer-term positions on major trend continuation by far.

Technicals

Monthly

August and September months do not make strong impact on monthly picture. Monthly chart still shows no signs that could make us doubt on bearish long-term setup by far. Market has free space between 1.20 lows and our 1.1335 butterfly target. Breaking YPS1 confirms existence of long-term bear trend as well.

In longer-term perspective market stands with our all time AB-CD pattern. COP target and following retracement are done. Now CD leg continues and in long-term perspective, we have OP target at 0.95 level.

Retracement that we've anticipated around "1.20 lows" is started. While it holds, we mostly deal with shorter time frames - daily and intraday.

Weekly

Market barely has not reached 1.18 butterfly target, showing W&R of 1.20 lows that we've discussed as well. Weekly chart has the signs of short-term reversal and retracement - completed bullish butterfly and W&R around COP target as well. Last week also has a features of Reversal one, but it just near missed the close price as it should be above previous week's top.

Butterfly suggests at least 30% pullback which means that major level on coming week is 1.25, which is also recent lows. We also do not exclude reaching of 1.2830 K-resistance area, but GBP will need some additional external push from political factors to reach it.

Daily

All technical bullish signs are present here - MACD divergence, W&R of recent lows, fast acceleration. First 3/8 level was broken and market is stopped by Overbought only. MPR1 also stands there.

Here we could recognize the shape of Double Bottom pattern. It means that reaching of 1.25 area is just a question of time, second - it keeps door open to reach 1.28 level as well.

Intraday

So, as market at overbought, we start next week from retracement. Market has formed bullish reversal swing here. And we could get two different trades. First one is our major setup for taking long position, by-product trade, the secondary one is possible B&B "Buy" that could be formed at major 3/8 support of 1.22 level, accompanied by WPP.

In general, because of overbought and first reversal swing, retracement could be deeper, but it would be better to not ignore B&B as well. It creates great low risk setup and who knows, what if upside action will start from just 3/8 level. As usual, we could catch both trades, but it is possible to split total position in two parts and apply scale-in if market later will drop to 1.21 level.

Conclusion:

Analysis of fundamental factors this week confirms existing of bearish sentiment and we keep our long-term bearish view on GBP. In longer term perspective we expect that GBP will trade lower due Brexit culmination and more adopted BoE policy which now stands out of reality a bit. Technically, we have two targets - 1.13 and 0.95.

In shorter-term perspective, as we've expected fake 1.20 breakout and upside bounce due overextended speculative position on GBP which stands at all time lows and possible which is done already now all eyes stand on October "early voting" in UK Parliament. Until this moment, GBP could drift higher or turn to wide flat. But, overall situation, despite the results of voting provides narrow room to positive outcome to GBP.

The technical portion of Sive's analysis owes a great deal to Joe DiNapoli's methods, and uses a number of Joe's proprietary indicators. Please note that Sive's analysis is his own view of the market and is not endorsed by Joe DiNapoli or any related companies.

")