Bitcoin Fundamental Briefing, December 2021

The Bitcoin and the Fed

What year to come prepares us…

Traditionally December is a quiet month as everybody is watching for the Xmas holidays, and worn out with the worries of the year behind, desire to forget it, at least for the short time of holidays. And this year becomes mostly the same, except a few days of collapse after the Fed meeting.

In December, we met the risk factor that we warned about a few months ago when markets have not completed the reality of hawkish policy announcements yet. Still, everybody understood that this was just a question of time. As we’ve said – don’t be too hasty to treat cryptocurrencies as a replacement of the Gold, like it has full features of the inflation-protected asset. It is the theory and expectations, but the reality might be different. Because Bitcoin in particular and cryptocurrencies, in general, were never before in an environment of hawkish Fed policy and rate hiking cycle. This is the first experience of this kind. We said that Bitcoin reaction depends not on the features of the asset per se but on the place given to it by the global investing society. Whether it is treated like a safe-haven and inflation-protected asset or like a riskier one? And reality confirms our worrying. Once Fed policy change had been announced – Bitcoin collapsed more than 20%. It means that the actual place among riskier assets and not of the primary quality. On the financial hierarchy, it stands lower than stocks as it was sold off, while the stock market mostly was able to hold on to an upside trend.

It means that in 2022 we have to forget about statements that Bitcoin is a gold-featured asset that carries the same qualities. But we should treat it as it has shown itself – as the riskier asset and foresee Fed policy changes concerning it correspondingly.

2021 Market Statistics (By Glassnode)

- Prices are up 78.5% from 1-Jan with a current drawdown of 24.4% from 10-Nov ATH.

- The total supply currently held at a loss is 3.480M BTC, equivalent to 18.34% of the circulating supply.

- Exchange balances saw a net yearly outflow of 67.8k BTC, a decline of just 2.5%.

- Long-Term Holders added 1.846M BTC to their holdings, while Short-Term Holder supply declined by 1.428M BTC.

- Futures Open Interest almost doubled, increasing by $9.57B (97%), while futures trading volume actually declined by 16% to $36.7B/day.

- Mining hash-rate has finished 2021 up 27% on the year, after recovering entirely from the great migration where around 53% of miners were shut-off almost overnight.

- Meanwhile, aggregate miner revenue is up 58% YTD and up over 440% since the halving event in May 2020.

The modest transfer of wealth from Short-Term to Long-Term Holders, despite multiple price ATHs, suggests that 2021 is best described as a macro consolidation and a period of modest accumulation. Such on-chain behavior is more typically observed during Bitcoin bear markets, which in hindsight are effectively lengthy periods of coin redistribution from weaker hands to those with stronger and longer-term convictions.

Notwithstanding Bitcoin’s rocky ride in 2021 and numerous warnings from regulators, investors are making a beeline to snap up the world’s most popular cryptocurrency, according to a survey conducted by Grayscale Investments, the world’s largest digital currency manager and financial market research firm 8 Acre Perspective. Among the key findings:

- More than one-quarter (26%) of surveyed investors already own Bitcoin

- More than half (59%) of surveyed investors are interested in Bitcoin investments – marking a notable increase from 2020 (55%) and 2019 (36%)

- More than half (55%) of investors who currently own Bitcoin began investing over the last 12 months

- Interest in Bitcoin investment products rose significantly among older investors — between ages 55 and 64 (46% in 2021 from 30% in 2020) — and female investors (53% in 2021 from 47% in 2020)

- Most Bitcoin owners (87%) own one or more other digital currencies

Grayscale, which has more than $51 billion in assets under management, also noted that the demographics of bitcoin investors shifted noticeably towards the older generation from previous years.

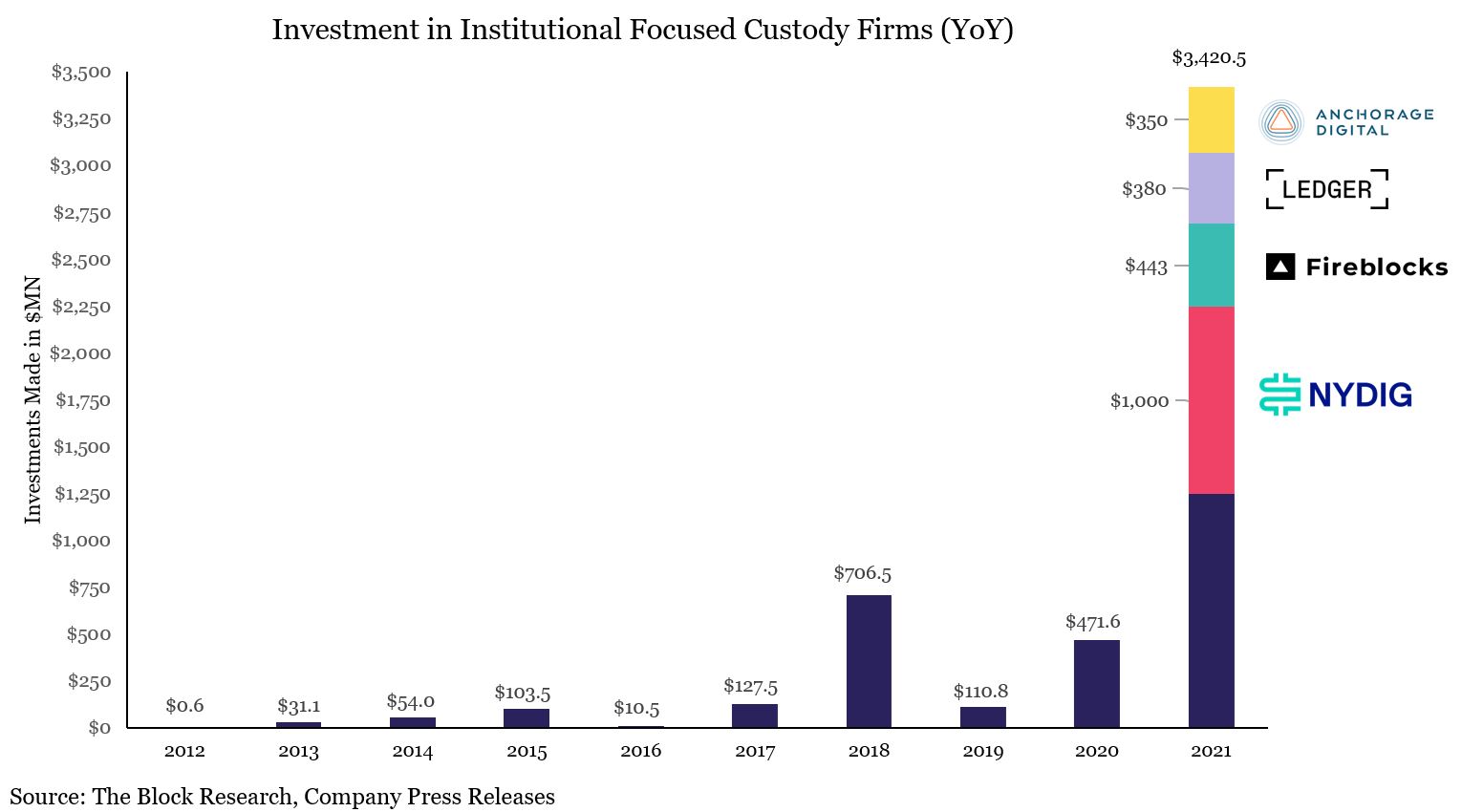

Institutional crypto custodians raised more than $3 billion in 2021

Such firms have raised more than $3 billion this year. As noted in The Block Research’s 2022 Digital Asset Outlook Report, the rate of investments was more than three times higher than 2020.

With yesterday’s announcement of NYDIG’s $1B raise and today’s announcement of Anchorage’s $350M raise, total investments into institutional focused custody firms in 2021 are almost at $3.5B for the year, ~4.8x the amount raised in 2018 the previous record year.

As noted by The Block Research’s Carlos Reyes and Greg Lim, such funding rounds are likely to carry implications for the digital asset industry moving into 2022.

“In 2022, the investments into digital asset custody are likely to bear fruit in the form of enhanced service offerings and continued innovation into the technologies that enable digital asset custody,” they wrote. “The space will also continue to grow as traditional financial institutions such as BBVA, BNY Mellon, and U.S. Bank among others, enter or expand their digital asset offerings, including custody, either directly or by partnering with an existing custodian.”

Volatility, Fed undermine Bitcoin’s inflation hedge claim

With annual U.S. inflation running at its highest since 1982, now would be the perfect time for Bitcoin to stand up and cement its status as a ‘real’ asset, a store of value, and the hedge against inflation its enthusiasts claim.

Many markets the primary cryptocurrency as ‘digital gold’ – due largely to a design that limits its supply akin to the finite reserves of precious metal. And inflows into crypto funds have accelerated in recent months as investors – and notably, policymakers – fret about entrenched inflation.

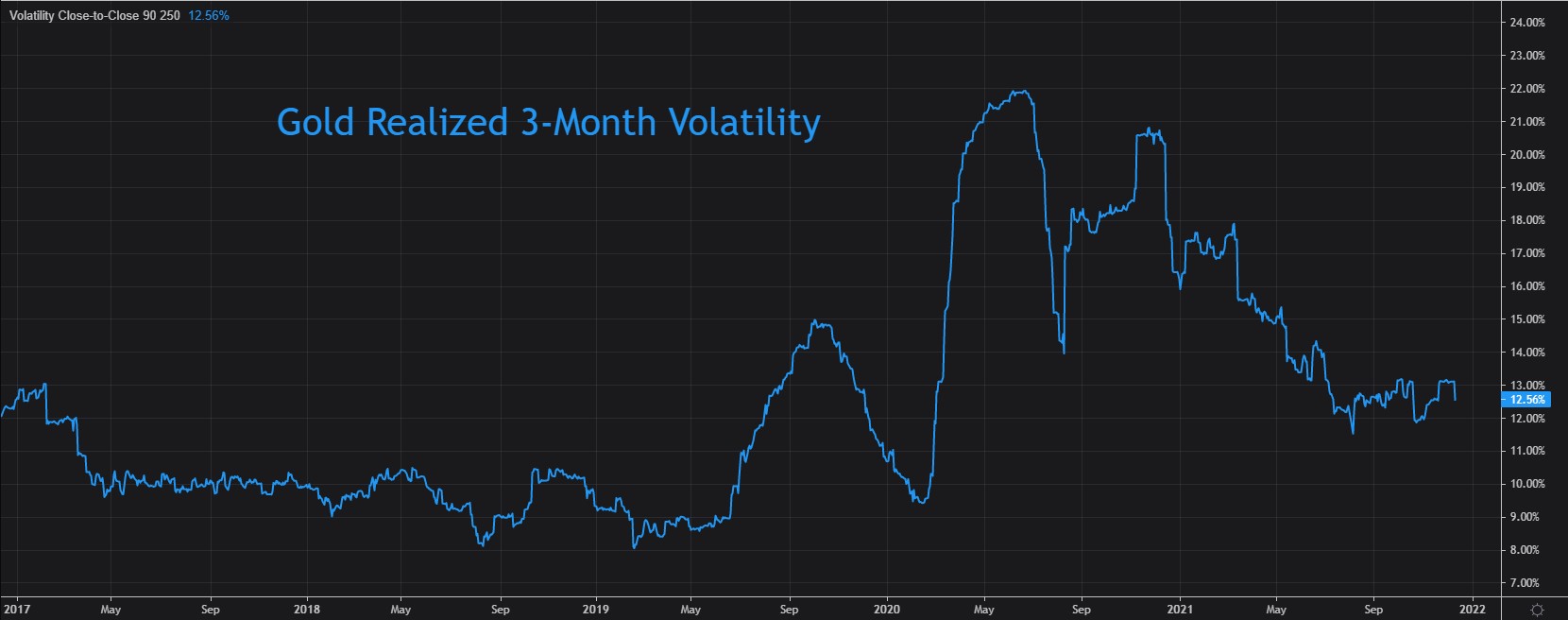

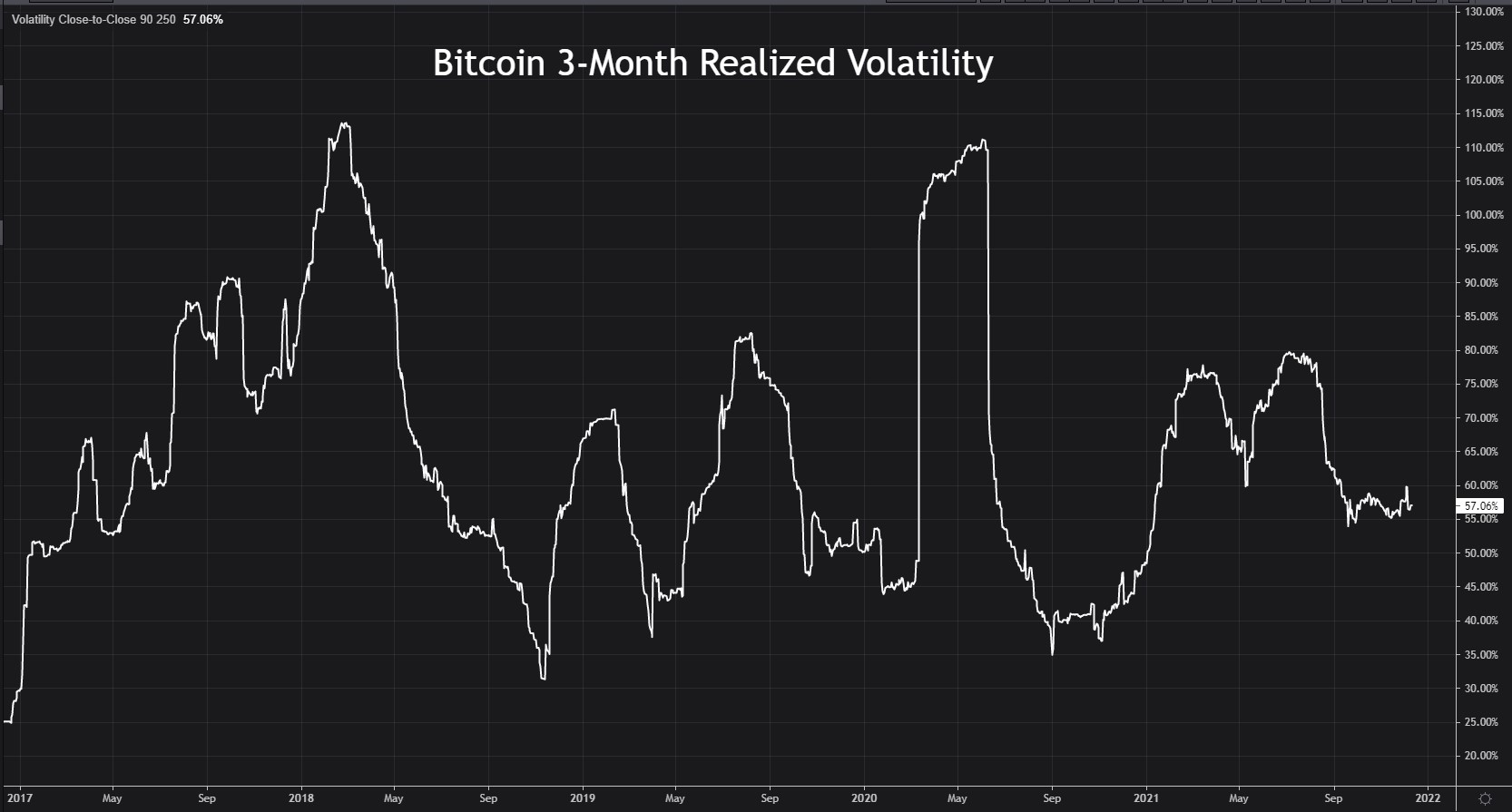

Compared to gold, the world’s oldest and most-established inflation hedge, Bitcoin is far more volatile. Inherently risk-averse investors seeking a relatively safe asset to hedge against rising inflation would at balk that level of volatility in their portfolios.

Unlike gold, however, it rose well into the second half of that two-year tightening cycle, peaking just above 110% in March 2018.

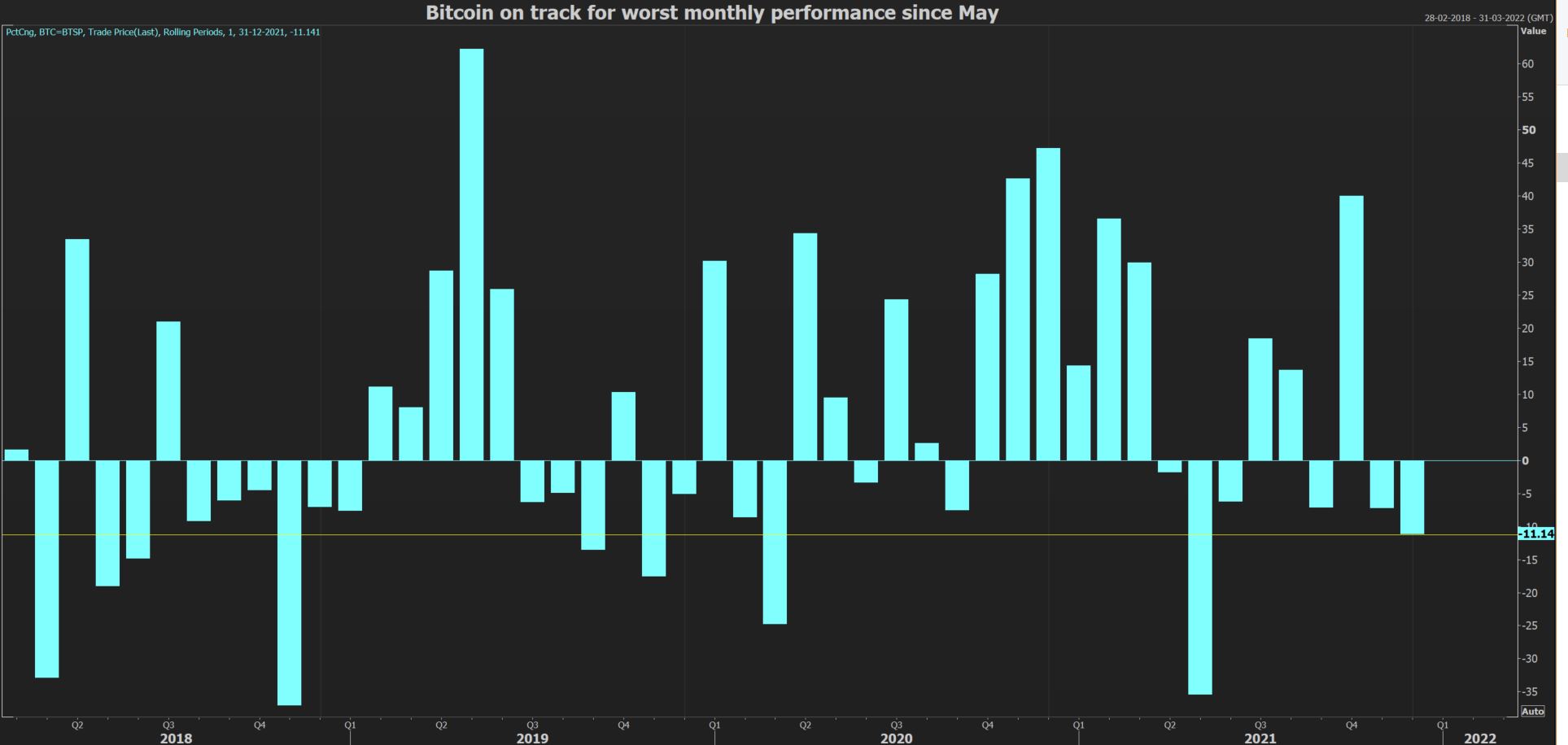

Two major shakeouts this year underscore the risks. Bitcoin plunged 50% over a nine-day period in May, and tumbled another 40% over a few weeks from its all-time high near $70,000 struck on Nov. 10.

According to analysts at UBS, this illustrates why digital gold is nowhere near as viable a hedge against inflation as actual gold. They also note that Bitcoin is far less resilient to equity market drawdowns than gold, another black mark against it as a hedge.

“We view direct exposure in crypto coins and tokens as suitable only for highly risk tolerant and speculative investors, and don’t think they belong within a traditional financial portfolio,” they wrote this week.

JP Morgan‘s Nikolaos Panigirtzoglou, however, argues that volatility is not inconsistent with being a store of value, as shown by gold’s performance in the late 1970s and early 1980s. But it is worth paying close attention to.

The difference between realized Bitcoin vol and gold vol is a key determinant of Bitcoin’s fair value in his framework. When the gap narrows, as it did in mid-2020 to around 2-to-1, Bitcoin’s fair value was around $70,000. A gap now of around 5-to-1 suggests fair value could be less than half that, closer to $30,000.

“Bitcoin is already part of an investor’s portfolio, it is already an institutional asset class. And it will only grow,” he says.

But rising volume doesn’t mean rising price. Look at the global FX market, whose average daily turnover has more than trebled in the last 20 years to $6 trillion. The dollar hasn’t trebled in value.

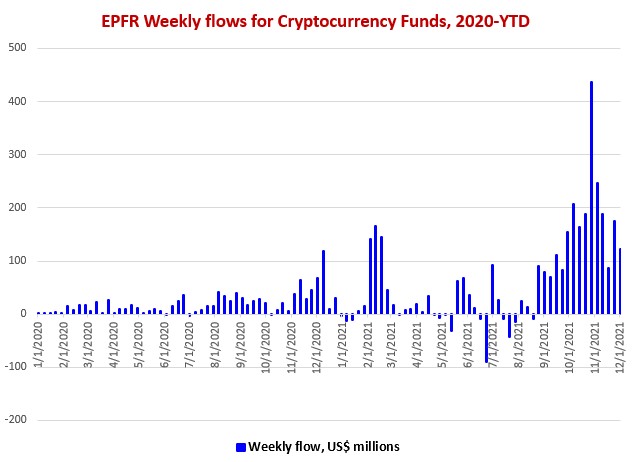

But what of inflation, traditional interest rates and the cost of money? U.S. inflation rose at an annual pace of 6.8% in November, the fastest since 1982. Data from fund flows analysis firm EPFR suggests rising inflation concerns in recent months have stoked demand for Bitcoin and other cryptocurrencies.

Unsurprisingly, expectations on the Fed’s policy response are also shifting. Futures markets now expect the Fed to start raising rates in June – perhaps even earlier – and three hikes of 25 basis points next year are almost fully discounted.

All else being equal, rising rates – especially real rates – rein in inflation expectations and are negative for both inflation hedges and commodity-like tokens such as Bitcoin that have no fixed yield to match.

Real yields have been negative for two years and reached a record low of -1.2% last month. But they may now have troughed and could well climb from here if the Fed follows its hawkish bark with a hawkish bite next year.

This hinges on how inflation behaves in the coming months, of course. The latest numbers show that price pressures are broadening.

So the big problem for Bitcoin is if the Fed feels it has to catch up and raise rates more aggressively. This could lift real yields closer to – maybe even into – positive territory, undermine risk appetite everywhere and potentially crush any inflation-driven support for ‘new money.’

Few dare forecast Bitcoin’s direction after the past five years of eye-watering gains and withering slides – but it will hardly be a refuge for the risk-averse in another market storm.

MARKET SENTIMENT

According to the Fear and Greed index, the market still stands frightened after the December collapse. Now index level stands around 27 points, near the ultimate

Markets have been juggling worries over the Omicron variant of coronavirus over the past weeks, and cryptocurrencies have not been immune.

As per cryptocurrency research firm CryptoCompare, total inflows into digital asset products turned negative in December’s third week. That marks the first time since mid-August.

However, digital products along with other risky assets have caught some Christmas cheer from the so-called “Santa Claus rally” this week. Bitcoin is up about 8% so far this week, on track for its best week in two months.

The MVIS CryptoCompare Digital Assets 100 Index which tracks a basket of the 100 largest digital assets, is on track for monthly losses of 9%.

On the brighter side, CryptoCompare notes that weekly flows in December still average around $43.4 million of inflows each week. Unsurprisingly, bitcoin-based products captured the newest money, averaging $35.6 million of net inflows.

However, ethereum has posted $18.6 million of weekly net outflows on average, the only digital asset tracked to do so.

“Trends remain bearish near-term and momentum has not showed proper evidence of stabilizing in a way that should allow a bounce to unfold just yet,” said Fundstrat in a research note. Most of the trend exhaustion techniques still suggest another 4-6 days lower is likely before any trading low can occur,” it added.

Meanwhile, assets under management in Greyscale investment products dipped 17.1% to $43.9 billion, as per CryptoCompare data. Greyscale products still hold the lion’s share of the digital asset investment market, with a market share of 76.2% of total AUM, but they have lost some ground from the 86.6% they held at the start of 2021.

2022 MARKET OUTLOOK

On New Year’s Day, we do not want to bother you with a lot of information but provide a few things that might be really interesting. The primary topic is the relation between Fed policy and BTC performance in 2022.

In fact, things that Mike McGlone, Bloomberg Intelligence analysts, tells below are not new. We’re talking the same in our weekly reports on the FX market and especially on Gold. A couple of weeks ago, we talked about why markets do not buy the hawkish Fed.

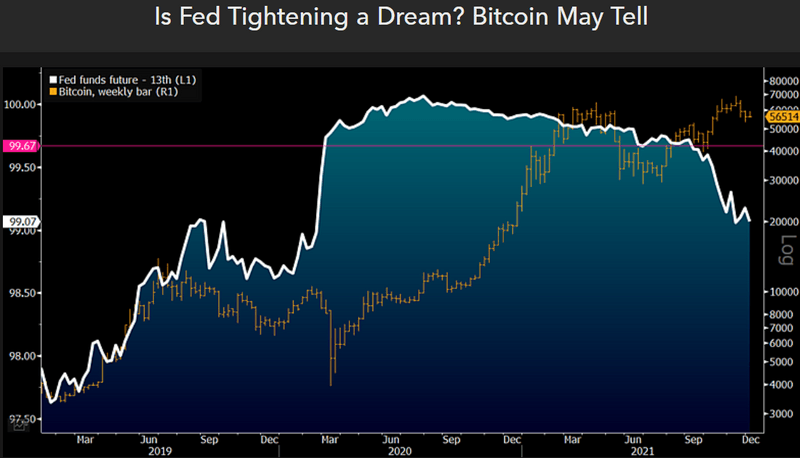

The primary reason for that is a very fragile balance between too high inflation and unstable US economic recovery. While the US economy shows its first shaky steps to recover, inflation is already around 6%. And Fed stands in a very tricky situation when it can’t ignore the inflation and have to struggle it, but at the same time, it scares to hurt the economic recovery. This combination makes investors think that the Fed hardly keeps its hawkish promising to execution and will have to stop halfway. Markets do not believe in a complete tightening cycle that could lead the Fed rate to a 2.15-2.25%. This is the major reason for the dropping in the bond market, which is a major hope for Bitcoin. This is the cornerstone of the potential bullish tendency that everybody hopes to see in 2022.

And Mike points on the same thing here:

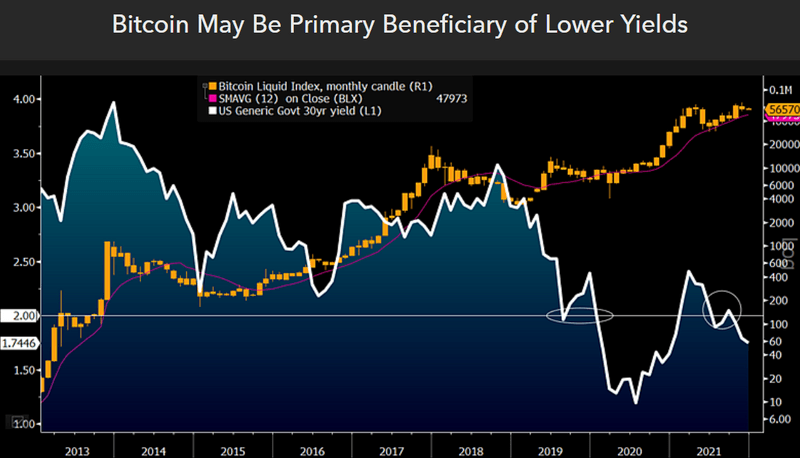

The inability of the U.S. Treasury long bond to sustain above 2%, despite widespread consensus for higher yields, may become a primary indicator of a transition back to a more deflationary environment in 2022 favoring Bitcoin. The long bond first dropped below the 2% threshold in February 2020, signaling the severity of the pandemic. Most risk assets followed in March. Our graphic depicts U.S. yields potentially on a trajectory to follow Japan and Europe into negative territory. The upcoming digital reserve asset may be a top standout to benefit.

Among other reasons for positive BTC performance also suggested

- Proper regulation that should attract conservative and supervised authorities like Pension Funds;

- Oversupply of fiat money;

- Potential deep retracement on the stock market;

- Rising ETF and Hedge Funds interest to cryptocurrencies;

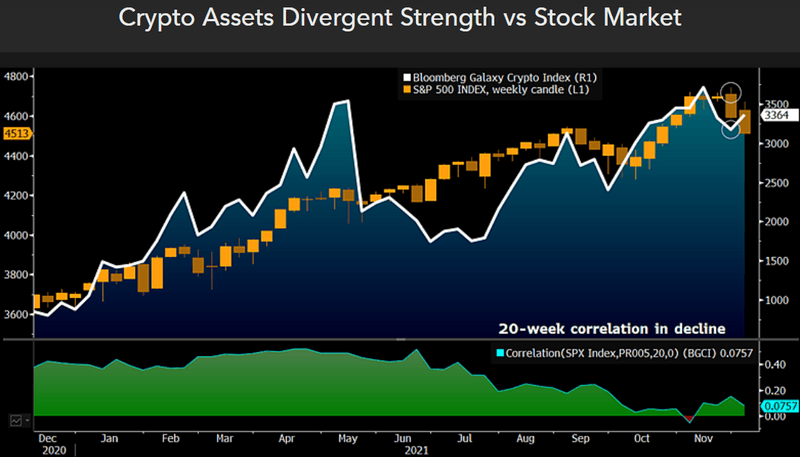

In fact, the Bitcoin market has formed solid retracement this year – not only in May but in December, either. While the stock market shows no proper reaction to changing the Fed policy, a high degree is yet to come. This leads to the divergence among risky assets, stocks, and cryptocurrencies. Bitcoin should be in a better condition and attract some risk capital when it comes.

Here is what Mike tells about it:

Divergent strength vs. the stock market and underpinnings from the sharp drawdown in 2021 may set the stage for further appreciation of cryptocurrency asset prices in 2022. Compared with broad equities, which haven’t had a 10% correction since the 2020 swoon, the crypto market may have a relative advantage in 2022. Our graphic depicts the Bloomberg Galaxy Crypto Index recovering despite the declining S&P 500 at the end of November. Cryptos are risk assets, but the primaries — Bitcoin and Ethereum — may be transitioning toward stores-of-value.

That’s being said, the combination of when the first hawkish Fed steps put pressure on stocks, putting them into downside retracement, and following later backpedal that keeps the interest rates at low levels is the best combination for the cryptocurrencies.

Renewed impetus from the Federal Reserve to take away the punch bowl and declining bond yields may point to a macroeconomic environment in 2022 that favors top cryptocurrencies Bitcoin and Ethereum. Crypto assets showing divergent strength vs. equities near the end of 2021 may portend continued digital-asset outperformance in 2022.

A primary force to reverse expectations for Federal Reserve tightening in 2022 is a drop in the stock market, which may be a bit of a win-win for Bitcoin. The benchmark crypto, well on its way to becoming a digital store-of-value, remains in a price-discovery mode and is a risk asset, and has been rising with the equity tide. Bitcoin will face initial headwinds if the stock market drops, but to the extent that declining equity prices pressure bond yields and incentivize more central-bank liquidity, the crypto may come out as a primary beneficiary.

As a result, ETFs and Hedge funds should pay more interest to cryptocurrencies as its missing in portfolios very soon could be treated as a crime:

Funds have been moving away from old analog gold and toward Bitcoin and Ethereum. The question for 2022 centers on the reversal or acceleration of these flows. With bond yields in decline, our bias is toward the latter.

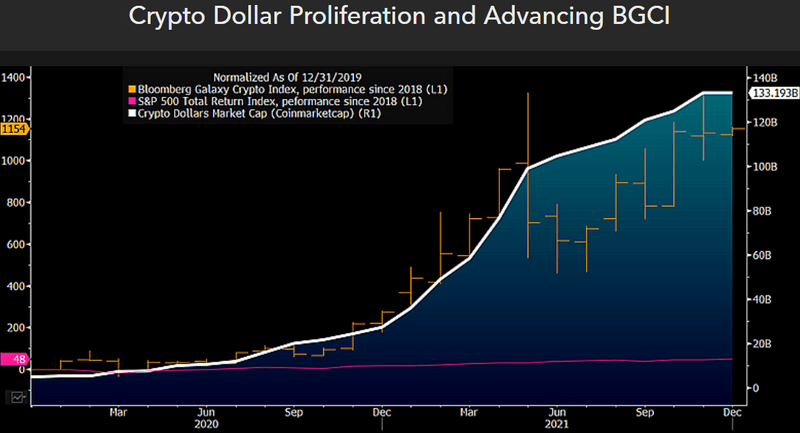

… when a new asset class outperforms incumbents, naysayers have little choice but to join in. We see this process playing a primary role in 2022, as money managers may face greater risks if they continue to have no portfolio allocations to cryptos. Our graphic depicts the Bloomberg Galaxy Crypto Index (BGCI) increasing about 1,200% since the end of 2019 vs. closer to 90% for the S&P 500. Such outsized performance typically comes with volatility, and the almost 60% drawdown in the BGCI in 2021 could add underpinnings for further appreciation in 2022.

The BGCI is 80% Bitcoin and Ethereum. A solid trend of 2021 that we expect to accelerate in 2022 is the proliferation of crypto dollars. Our graphic shows the crypto dollar market cap rising above $130 billion.

Finally, with providing healthy regulation and oversupply of fiat money and limited supply of Bitcoin – it might be treated as a secondary supportive factor for cryptocurrencies in 2022:

We expect the U.S. to embrace cryptocurrencies in 2022, with proper regulation and related bullish price implications. The unlimited supply of fiat currency should sustain rising prices, notably in Bitcoin and Ethereum, which have limited supply. Some normalization in stock-market returns and a continued decline in U.S. Treasury bond yields may shine on Bitcoin and Ethereum in portfolios.

Diminishing supply is a key attribute shared by the top two cryptos. Digital assets, in early adoption-and-migration days into investment portfolios, may have an advantage vs. an extended stock market, at risk of wobbling, notably as the Federal Reserve reduces liquidity.

Mike McGlone concludes:

Representing a better way to transact, a strengthening ecosystem, and an asset class that’s here to stay, crypto dollars are the most significant advancing part of the digital-money revolution and the third leg of the crypto stool. Bull markets in the other two — Bitcoin and Ethereum — look as durable as the advancing market cap of stable coins tracking the dollar.

Overvalued US dollar is another risk factor

The U.S. dollar is trading at a high premium relative to its fundamentals as investors fret over the spread of the Omicron COVID-19 variant and high inflation. But that is unlikely to last, with risks to the currency rising next year, according to The Leuthold Group.

The greenback typically trades with a strong positive correlation to consumer sentiment, however, this relationship reverses when confidence is replaced by fear and then panic, as is currently the case, James Paulsen, chief investment strategist said in a report.

In fact, the safe-haven premium currently priced into the U.S. currency is nearly 40%, the second-highest level since 1988.

“This strongly suggests the U.S. dollar is poised to decline next year,” Paulsen said.

Heading into 2022 investors are concerned about COVID and high inflation but

“there is a decent chance some semblance of victory will be declared over both, which would likely boost confidence and cause the safe-haven premium to evaporate.”

The Omicron variant so far appears to be far less virulent than Delta, and there are more tools and treatments now that can address the virus. The pandemic is also likely to morph into an epidemic, which should help ease supply chain problems, reduce inflation pressures and improve confidence, Paulsen said.

That may mean that the dollar will see a year of renewed weakness, which would boost commodity prices and possibly keep inflation above the Federal Reserve’s 2% target, with 10-year Treasury yields possibly rising above 2%, Leuthold said.

At first glance it seems that overvalued dollar is a bullish factor for Bitcoin, but only if compare them face-to-face. Indeed, a weakened dollar should support Bitcoin price, that is actually traded against it. But the secret stands with the indirect impact of the US Dollar’s weakness on other statistics. Thus, dropping US Dollar supports price rising and accelerates inflation, which pushes Fed to the more aggressive policy that, in turn, leads to real interest rates increasing and will be negative for the Bitcoin market.

It means that in the chain of “US Dollar – Interest rates – (inflation) – Bitcoin” it is needed US dollar to be more or less stable or slightly weaker to avoid triggering of new inflation spiral up. So, markets should calm down a bit around Omicron and pandemic topics but not relax too much to keep demand for the USD. This is the “golden mean” to Bitcoin.

The Bottom Line

Recent Bitcoin performance suggests that our fears of “institualisation” of Bitcoin are not in vain. We’re sure that recent performance and a high degree of sensitivity of major cryptocurrencies to important economical statistics and Fed Reserve policy stands due to the acceleration of the inflow of institutional investors’ money and their big participation in the price dynamic of Bitcoin.

As a result, Bitcoin was just built-in into the common model of assets hierarchy and “proper” reaction on basic principles, such as “rising rates”, “dropping rates”, “higher/lower inflation”, “tighter/lighter Fed policy” etc. Now, as institutional investors own a bulk amount of Bitcoins, the market starts reacting “classically” to major turnings in fiscal policy and the economic cycle.

In 2021 we many times talk about that the coming change of economic cycle and tighter Fed policy might become a tough challenge for the cryptocurrency market and cares a lot of risks as the market meets it never before. And now our fears become a reality. Now it is becoming clear that Bitcoin closely reacts to the behavior of the US interest rates. Some analysts even have found a regression model that describes the relation of BTC price to the level of 10-year interest rates:

BTC = (Y10 — 0,5) * 50 000

And it reflects relation pretty nice, at least at current price levels. Other market members also talk about the extraordinary “institualisation” of Bitcoin.

Sean Farrell, head of digital asset strategy, at Fundstrat cited bitcoin’s “outsized correlation to macro uncertainty,” compared with the rest of the crypto market.

We think this speaks to the overwhelming level of institutionalization of bitcoin over the prior 12 months as well as the independent market dynamics throughout the rest of crypto,” Farrell said. This might explain why there was so much capitulation in bitcoin markets … as legacy institutions look to preserve annual gains heading into year-end,” he added.

Thus, we were correct in our judgment that collapse has happened just because of sell-off in risky assets where investors classify Bitcoin as a reaction to changing of the Fed policy. All 2nd quality risky assets were sold off as well. Even blue-chip stocks have been hurt that day but to less degree.

It means that in 2022 we have to treat Bitcoin correspondingly as strongly sensitive to the changes of Fed policy, major US statistics, and dynamic of interest rates, avoiding romantic BTC idealizing as a “safe-haven” gold-featured asset.

With keeping this reasonable view we should escape any unpleasant “uncertainties” closely watching for mentioned driving factors. How to do it and what to watch for – we’ve discussed above. Now it seems that BTC has good chances to start a new upside bounce because the chances that Fed stifles fragile economic recovery with rising interest rates are relatively high. The first steps of Fed tightening enthusiasm should hurt the stock market as well, which is might be a “win-win” combination. This is what we would like to get.

Then we just need to keep our nose to the wind. In general, more aggressive Fed behavior will be negative for BTC, as well as massive run into “quality” if pandemic will turn to “worst” scenario, which now doesn’t seem as very probable. All other ways seem to be more or less optimistic for BTC’s performance in 2022.

Author Profile

Sive Morten

At the Forex Peace Army, he is known as an author of Forex Military School, which quite unique free forex trading course. We do not know of any other free forex trading education covering such a broad spectrum of forex market concepts in such details while keeping it easy to understand and practically use.

As if that wasn't enough, he is the part of the Shoulders of Giants Program. He shares with his fellow traders at FPA his view and forcast of the Gold Market, Currency Market, and Crypto Market in form of weekly analytics and daily video updates.

* Complete Forex Trading Course by Sive Morten >>

* Sive Morten Forex , Gold , and Crypto Analysis >>

Info

412 Views 0 CommentsComments

Table of Contents

Recent

-

Bitcoin Fundamental Briefing, March 2024 Demystifying Cryptocurrency Nodes: Deep Dive into Polygon Node Ecosystem Strategies for Trading Forex on a Budget Bitcoin Fundamental Briefing, February 2024 Bitcoin Fundamental Briefing, January 2024 Strategic Asset Allocation Techniques for Currency Traders Bitcoin Fundamental Briefing, December 2023 Bitcoin Fundamental Briefing, November 2023