Sive Morten

Special Consultant to the FPA

- Messages

- 18,680

Fundamentals

We've got bulk of data that significantly shifts the expectations of investors. Revised CPI, PPI numbers together with strong Retail Sales have pushed hawkish expectations from the Fed and 0.5% rate change on March 1st, raises on horizon again. At the same time, investors argue what the reason was to change CPI calculation method, so we will share our version with you.

Market overview

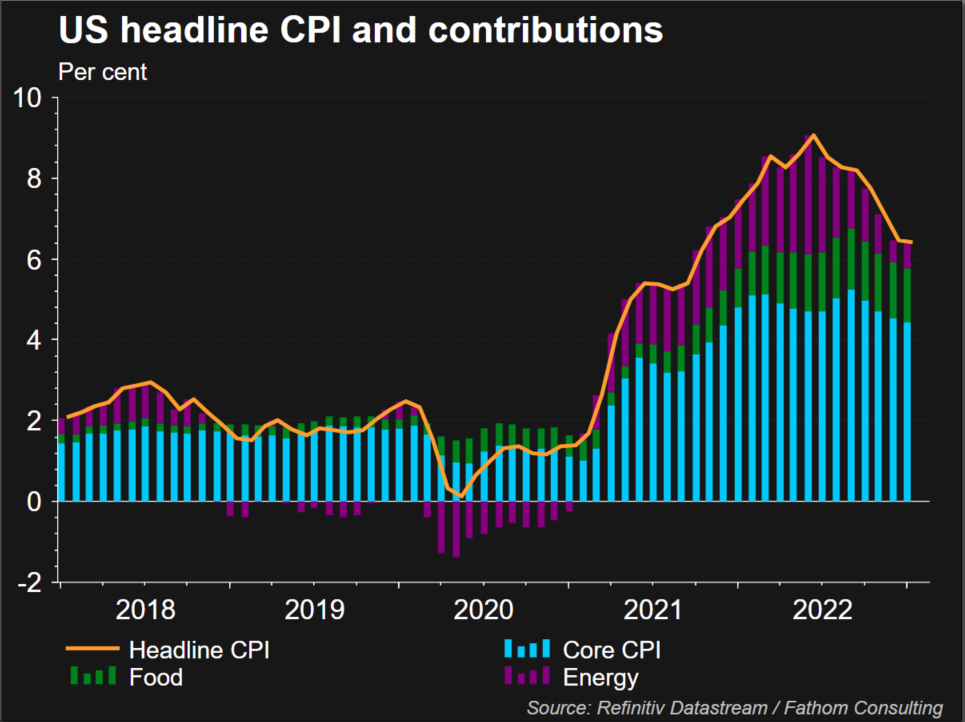

The Labor Department's Consumer Price Index increased 0.5% last month after gaining 0.1% in December, data showed. Monthly inflation was boosted in part by rising gasoline prices, which increased 3.6% in January. But in the 12 months through January, the CPI grew 6.4%, the smallest gain in about 1-1/2 years, and followed a 6.5% rise in December. January's annual CPI rate though was higher than market forecasts for a 6.2% gain.

The dollar climbed to a six-week peak against a currency basket after the release of hotter-than-expected U.S. retail sales data on Wednesday, bolstering investors' expectations that the Federal Reserve would keep monetary policy tight for some time to fight stubbornly high inflation. Data showed that U.S. retail sales surged 3.0% last month, increasing by the most in nearly two years. The numbers for December were unrevised to show sales dropping 1.1%. Economists polled by Reuters had forecast sales would increase 1.8%, with estimates ranging from 0.5% to 3.0%.

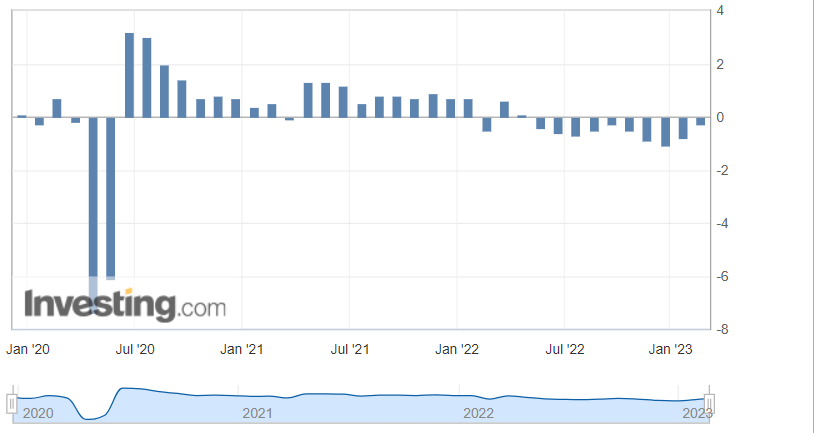

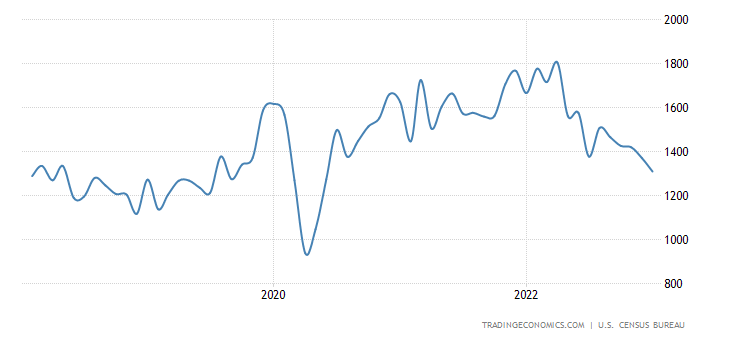

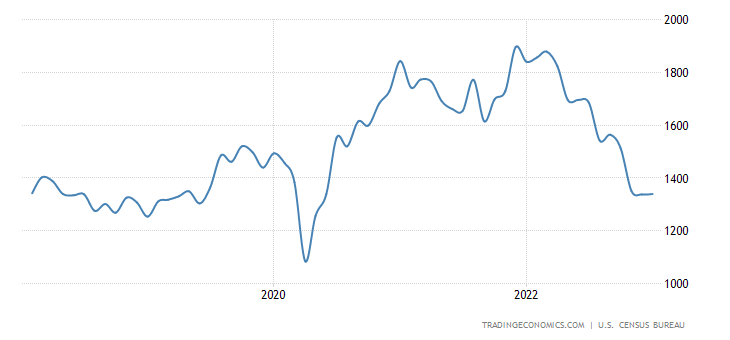

We could say that the American consumer demonstrates amazing resilience, which is at odds with classical monetary theory and the main economic models operated by the Fed and leading international agencies. So 3% up MoM at par in January 2023 after declining 1.1% in the previous two months. Accordingly, in one month the failure of November-December was compensated and reached the next maximum in terms of expenses.

Technical reason for this volatility stand partially in the broken seasonal adjustment factor , which in November-December strongly "downplays" the volume of sales, boosting them at the beginning of the next year. Looking at a broader retrospective, adjusted for inflation, we could see that extended stagnation since June 2021. Sales are very strong by historical standards, but have not been growing for the last 1.5 years, artificially maintaining a high base on domestic doping.

This should knock the rug out from under the Fed's doves at the next meeting.

Deutsche Bank economists said they now expect the Fed to raise the policy rate to as high as 5.6%, having previously expected a 5.1% peak.

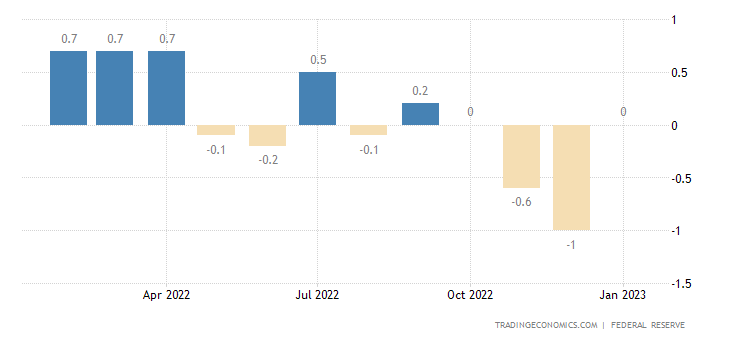

The U.S. producer price index bounced to 0.7% in January, after declining 0.2% in December. Meanwhile, jobless claims unexpectedly fell to 194,000, compared to the 200,000 claims expected, according to a Reuters poll.

BNY's Velis said stronger labor market data and sticky inflation certainly solidified the "higher for longer" school of thought on rates. The interest rate futures market shows U.S. rates could peak close to 5.25% by July before dropping to 5.0% by the end of the year. However, the question for market watchers is how well can the economy continue to hold up, especially as rates head much higher than many originally thought.

The European Central Bank will raise its deposit rate at least twice more, taking the terminal rate to 3.25% in the second quarter, with a vast majority of economists polled by Reuters saying the greater risk is it goes even higher. ECB President Christine Lagarde said at a news conference this month that the euro zone's central bank would add 50 basis points to the deposit rate. Economists took her at her word, with all 57 of them polled in the Feb. 10-15 period expecting a deposit rate hike to 3.00% at the March 16 meeting.

The ECB will follow up on March's move with a further 25-basis-point lift next quarter, medians showed, giving a terminal deposit rate of 3.25% and a refinancing rate of 3.75%. The U.S. Federal Reserve and the Bank of England are also nearing the end of their tightening cycles. But there was no clear consensus in the poll.

Inflation in the 20 countries using the euro fell to an annual rate of 8.5% last month from 9.2% in December, official data showed. While the poll suggested it would continue to fall, it was not expected to reach the ECB's 2.0% target until 2025 at least.

JPMorgan Chase & Co, the largest U.S. bank by assets, is expecting a nearly 20% drop in banking revenue in the first quarter, Chief Financial Officer Jeremy Barnum said at a conference on Tuesday.

Goldman Sachs and Bank of America said they expect the U.S. Federal Reserve to raise interest rates three more times this year, lifting their estimates after data pointed to persistent inflation and a resilient labor market.

Meanwhile, money markets are currently pricing in a terminal rate of 5.3% by July.

Budget deficit is a hidden danger

Another thing that was in a shadow of CPI/Retail Sales report is the US Budget deficit. It is rising. US Treasury has to finance it, the deficit tightly relates to the US Bond market. Problems with the debt ceil and demand for on-the-run securities is a long story that, in turn, relates to the Fed policy and its ability to keep rate at high levels for the long term.

In the first four months of fiscal year 2023 (October 2022-January 2023), the budget deficit rose to $460 billion from $259 billion in the same period in fiscal 2022.

Expenditures increased by 9% (from 1775 billion to 1933 billion), and the main contribution to the growth of expenditures is made not by “injections into the economy” and not by support for business and the population, but by financial transactions. Interest expenses on debt are growing extremely fast - by 42% (from 136 billion to 194 billion).

It is important to note that revenues began to decline. In the first 4 months of fiscal year 2023, revenues fell by 3% at par (1516 - > 1472 billion), where the main negative contribution was made by taxes on individuals, which is likely due to a decrease in collections from rich Americans.

The annual deficit is 1.6 trillion vs 2.3 trillion in January 2022 – this may seem like a positive trend, but in July the annual deficit was less than 1 trillion. The annual expenses of the Ministry of Finance are now 6.4 trillion, and revenues - 4.8 trillion.

If we bring income and expenses in real terms in 2021 prices, we can see that spending has accelerated since July 2022, while income, on the contrary, is declining, which increases the deficit.

Now the increase in spending is influenced by interest, social, medical and defense spending. The deficit could rise to $2 trillion.

Why it is a problem? Most common decision among all investors is the traditional flight to long-dated US Treasuries as a “safe haven” as markets and economies head south. Now a traditional safe haven starts looking more like a death trap. The answers are found in blunt facts and simple math—two themes our policy makers have long-ago decided to cancel, deny or ignore.

In the painful days of 2008 and 2020, U.S. deficits as a percentage of GDP rose by 8% and 10% respectively. After all, bad times require more debt “accommodation”—i.e., more deficit spending and rising growth rates for debt. Heading into 2023, the annual Federal deficit burn rate was already at $1.5T, which is not only embarrassing but dangerous.

Unfortunately, hard math suggests that this figure is likely to get worse in 2023. Much worse.

Using the prior deficit growth percentages (800 and 1000 bps) in 2008 and 2020, respectively, 2023 could mathematically see annualized Federal deficit burn rates hitting $2T to $2.6T, which would conservatively place the U.S. Federal deficit somewhere between $3.5T and $4T in 2023.

But that’s just the beginning. If we then tack on the current -$95B monthly tightening (QT) at the Fed, this would take our 2023 deficit levels near and then past the $5T mark. This, of course, is assuming Powell doesn’t pivot from his QT war on inflation, that we've suggested in our weekly reports last year, risks sending the US markets and economy to lows not seen since well before 1871…

US Treasuries now have negative return, and the growing lack of trust and interest in USTs merely compounds the problem and math of this ticking deficit timebomb.

Powell and Yellen’s myopic and one-sided policy of raising rates and strengthening the USD was an absolute gut-punch to foreign currencies and economies.

This attempt to lure foreign money into the UST market backfired. Instead, it just forced developing and developed nations (from the BRICS to Japan) to dump (sell) USTs in order to defend their own currencies against the otherwise bully-like and unsustainable rise in the USD. Given the foregoing, we could easily witness another $1T in foreign selling of US Treasuries in 2023, which could ostensibly lift that growing US deficit figure above $6T by year end.

The very notion of such a net issuance in USTs suggests that the supply of Uncle Sam’s bonds will be greatly surpassing their demand as we limp into 2023. From high-school econ, we know that such a mis-match in supply and demand means a massive fall in price. Stated otherwise, U.S. Treasuries will be falling like Newton’s apples as yields rise like approaching shark fins.

In short, the need to dramatically increase the supply of USTs to match growing US deficit levels is greatly at odds with the hard fact that natural and foreign demand for those IOUs just aint there anymore… Unless, of course, these new bonds are purchased with mouse-click money and Powell’s so-called war against inflation pivots toward a QE policy of extreme inflation.

Ahhh. The ironies, they do abound. Powell is quite simply cornered. His options are horrific. He either tightens and thus destroys markets and Main Streets, or he loosens and destroys the USD within an inflationary hurricane. Given current policies and trends, it is therefore mathematically safe to suggest that going long those long-dated USTs is more akin to tip-toeing through a minefield rather than sailing into a “safe-haven.”

As maintained throughout 2022, and despite the official narrative to the contrary, our view is that growth rates and yield curves suggest we are already in a recession, and that once that recession becomes official (always a lagging announcement), there will be even more UST issuance and hence even more tanking bond prices.

CPI revision, what for?

Before the publication of the inflation report, the US made a large-scale revision of inflation data, and over the past 6 months, the revision was upward and ... quite radical. From July to December 2022, the average monthly inflation, according to the old data , was 0.16%, and became 0.24%. Given that there is a battle for every tenth of a percent, such a discrepancy matters.

It was previously assumed that from July to December 2022, the cumulative price increase was 0.94% for the broad consumer price index and 2.24% for core inflation excluding food and energy, but according to new data, price increases were 1.45% and 2.53%, respectively.

In other words, over the past six months, it was believed that inflation in the US was slowing down rapidly and reached the goal (0.94% for 6 months is less than 2% per annum, which is right on par with the target), but the revision of the data changed everything.

The data revision has occurred since January 2018, and the further, the more significant the spread. Now the accumulated error is 0.3 p.p. by the cut-off for December, i.e. new data indicate that inflation is higher than expected at 0.3%.

What's with the revision? The change in the weights of the components included in the CPI (we underestimated energy on the assumption that less money is now spent on energy than in June) and the change in the seasonality factor , which is clearly visible on the graph comparing old and new data.

It turned out that the ancient data was underestimated, and the latest data was overestimated and made very “on time”, when it seemed to everyone that inflation had reached the target – an obvious manipulation. There are 6 months ahead, when the seasonal factor will drop about 0.5-0.6 percentage points from inflation over the course of six months.

Conclusion:

So maybe consumer inflation was slightly raised that it could be further reduced? Indeed, it is somehow indecent to show deflation in the current situation, and there is nowhere to lower the official figure of 0.1%, how can we demonstrate a positive effect? Last year's inflation was slightly reduced, and the current one was slightly raised (in order not to show an increase in annual inflation, there is somewhere to reduce it!). However, it is still difficult to talk about the details of this situation. WE just need to watch closely. Most likely, the coming weeks will give a lot of food for thought. By the way, industrial inflation (in terms of the total volume of goods) has fallen slightly:

Whether the methodology was changed here is a separate question. So it is possible that we are generally dealing with local distortions associated with the process of changing methods and in the coming months, as new statistical technologies are developed, these problems will be solved and the picture will become more regular.

But if we draw any conclusion from what happened, assuming that the data correspond to reality, at least in part, we can assume that, apparently, it has not yet been possible to launch the investment process in the United States -

Estimates of the US economy do not change. The New York Fed index has been in the red for the last 3 months and 6 of the last 7 months:

The Philadelphia Fed index has been negative for 6 months in a row, excluding the collapse of 2020, it is the worst since 2009:

Leading indicators in the US have been declining monthly for 10 months in a row:

The number of new buildings in the US has been declining for 5 months in a row. It is minimum for 2.5 years:

And the Building Permits:

The decline in industrial production and the construction sector is visible to the naked eye, both in the United States and in other countries. But, apparently, the main problem is the obvious stagnation of the investment process. This can be seen from the fact that another serious growth of the stock market has begun, and this time it is not accompanied by large liquidity injections of Central Banks. The question is — where does the money come from?

From the investment sector. It is unprofitable to invest in the construction of new capacities in the conditions of falling consumer demand, so they began to put money into speculative operations. The only exception is budget investment programmes, but there is such a colossal scale of corruption that one can only be horrified. In the United States, numerous programs for the development of new weapons have been launched over the past 20 years, but the only one has been completed ... Everything else is missing, although the money was allocated carefully and even exceeding the initial calculations.

The situation is similar in the European Union, so all attempts to start stimulating growth through budgetary mechanisms are doomed to failure, although they can create some visibility of activity.

The specific of the structural crisis is that it migrates from one industry to another. The rate was raised to combat inflation — problems began in the construction industry. The money supply began to be squeezed — the standard of living of the population and the volume of retail sales began to fall. If we start maintaining sales volume tomorrow, inflation will start to rise again.

Actually, there is only one question left: why is inflation rising if demand is falling and money is not being printed? The answer, most likely, is that the decline in demand and the general degradation of technical systems (in the US, first of all) lead to an increase in fixed costs. Roughly speaking, the cost of infrastructure costs per unit of products sold is growing significantly faster than inflation. As a example of expenses - loan servicing can also be included here — the rate is growing, and loan expenses per unit of the goods sold is rising. And, as a result, manufacturers are forced to raise prices even in a situation of declining demand. The only alternative is to increase the issue support of households again, but this will inevitably start to increase inflation.

Ok, keeping lyrics aside, investors are not digging situation as we do, ignoring revision of CPI, problems of rising Budget deficit and so on. They are watching for nominal data, paying no attention to the hidden tricky moments. The nominal picture is relatively clear - economy data is strong. We see falling inflation, strong job market, positive GDP and rising retail sales. It is free hands for the Fed at least for few months. And they definitely will use this situation to rise more. Not occasionally, the 0.5% rate change appears on horizon again. It means that no dollar weakness in near term. While 0.5% coming change from ECB brings no surprise, the same change from the Fed is a different tune. So, it seems that our technical B&B "Sell" trade on monthly chart is start getting fundamental background. Let's focus on nearest target, but keep 0.9 level in mind, who knows...

We've got bulk of data that significantly shifts the expectations of investors. Revised CPI, PPI numbers together with strong Retail Sales have pushed hawkish expectations from the Fed and 0.5% rate change on March 1st, raises on horizon again. At the same time, investors argue what the reason was to change CPI calculation method, so we will share our version with you.

Market overview

The Labor Department's Consumer Price Index increased 0.5% last month after gaining 0.1% in December, data showed. Monthly inflation was boosted in part by rising gasoline prices, which increased 3.6% in January. But in the 12 months through January, the CPI grew 6.4%, the smallest gain in about 1-1/2 years, and followed a 6.5% rise in December. January's annual CPI rate though was higher than market forecasts for a 6.2% gain.

"Month-over-month as expected, but upward revisions for last month brought year-over-year numbers above expectations. This should keep the U.S. dollar strong," said Athanasios Vamvakidis, global head of G10 FX strategy, at Bank of America in London. Inflation in the U.S. is clearly sticky. This will keep the Fed policies on track, keeping the U.S. dollar strong - not necessarily stronger. The big picture is that the inflation data clearly show that the market is too optimistic about inflation dropping enough this year to allow the Fed to start cutting rates."

"The market is leaning toward short dollars for the first part of the year," said Erik Nelson, macro strategist at Wells Fargo in London. "With a CPI number like this and recent activity numbers, it would be hard for the dollar to continue to sell off. I think it will remain relatively strong in the near term."

The dollar climbed to a six-week peak against a currency basket after the release of hotter-than-expected U.S. retail sales data on Wednesday, bolstering investors' expectations that the Federal Reserve would keep monetary policy tight for some time to fight stubbornly high inflation. Data showed that U.S. retail sales surged 3.0% last month, increasing by the most in nearly two years. The numbers for December were unrevised to show sales dropping 1.1%. Economists polled by Reuters had forecast sales would increase 1.8%, with estimates ranging from 0.5% to 3.0%.

We could say that the American consumer demonstrates amazing resilience, which is at odds with classical monetary theory and the main economic models operated by the Fed and leading international agencies. So 3% up MoM at par in January 2023 after declining 1.1% in the previous two months. Accordingly, in one month the failure of November-December was compensated and reached the next maximum in terms of expenses.

Technical reason for this volatility stand partially in the broken seasonal adjustment factor , which in November-December strongly "downplays" the volume of sales, boosting them at the beginning of the next year. Looking at a broader retrospective, adjusted for inflation, we could see that extended stagnation since June 2021. Sales are very strong by historical standards, but have not been growing for the last 1.5 years, artificially maintaining a high base on domestic doping.

This should knock the rug out from under the Fed's doves at the next meeting.

"What all this has done, is it's pushed that terminal rate, just 25 basis points higher than in January. So, now, the terminal rate has been pushed to about 5.25," said Ivan Asensio, head of FX risk advisory at Silicon Valley Bank in San Francisco, referring to the U.S. central bank's benchmark overnight interest rate. "It's not just that we have renewed expectations for now 25 (basis points higher) in March and then 25 as expected in May, but also the possibility that rates have to stay higher for longer. So, where is the plateau? Every day that goes by, the 2% (inflation) target for the Fed seems a bit far into the distance," he added.

Deutsche Bank economists said they now expect the Fed to raise the policy rate to as high as 5.6%, having previously expected a 5.1% peak.

The U.S. producer price index bounced to 0.7% in January, after declining 0.2% in December. Meanwhile, jobless claims unexpectedly fell to 194,000, compared to the 200,000 claims expected, according to a Reuters poll.

"The strong PPI data and hawkish speak from Cleveland Fed President (Loretta) Meister have raised rate expectations further and this is keying the dollar’s upward move today," said John Velis, FX and macro strategist at BNY Mellon Markets in New York.

BNY's Velis said stronger labor market data and sticky inflation certainly solidified the "higher for longer" school of thought on rates. The interest rate futures market shows U.S. rates could peak close to 5.25% by July before dropping to 5.0% by the end of the year. However, the question for market watchers is how well can the economy continue to hold up, especially as rates head much higher than many originally thought.

"We've had a trend of strong data," said Michael O’Rourke, chief market strategist at JonesTrading. "The PPI was the latest, the straw that broke the camel's back, making investors think we should be concerned. Then 15 minutes later Meister came out and said she saw a compelling case for 50 basis points rate hike at the meeting earlier this month. With the strong data we've had it gets people concerned the Fed is behind the curve on inflation once again."

The European Central Bank will raise its deposit rate at least twice more, taking the terminal rate to 3.25% in the second quarter, with a vast majority of economists polled by Reuters saying the greater risk is it goes even higher. ECB President Christine Lagarde said at a news conference this month that the euro zone's central bank would add 50 basis points to the deposit rate. Economists took her at her word, with all 57 of them polled in the Feb. 10-15 period expecting a deposit rate hike to 3.00% at the March 16 meeting.

The ECB will follow up on March's move with a further 25-basis-point lift next quarter, medians showed, giving a terminal deposit rate of 3.25% and a refinancing rate of 3.75%. The U.S. Federal Reserve and the Bank of England are also nearing the end of their tightening cycles. But there was no clear consensus in the poll.

Inflation in the 20 countries using the euro fell to an annual rate of 8.5% last month from 9.2% in December, official data showed. While the poll suggested it would continue to fall, it was not expected to reach the ECB's 2.0% target until 2025 at least.

JPMorgan Chase & Co, the largest U.S. bank by assets, is expecting a nearly 20% drop in banking revenue in the first quarter, Chief Financial Officer Jeremy Barnum said at a conference on Tuesday.

Goldman Sachs and Bank of America said they expect the U.S. Federal Reserve to raise interest rates three more times this year, lifting their estimates after data pointed to persistent inflation and a resilient labor market.

"In light of the stronger growth and firmer inflation news, we are adding a 25bp (basis points) rate hike in June to our Fed forecast, for a peak funds rate of 5.25%-5.5%," Goldman Sachs economists led by Jan Hatzius said in a note dated Thursday.

Meanwhile, money markets are currently pricing in a terminal rate of 5.3% by July.

BofA Global Research also expects a 25bps hike in the Fed's June meeting, pushing the terminal rate up to a 5.25%-5.5% range. Resurgent inflation and solid employment gains mean the risks to this (only two interest rate hikes) outlook are too one-sided for our liking," BofA wrote in a client note.

Budget deficit is a hidden danger

Another thing that was in a shadow of CPI/Retail Sales report is the US Budget deficit. It is rising. US Treasury has to finance it, the deficit tightly relates to the US Bond market. Problems with the debt ceil and demand for on-the-run securities is a long story that, in turn, relates to the Fed policy and its ability to keep rate at high levels for the long term.

In the first four months of fiscal year 2023 (October 2022-January 2023), the budget deficit rose to $460 billion from $259 billion in the same period in fiscal 2022.

Expenditures increased by 9% (from 1775 billion to 1933 billion), and the main contribution to the growth of expenditures is made not by “injections into the economy” and not by support for business and the population, but by financial transactions. Interest expenses on debt are growing extremely fast - by 42% (from 136 billion to 194 billion).

It is important to note that revenues began to decline. In the first 4 months of fiscal year 2023, revenues fell by 3% at par (1516 - > 1472 billion), where the main negative contribution was made by taxes on individuals, which is likely due to a decrease in collections from rich Americans.

The annual deficit is 1.6 trillion vs 2.3 trillion in January 2022 – this may seem like a positive trend, but in July the annual deficit was less than 1 trillion. The annual expenses of the Ministry of Finance are now 6.4 trillion, and revenues - 4.8 trillion.

If we bring income and expenses in real terms in 2021 prices, we can see that spending has accelerated since July 2022, while income, on the contrary, is declining, which increases the deficit.

Now the increase in spending is influenced by interest, social, medical and defense spending. The deficit could rise to $2 trillion.

Why it is a problem? Most common decision among all investors is the traditional flight to long-dated US Treasuries as a “safe haven” as markets and economies head south. Now a traditional safe haven starts looking more like a death trap. The answers are found in blunt facts and simple math—two themes our policy makers have long-ago decided to cancel, deny or ignore.

In the painful days of 2008 and 2020, U.S. deficits as a percentage of GDP rose by 8% and 10% respectively. After all, bad times require more debt “accommodation”—i.e., more deficit spending and rising growth rates for debt. Heading into 2023, the annual Federal deficit burn rate was already at $1.5T, which is not only embarrassing but dangerous.

Unfortunately, hard math suggests that this figure is likely to get worse in 2023. Much worse.

Using the prior deficit growth percentages (800 and 1000 bps) in 2008 and 2020, respectively, 2023 could mathematically see annualized Federal deficit burn rates hitting $2T to $2.6T, which would conservatively place the U.S. Federal deficit somewhere between $3.5T and $4T in 2023.

But that’s just the beginning. If we then tack on the current -$95B monthly tightening (QT) at the Fed, this would take our 2023 deficit levels near and then past the $5T mark. This, of course, is assuming Powell doesn’t pivot from his QT war on inflation, that we've suggested in our weekly reports last year, risks sending the US markets and economy to lows not seen since well before 1871…

US Treasuries now have negative return, and the growing lack of trust and interest in USTs merely compounds the problem and math of this ticking deficit timebomb.

Powell and Yellen’s myopic and one-sided policy of raising rates and strengthening the USD was an absolute gut-punch to foreign currencies and economies.

This attempt to lure foreign money into the UST market backfired. Instead, it just forced developing and developed nations (from the BRICS to Japan) to dump (sell) USTs in order to defend their own currencies against the otherwise bully-like and unsustainable rise in the USD. Given the foregoing, we could easily witness another $1T in foreign selling of US Treasuries in 2023, which could ostensibly lift that growing US deficit figure above $6T by year end.

The very notion of such a net issuance in USTs suggests that the supply of Uncle Sam’s bonds will be greatly surpassing their demand as we limp into 2023. From high-school econ, we know that such a mis-match in supply and demand means a massive fall in price. Stated otherwise, U.S. Treasuries will be falling like Newton’s apples as yields rise like approaching shark fins.

In short, the need to dramatically increase the supply of USTs to match growing US deficit levels is greatly at odds with the hard fact that natural and foreign demand for those IOUs just aint there anymore… Unless, of course, these new bonds are purchased with mouse-click money and Powell’s so-called war against inflation pivots toward a QE policy of extreme inflation.

Ahhh. The ironies, they do abound. Powell is quite simply cornered. His options are horrific. He either tightens and thus destroys markets and Main Streets, or he loosens and destroys the USD within an inflationary hurricane. Given current policies and trends, it is therefore mathematically safe to suggest that going long those long-dated USTs is more akin to tip-toeing through a minefield rather than sailing into a “safe-haven.”

As maintained throughout 2022, and despite the official narrative to the contrary, our view is that growth rates and yield curves suggest we are already in a recession, and that once that recession becomes official (always a lagging announcement), there will be even more UST issuance and hence even more tanking bond prices.

CPI revision, what for?

Before the publication of the inflation report, the US made a large-scale revision of inflation data, and over the past 6 months, the revision was upward and ... quite radical. From July to December 2022, the average monthly inflation, according to the old data , was 0.16%, and became 0.24%. Given that there is a battle for every tenth of a percent, such a discrepancy matters.

It was previously assumed that from July to December 2022, the cumulative price increase was 0.94% for the broad consumer price index and 2.24% for core inflation excluding food and energy, but according to new data, price increases were 1.45% and 2.53%, respectively.

In other words, over the past six months, it was believed that inflation in the US was slowing down rapidly and reached the goal (0.94% for 6 months is less than 2% per annum, which is right on par with the target), but the revision of the data changed everything.

The data revision has occurred since January 2018, and the further, the more significant the spread. Now the accumulated error is 0.3 p.p. by the cut-off for December, i.e. new data indicate that inflation is higher than expected at 0.3%.

What's with the revision? The change in the weights of the components included in the CPI (we underestimated energy on the assumption that less money is now spent on energy than in June) and the change in the seasonality factor , which is clearly visible on the graph comparing old and new data.

It turned out that the ancient data was underestimated, and the latest data was overestimated and made very “on time”, when it seemed to everyone that inflation had reached the target – an obvious manipulation. There are 6 months ahead, when the seasonal factor will drop about 0.5-0.6 percentage points from inflation over the course of six months.

Conclusion:

So maybe consumer inflation was slightly raised that it could be further reduced? Indeed, it is somehow indecent to show deflation in the current situation, and there is nowhere to lower the official figure of 0.1%, how can we demonstrate a positive effect? Last year's inflation was slightly reduced, and the current one was slightly raised (in order not to show an increase in annual inflation, there is somewhere to reduce it!). However, it is still difficult to talk about the details of this situation. WE just need to watch closely. Most likely, the coming weeks will give a lot of food for thought. By the way, industrial inflation (in terms of the total volume of goods) has fallen slightly:

Whether the methodology was changed here is a separate question. So it is possible that we are generally dealing with local distortions associated with the process of changing methods and in the coming months, as new statistical technologies are developed, these problems will be solved and the picture will become more regular.

But if we draw any conclusion from what happened, assuming that the data correspond to reality, at least in part, we can assume that, apparently, it has not yet been possible to launch the investment process in the United States -

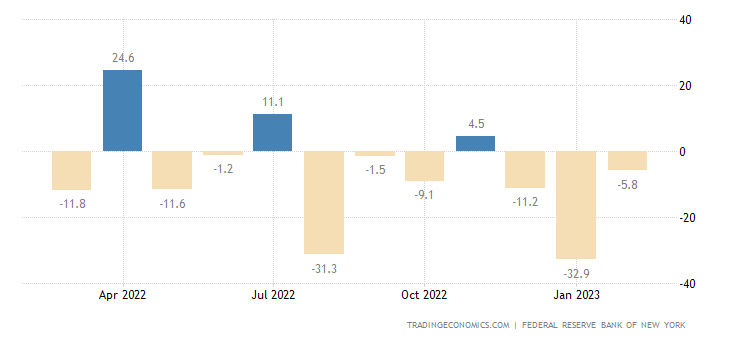

Estimates of the US economy do not change. The New York Fed index has been in the red for the last 3 months and 6 of the last 7 months:

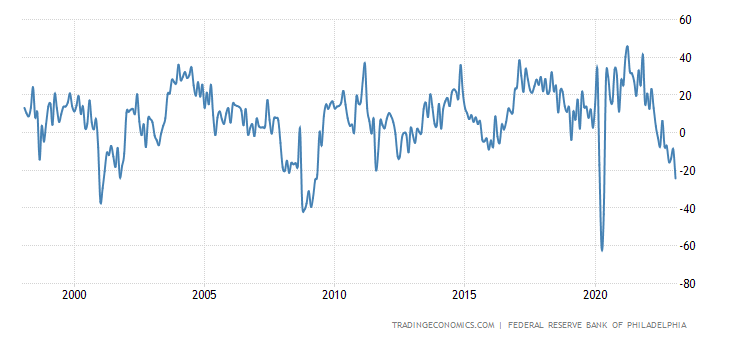

The Philadelphia Fed index has been negative for 6 months in a row, excluding the collapse of 2020, it is the worst since 2009:

Leading indicators in the US have been declining monthly for 10 months in a row:

The number of new buildings in the US has been declining for 5 months in a row. It is minimum for 2.5 years:

And the Building Permits:

The decline in industrial production and the construction sector is visible to the naked eye, both in the United States and in other countries. But, apparently, the main problem is the obvious stagnation of the investment process. This can be seen from the fact that another serious growth of the stock market has begun, and this time it is not accompanied by large liquidity injections of Central Banks. The question is — where does the money come from?

From the investment sector. It is unprofitable to invest in the construction of new capacities in the conditions of falling consumer demand, so they began to put money into speculative operations. The only exception is budget investment programmes, but there is such a colossal scale of corruption that one can only be horrified. In the United States, numerous programs for the development of new weapons have been launched over the past 20 years, but the only one has been completed ... Everything else is missing, although the money was allocated carefully and even exceeding the initial calculations.

The situation is similar in the European Union, so all attempts to start stimulating growth through budgetary mechanisms are doomed to failure, although they can create some visibility of activity.

The specific of the structural crisis is that it migrates from one industry to another. The rate was raised to combat inflation — problems began in the construction industry. The money supply began to be squeezed — the standard of living of the population and the volume of retail sales began to fall. If we start maintaining sales volume tomorrow, inflation will start to rise again.

Actually, there is only one question left: why is inflation rising if demand is falling and money is not being printed? The answer, most likely, is that the decline in demand and the general degradation of technical systems (in the US, first of all) lead to an increase in fixed costs. Roughly speaking, the cost of infrastructure costs per unit of products sold is growing significantly faster than inflation. As a example of expenses - loan servicing can also be included here — the rate is growing, and loan expenses per unit of the goods sold is rising. And, as a result, manufacturers are forced to raise prices even in a situation of declining demand. The only alternative is to increase the issue support of households again, but this will inevitably start to increase inflation.

Ok, keeping lyrics aside, investors are not digging situation as we do, ignoring revision of CPI, problems of rising Budget deficit and so on. They are watching for nominal data, paying no attention to the hidden tricky moments. The nominal picture is relatively clear - economy data is strong. We see falling inflation, strong job market, positive GDP and rising retail sales. It is free hands for the Fed at least for few months. And they definitely will use this situation to rise more. Not occasionally, the 0.5% rate change appears on horizon again. It means that no dollar weakness in near term. While 0.5% coming change from ECB brings no surprise, the same change from the Fed is a different tune. So, it seems that our technical B&B "Sell" trade on monthly chart is start getting fundamental background. Let's focus on nearest target, but keep 0.9 level in mind, who knows...