Sive Morten

Special Consultant to the FPA

- Messages

- 18,675

Fundamentals

In recent few months we've dedicated a lot of time to show you the wide picture of economy problems as in EU as in the US and described the relation of all economy sectors, and why ECB and Fed now are in the dead-way. Today it makes sense to update ECB and Fed policies, as we've passed through recent ECB decision and new inflation data and now come to the Fed meeting, PCE numbers and IIQ GDP preliminary data. Depending on what we will see from ECB and Fed policy we could make suggestion on future economy performance.

Before we turn directly to analysis of ECB rate decision, we need to take a look at performance of PMI indicators and recent poll of business in their attitude to current economy conditions. Crisis is just starting, its effect is barely could be signed by far, but it should become more evident within nearest 6 months. For example, here we already could recognize first signs of stagflation - slowing of economy growth, accompanied with inflation:

Here is what most recent Manufacturing Business Survey from Philadelphia Fed Reserve Bank shows.

This recent survey shows the first signs that production activity is decreasing while inflationary pressure, maybe is loosing impulse, but remains at high levels. This is not pleasant combination, guys.

The one of the ways, how inflation deteriorates households' wealth, you could see on example of gasoline demand. Now is summertime, high traveling season but take a look at gasoline consumption - it is decreasing far below 2015-2019 average level. This is because people have no money to pay for it.

This is how inflation works: nominally, people receive a record amount of dollars in the form of salaries, benefits, pensions, but they cannot afford the same amount of goods as yesterday. That is, real life has become worse. It is also interesting that the drop in gasoline demand in the United States does not cause a strong decline in oil prices. The reason for this is its shortage. The only source to set the balance between demand and supply is to take the oil from the US strategic reserves. However, they exhaust soon. If demand does not collapse more by that time, oil prices could go much higher.

Second component is unemployment. We have mentioned it few times, that we expect rising of unemployment in the US (in EU, UK as well) in near term, and expect it to be around 10%. Problems now start to catching up with the companies and Initial claims stubbornly rising, for the 8 weeks in a row, reaching the levels of Nov 2021. Not the numbers per se are interesting but the tendency, how they are increasing.

Situation in Europe hardly looks better. Recent EU CPI shows 9.6% level and this is not the ceil yet. The structure of price rising envelops all spheres. It is not necessary to talk about electricity and energy. Food is rising for 12%, Transportation - 16%, home rent and utilities - 18%, other non-food and energy goods rising for 5%.

But, it is not the CPI inflation that makes us worry. CPI numbers have not become a surprise. Take a look at these two indicators and how strong correlated they are. Business activity is lagging, and supposedly should keep dropping. It is understandable now. Energy crisis provokes economy crisis, which in turn has triggered political crisis as well.

There are all signs of economic degradation. The consumer confidence index against the backdrop of record price growth in the Eurozone has collapsed to its historic low – it has never been as bad as in July 2022. Neither in 2008-2009, nor in the debt crisis of 2010-2012, nor even in the COVID crisis of 2020.

Not only the minimum levels of consumer confidence for all time are reached here, but the rate of degradation is also remarkable. The breaking point is February 2022, when consumer confidence turned into an uncontrolled collapse.

The resignation of the British Prime Minister, the departure of Italian Prime Minister Mario Draghi, resignations in Estonia, Belgium and Bulgaria, a significant undermining of confidence to Scholz, and finally the drop in the confidence rating of the French president. There is a fragmentation of the European coalition and fragmentation of the political space, center-left forces are growing, there is a risk of expansion of radical political parties against the background of economic collapse.

There are all signs of economic degradation. The consumer confidence index against the backdrop of record price growth in the Eurozone has collapsed to its historic low – it has never been as bad as in July 2022. Neither in 2008-2009, nor in the debt crisis of 2010-2012, nor even in the COVID crisis of 2020.

The graph shows a comparison with the index of economic activity, which has a correlation close to unity with the consumer confidence index. The dynamics are almost completely synchronized, but the collapse of economic activity is not as rapid yet. It means that the worst is yet to come. The system is still based on some inertia, but the processes are running.

With this preview, lets take a look at solution that ECB (and later the Fed as well) has offered to the investors and economists.

ECB MEETING RESULTS

0.5% rate change was not totally unexpected, that we could understand from market reaction. It was very short-term and reversed relatively fast. Most interesting what else C. Lagarde said. The major event of last ECB meeting is an announcement of unlimited QE ("Purchases are not restricted ex ante"). Yes, and don't be surprised with it. Barely ECB has finished PEPP programme as they immediately has started TPI - The Transmission Protection Instrument. It was a lot of sophistics has been used in explanation, but in two words speaking - ECB will monitor the interest rates market of EU countries and use TPI to "fix disproportions" and "to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across the euro area" . Since this "disorderly market dynamics" appears on the interest rates of highly indebted countries, like Italy, Portugal, Spain, Greece, etc., ECB will buy their bonds to hold undesirable rate rising. Instead they will sell Germany bonds that have relatively low yield. Also it is noted that TPI might be applied not only to government but to corporate sector as well (Uniper, RWE ??).

Thus, ECB intends to plug holes in EU countries despite of budget policy, Debt/GDP ratio etc. The priority direction is the reinvestment of securities from "strong participants" to the purchase of securities of "weak participants". However, the news is that the ECB allows an increase in the balance sheet if the pace of reinvestment is not enough to stabilize the market. That's the wonderful way they are trying to beat inflation... And the major conclusion is - ECB capitulates and keep printing money while inflation will keep going higher. Such perspectives suggest further weakness of EUR/USD.

Well, although ECB starts QE, but it did it publicly, while FED is trying to play spies game. We're coming to turning point on next week. First is, market anticipates 1.0% rate change. Many traders suppose that it is already mostly priced-in. We agree but only for tactical, speculating purposes in a moment of decision release US dollar could drop as traders will start "selling on the fact". But not in long-term, as it is difficult to accept high 2.5-2.75% interest rate now. And after short-term profit taking, the major tendency continues.

Next hit will come from earning reports on 27th of July. Microsoft and Alphabet Inc. (Google) are expected to report earnings on 07/26/2022 after market close. According to Zacks Investment Research, based on 12 analysts' forecasts, the consensus EPS forecast for the quarter is $1.28. Microsoft EPS according to Zacks Investment Research is $2.28. The reported EPS for the same quarter last year was $2.17. It is rumor that reports will be worse than expected.

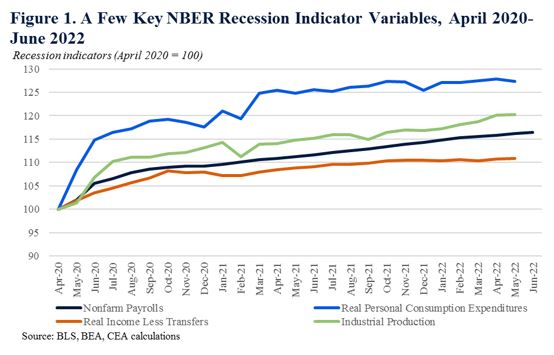

Finally, on 28th of July, the US economy officially steps in recession as IIQ GDP numbers will be negative:

Next day we also get PCE index, personal income and consumption that are also vital to the whole picture.

So, be prepared to verbal intervention across all media screaming "recession, recession..." Within these two days of 27-28th we expect big collapse on stocks and cryptocurrencies.

And what's about the FED? Thus, we've talked about interest rate... How is the Fed's balance sheet QT programme going? And I answer - nohow. As it was announced they have intended to cut balance for ~$47 Bln per month up to $95 Bln within three months. But, They haven't sold anything in June because of extreme interest rates rally,while they have sold just 17.6Bln from 1st -20th of July.

It means that neither the Fed nor the ECB are consistent in tightening monetary conditions – they falter as soon as the destabilization of the debt market begins.

But as we've said earlier, the irony is the debt market will inevitably destabilize due to ultimate negative rates. This, in turn, is caused by inflation, which is expanding over the new goods and services every month . Inflation is becoming more stable and structural. To defeat inflation, it is necessary to collapse demand and tough financial conditions. But tough financial conditions can't be set because of the debt market and rising cost of debt servicing. A despair circle.

The Fed balance has contracted for just $66 Bln. from the all time peak.

At the same time due decreasing of US Treasury deposit almost $350 Bln were pumped back into economy (i.e. markets).

Thus, net liquidity has increased for ~ $290 Bln. This explains, why Bitcoin and Stocks are rising by far.

As a result Fed is expanding its balance 2nd week in a row, trying to keep interest rates low.

The despair circle for the US economy is quite the same as for EU. The only difference is in economy size and its power, that provides more time and capacity to the US. With coming interest rate change and despite the recession "sensation" coming, USD stands in much better conditions, and we suggest continuation of long-term EUR/USD trend, keeping valid our major 0.9 target by far.

In recent few months we've dedicated a lot of time to show you the wide picture of economy problems as in EU as in the US and described the relation of all economy sectors, and why ECB and Fed now are in the dead-way. Today it makes sense to update ECB and Fed policies, as we've passed through recent ECB decision and new inflation data and now come to the Fed meeting, PCE numbers and IIQ GDP preliminary data. Depending on what we will see from ECB and Fed policy we could make suggestion on future economy performance.

Before we turn directly to analysis of ECB rate decision, we need to take a look at performance of PMI indicators and recent poll of business in their attitude to current economy conditions. Crisis is just starting, its effect is barely could be signed by far, but it should become more evident within nearest 6 months. For example, here we already could recognize first signs of stagflation - slowing of economy growth, accompanied with inflation:

Here is what most recent Manufacturing Business Survey from Philadelphia Fed Reserve Bank shows.

The diffusion index for current general activity decreased for the fourth consecutive month, falling 9 points to -12.3 in July. It suggests the decreasing of Industrial Production in July-August 2022. Nearly 56 percent of the firms reported increases in input prices, while 3 percent reported decreases; 40 percent of the firms reported no change.

Nearly 79 percent of the firms indicated wages and compensation costs had increased over the past three months, 21 percent reported no change, and none reported decreases. Most firms have reported adjusting their 2022 budgets for wages and compensation since the beginning of the year, with 57 percent noting they are planning to increase wages and compensation by more than originally planned and 14 percent noting they are planning to increase wages and compensation sooner than originally planned.

The firms still expect higher costs across all categories of expenses in 2022, but median expected increases were unchanged or lower than when this question was last asked in April for most categories. Responses indicate a median expected increase of 7.5 to 10 percent for energy and for raw materials and of 5 to 7.5 percent for intermediate goods, health benefits, and total compensation (wages plus benefits).

This recent survey shows the first signs that production activity is decreasing while inflationary pressure, maybe is loosing impulse, but remains at high levels. This is not pleasant combination, guys.

The one of the ways, how inflation deteriorates households' wealth, you could see on example of gasoline demand. Now is summertime, high traveling season but take a look at gasoline consumption - it is decreasing far below 2015-2019 average level. This is because people have no money to pay for it.

This is how inflation works: nominally, people receive a record amount of dollars in the form of salaries, benefits, pensions, but they cannot afford the same amount of goods as yesterday. That is, real life has become worse. It is also interesting that the drop in gasoline demand in the United States does not cause a strong decline in oil prices. The reason for this is its shortage. The only source to set the balance between demand and supply is to take the oil from the US strategic reserves. However, they exhaust soon. If demand does not collapse more by that time, oil prices could go much higher.

Second component is unemployment. We have mentioned it few times, that we expect rising of unemployment in the US (in EU, UK as well) in near term, and expect it to be around 10%. Problems now start to catching up with the companies and Initial claims stubbornly rising, for the 8 weeks in a row, reaching the levels of Nov 2021. Not the numbers per se are interesting but the tendency, how they are increasing.

Situation in Europe hardly looks better. Recent EU CPI shows 9.6% level and this is not the ceil yet. The structure of price rising envelops all spheres. It is not necessary to talk about electricity and energy. Food is rising for 12%, Transportation - 16%, home rent and utilities - 18%, other non-food and energy goods rising for 5%.

But, it is not the CPI inflation that makes us worry. CPI numbers have not become a surprise. Take a look at these two indicators and how strong correlated they are. Business activity is lagging, and supposedly should keep dropping. It is understandable now. Energy crisis provokes economy crisis, which in turn has triggered political crisis as well.

There are all signs of economic degradation. The consumer confidence index against the backdrop of record price growth in the Eurozone has collapsed to its historic low – it has never been as bad as in July 2022. Neither in 2008-2009, nor in the debt crisis of 2010-2012, nor even in the COVID crisis of 2020.

Not only the minimum levels of consumer confidence for all time are reached here, but the rate of degradation is also remarkable. The breaking point is February 2022, when consumer confidence turned into an uncontrolled collapse.

The resignation of the British Prime Minister, the departure of Italian Prime Minister Mario Draghi, resignations in Estonia, Belgium and Bulgaria, a significant undermining of confidence to Scholz, and finally the drop in the confidence rating of the French president. There is a fragmentation of the European coalition and fragmentation of the political space, center-left forces are growing, there is a risk of expansion of radical political parties against the background of economic collapse.

There are all signs of economic degradation. The consumer confidence index against the backdrop of record price growth in the Eurozone has collapsed to its historic low – it has never been as bad as in July 2022. Neither in 2008-2009, nor in the debt crisis of 2010-2012, nor even in the COVID crisis of 2020.

The graph shows a comparison with the index of economic activity, which has a correlation close to unity with the consumer confidence index. The dynamics are almost completely synchronized, but the collapse of economic activity is not as rapid yet. It means that the worst is yet to come. The system is still based on some inertia, but the processes are running.

With this preview, lets take a look at solution that ECB (and later the Fed as well) has offered to the investors and economists.

ECB MEETING RESULTS

0.5% rate change was not totally unexpected, that we could understand from market reaction. It was very short-term and reversed relatively fast. Most interesting what else C. Lagarde said. The major event of last ECB meeting is an announcement of unlimited QE ("Purchases are not restricted ex ante"). Yes, and don't be surprised with it. Barely ECB has finished PEPP programme as they immediately has started TPI - The Transmission Protection Instrument. It was a lot of sophistics has been used in explanation, but in two words speaking - ECB will monitor the interest rates market of EU countries and use TPI to "fix disproportions" and "to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across the euro area" . Since this "disorderly market dynamics" appears on the interest rates of highly indebted countries, like Italy, Portugal, Spain, Greece, etc., ECB will buy their bonds to hold undesirable rate rising. Instead they will sell Germany bonds that have relatively low yield. Also it is noted that TPI might be applied not only to government but to corporate sector as well (Uniper, RWE ??).

Thus, ECB intends to plug holes in EU countries despite of budget policy, Debt/GDP ratio etc. The priority direction is the reinvestment of securities from "strong participants" to the purchase of securities of "weak participants". However, the news is that the ECB allows an increase in the balance sheet if the pace of reinvestment is not enough to stabilize the market. That's the wonderful way they are trying to beat inflation... And the major conclusion is - ECB capitulates and keep printing money while inflation will keep going higher. Such perspectives suggest further weakness of EUR/USD.

Well, although ECB starts QE, but it did it publicly, while FED is trying to play spies game. We're coming to turning point on next week. First is, market anticipates 1.0% rate change. Many traders suppose that it is already mostly priced-in. We agree but only for tactical, speculating purposes in a moment of decision release US dollar could drop as traders will start "selling on the fact". But not in long-term, as it is difficult to accept high 2.5-2.75% interest rate now. And after short-term profit taking, the major tendency continues.

Next hit will come from earning reports on 27th of July. Microsoft and Alphabet Inc. (Google) are expected to report earnings on 07/26/2022 after market close. According to Zacks Investment Research, based on 12 analysts' forecasts, the consensus EPS forecast for the quarter is $1.28. Microsoft EPS according to Zacks Investment Research is $2.28. The reported EPS for the same quarter last year was $2.17. It is rumor that reports will be worse than expected.

Finally, on 28th of July, the US economy officially steps in recession as IIQ GDP numbers will be negative:

Next day we also get PCE index, personal income and consumption that are also vital to the whole picture.

So, be prepared to verbal intervention across all media screaming "recession, recession..." Within these two days of 27-28th we expect big collapse on stocks and cryptocurrencies.

And what's about the FED? Thus, we've talked about interest rate... How is the Fed's balance sheet QT programme going? And I answer - nohow. As it was announced they have intended to cut balance for ~$47 Bln per month up to $95 Bln within three months. But, They haven't sold anything in June because of extreme interest rates rally,while they have sold just 17.6Bln from 1st -20th of July.

It means that neither the Fed nor the ECB are consistent in tightening monetary conditions – they falter as soon as the destabilization of the debt market begins.

But as we've said earlier, the irony is the debt market will inevitably destabilize due to ultimate negative rates. This, in turn, is caused by inflation, which is expanding over the new goods and services every month . Inflation is becoming more stable and structural. To defeat inflation, it is necessary to collapse demand and tough financial conditions. But tough financial conditions can't be set because of the debt market and rising cost of debt servicing. A despair circle.

The Fed balance has contracted for just $66 Bln. from the all time peak.

At the same time due decreasing of US Treasury deposit almost $350 Bln were pumped back into economy (i.e. markets).

Thus, net liquidity has increased for ~ $290 Bln. This explains, why Bitcoin and Stocks are rising by far.

As a result Fed is expanding its balance 2nd week in a row, trying to keep interest rates low.

The despair circle for the US economy is quite the same as for EU. The only difference is in economy size and its power, that provides more time and capacity to the US. With coming interest rate change and despite the recession "sensation" coming, USD stands in much better conditions, and we suggest continuation of long-term EUR/USD trend, keeping valid our major 0.9 target by far.

Last edited: