Sive Morten

Special Consultant to the FPA

- Messages

- 18,644

Fundamentals

This week we've got few important events and data. First is Dollar Index (and EUR) has hit long-term target and resistance area that let us hope to get some good trading setups within few weeks. Inflation pressure is rising and now accompanied with good numbers on consumption and personal spending that makes people more and more talk about Fed policy change sooner rather than later. Finally, the spike in EU inlfation that mostly was missed by wide market society seems important to us, because it perfectly fits to technical picture that suggest EUR upward bounce. We've discussed this spike in last report and suggest that Germany inflation could peak around 5% in next month. So, this should shake sleeping ECB a bit.

Market overview

The U.S. dollar advanced on Monday, bolstered by the rise in Treasury yields ahead of a slew of Federal Reserve speakers this week who could affirm expectations of the start of asset purchase reduction before the end of the year. U.S. benchmark 10-year Treasury yields hit a three-month high of $1.516%.

The greenback also extended gains after data showed new orders and shipments of key U.S.-made capital goods increased solidly in August, rising 0.5% in August amid strong demand for computers and electronic products.

But the market has been more focused on the U.S. Treasury market. U.S. yields climbed to their highest since late June in anticipation of tighter monetary policy after the Fed announced last week it may start tapering stimulus as soon as November and flagged interest rate increases may follow sooner than expected.

The euro largely ignoring developments in German elections over the weekend, with the Social Democrats projected to narrowly defeat the CDU/CSU conservative bloc.

U.S. Treasury Secretary Janet Yellen, said on Tuesday that U.S. inflation at the end of the year would be closer to 4%, double the Fed target.

The dollar surged on Wednesday to a one-year high against major currencies, boosted by increased expectations for a reduction in the U.S. Federal Reserve's asset purchases starting in November and an interest rate hike, possibly in late 2022.

The greenback also fared well despite an impasse in Washington over the U.S. debt ceiling that threatened to plunge the government into a shutdown. The world's largest reserve currency, seen as a safe-haven bet at times of market stress, has strengthened in recent days as investors instead focused on fears of a global slowdown, a rise in energy prices and higher U.S. Treasury yields.

Traders are also concerned that the Fed will start to withdraw policy support just as global growth slows.

Erik Nelson, macro strategist at Wells Fargo in New York, sees a further 2% to 3% upside in the dollar index.

The dollar began the last quarter of 2021 near its highest levels of the year and headed for its best week since June, as currency markets braced for U.S. interest rates to rise before those of major peers.

A Federal Reserve meeting last week reinforced expectations for asset purchase tapering beginning this year and rate hikes starting in 2022 or early in 2023.

"As long as markets remain confident that the U.S. is going to start tightening monetary policy within a reasonable timeframe, the dollar should remain well supported and eventually rise 5-10% from current levels," said Societe Generale strategist Kit Juckes. "The prospect of the European Central Bank keeping rates below zero while the Fed hikes should keep euro/dollar in the post-2014 range, with a centre of gravity around $1.12-1.16," he said.

Commodity currencies made a bounce on the dollar on Thursday following a Bloomberg report which said China had ordered energy companies to secure supplies for the winter at all costs, citing unnamed people familiar with the matter. Beijing is scrambling to deliver more coal to utilities to restore supply amid a power crunch that has unsettled markets due to the likely hit to economic growth.

Cautious market sentiment due to COVID-19 concerns, wobbles in China’s growth and a Washington gridlock ahead of a looming deadline to lift the U.S. government’s borrowing limit also lent support to the dollar which is seen as a safe-haven asset.

Benchmark 10-year Treasury yields are up for a sixth straight week and real 10-year yields, discounted for inflation, are rising far more quickly than counterparts in Europe.

U.S. consumer spending surged in August, but outlays adjusted for inflation were weaker than initially thought in the prior month, reinforcing expectations that economic growth slowed in the third quarter as COVID-19 infections flared up. Consumer spending, which accounts for more than two-thirds of U.S. economic activity, rebounded 0.8% in August. Data for July was revised down to show spending dipping 0.1% instead of gaining 0.3% as previously reported.

Inflation maintained its upward trend in August, though price pressures have probably peaked. The personal consumption expenditures (PCE) price index, excluding the volatile food and energy components, climbed 0.3% after increasing by the same margin in July. In the 12 months through August, the so-called core PCE price index increased 3.6%, matching July's gain.

The core PCE price index is the Federal Reserve's preferred inflation measure for its flexible 2% target. The U.S. central bank last week upgraded its core PCE inflation projection for this year to 3.7% from 3.0% back in June.

Inflation could remain high for a while. A survey from the Institute for Supply Management on Friday showed manufacturers experienced longer delays getting raw materials delivered to factories and paid higher prices for inputs in September.

High inflation is cutting into spending. Real consumer spending rose 0.4% in August following a downwardly revised 0.5% drop in July. With the August and July data in hand, economists predicted that growth in consumer spending would probably brake to around a 1% annualized rate in the third quarter.

The Atlanta Fed cut its GDP estimate for the quarter to a 2.3% rate from a 3.2% pace. Slower growth was reinforced by a third report from the Commerce Department showing construction spending flat in August.

The economy remains supported by record corporate profits. Households accumulated at least $2.5 trillion in excess savings during the pandemic. Coronavirus infections are trending down, which is already leading to a rise in demand for travel and other high-contact services. Businesses need to replenish depleted inventories, which will keep factories humming.

U.S. manufacturing activity picked up further in September, but factories experienced longer delays getting raw materials delivered and paid higher prices for inputs.

The Institute for Supply Management (ISM) said on Friday its index of national factory activity increased to a reading of 61.1 last month from 59.9 in August.

Euro zone and British manufacturing growth remained strong but activity suffered from logistical issues, product shortages and a labour crunch that are likely to persist and keep inflationary pressures high. IHS Markit's final manufacturing Purchasing Managers' Index (PMI) sank to 58.6 in September from August's 61.4 and Britain's PMI fell for a fourth month in a row, dropping to 57.1 from 60.3.

Inflation in the common currency area jumped to a 13-year high of 3.4% last month, preliminary official data showed on Friday, well above the European Central Bank's 2.0% target.

Core inflation excluding food and energy rose to 1.9% from 1.6%, as did a narrower measure that also excludes alcohol and tobacco.

A grinding rally in the dollar is picking up speed, fueled by a hawkish tilt from the Federal Reserve, rising Treasury yields and concerns over the possibility of a drawn-out battle to raise the U.S. debt ceiling.

The greenback is up 4.7% year-to-date and stands near its highest level in a year against a basket of currencies. Net bets on the dollar in futures markets are at a more than 18-month high, according to data from the CFTC.

Yields on 10-year United States Treasury Inflation Protected Securities , which strip out inflation, have risen by about 37 basis points since early August, compared with a gain of only 5 basis points for its German counterpart. That has increased the attractiveness of dollar-denominated Treasuries compared with their foreign counterparts.

COT Report

We do not see yet how results of this week impact the net position, but I dare to suggest that hardly it is very positive to EUR. Meantime, last week performance has negative impact on EUR net position. It has dropped, keeping downside trend that is started in June of last year.

COT data shows that net short position has increased this week as traders have opened more short positions. Open interest has increased for 10K. That combination suggests that overall sentiment stands moderately bearish for EUR.

Next week to watch

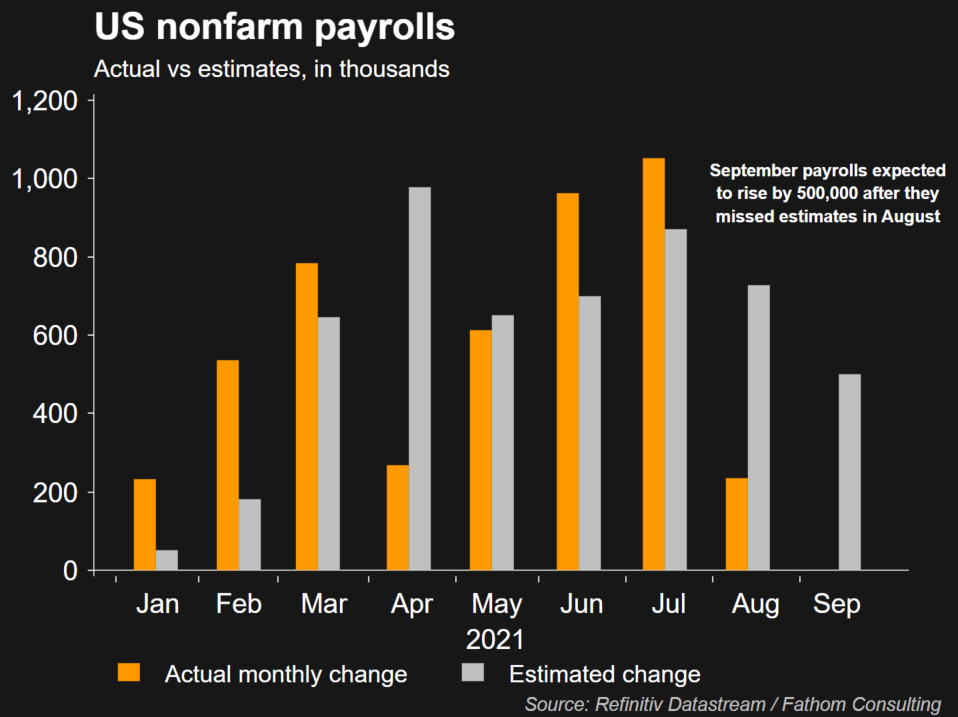

#1 US NFP Data

In September, the U.S. Fed said trimming monthly bond purchases could be warranted "soon"; Chair Jerome Powell noted it'll take one more "decent" jobs report to set the wheels in motion - not a "super-strong" one, just one that's "reasonably good". Will Friday's September nonfarm numbers - the last official jobs report before the Fed's November meeting - do the trick?

A Reuters poll expects 500,000 jobs were added after August's massive miss. Stronger-than-expected numbers might fuel fears the Fed could wind down easy-money policies faster than anticipated, potentially causing more market turbulence.

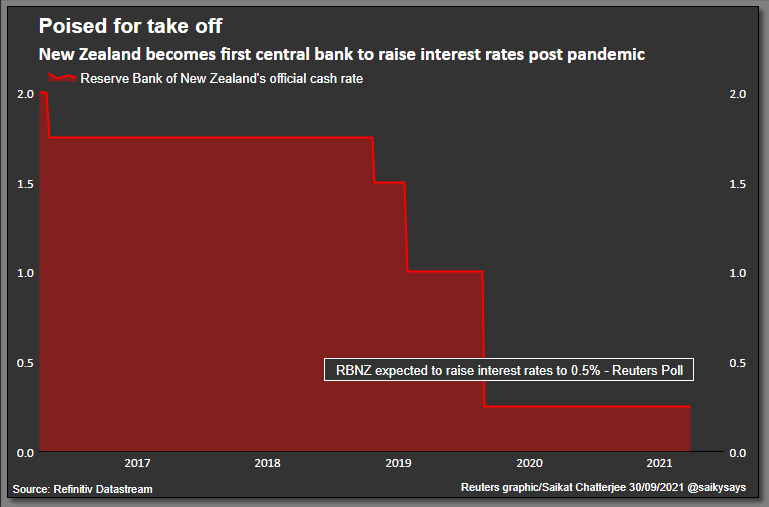

#2 Rates decision in Australia and NZ

Rates decisions are due in Australia and New Zealand - two countries separated geographically only by the Tasman Sea but worlds apart on monetary policy.

The Reserve Bank of New Zealand looks set to pull the trigger on Wednesday, with markets all but certain of a quarter point increase in the key rate to 0.5% RBNZWATCH. Governor Adrian Orr and crew were ready to become the first in the developed world to hike in August, but a COVID outbreak coinciding with the policy meeting scuppered those plans, leaving the Norges Bank to take the honours.

Australia's Reserve Bank meets on Tuesday and sits at the other end of the hawk-dove spectrum. Despite a red-hot housing market, Governor Philip Lowe threw cold water on markets recently, saying he found it "difficult to understand why rate rises are being priced in next year or early 2023."

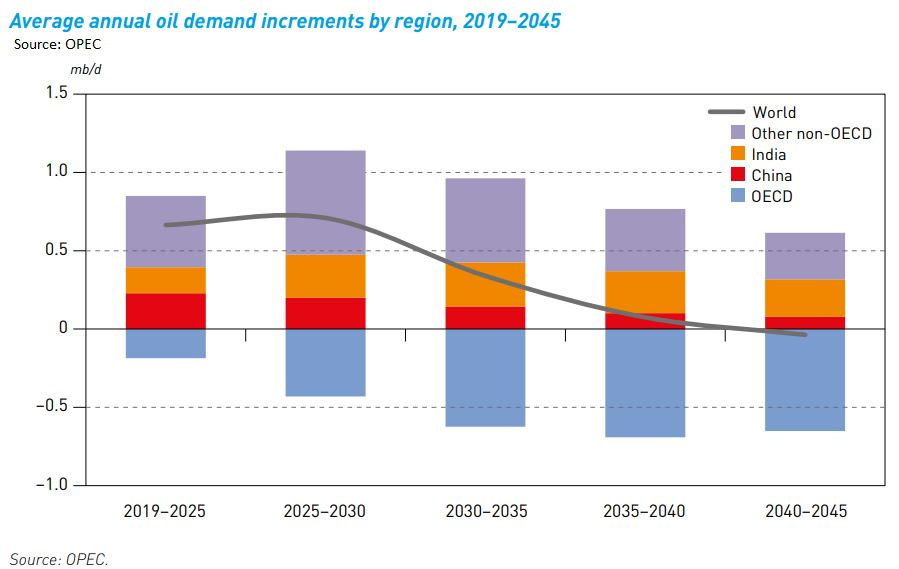

#3 OPEC + Decision

When ministers from OPEC+ - the Organization of Petroleum Exporting Countries and allies led by Russia - meet on Monday to review output policy they face oil prices at three-year highs above $80 a barrel and consumer pressure for more supply.

Until recently, sources expected the group to stick to the existing plan agreed in July and boost output by 400,000 barrels per day (bpd) a month to phase out 5.8 million bpd in cuts.

But with prices boosted by unplanned U.S. outages and a strong demand recovery after the pandemic, that thinking might be shifting: OPEC+ sources said adding more oil was being looked at as a scenario. The White House, which raised concerns about high prices, said it was in communication with OPEC and looking at how to address the cost of oil.

# 4 China difficulties

It's been quite a ride over the past three months: Chinese markets suffered some of their heaviest falls ever, energy prices spiralled, shipping and commodity costs soared and the clearest signs yet have emerged that central banks are starting to turn off the money taps. Analysts predict a bumpy ride ahead with markets pricing the end of the "Goldilocks" scenario - when growth and inflation are neither too high nor too low. Time for investors to be aware of the bears.

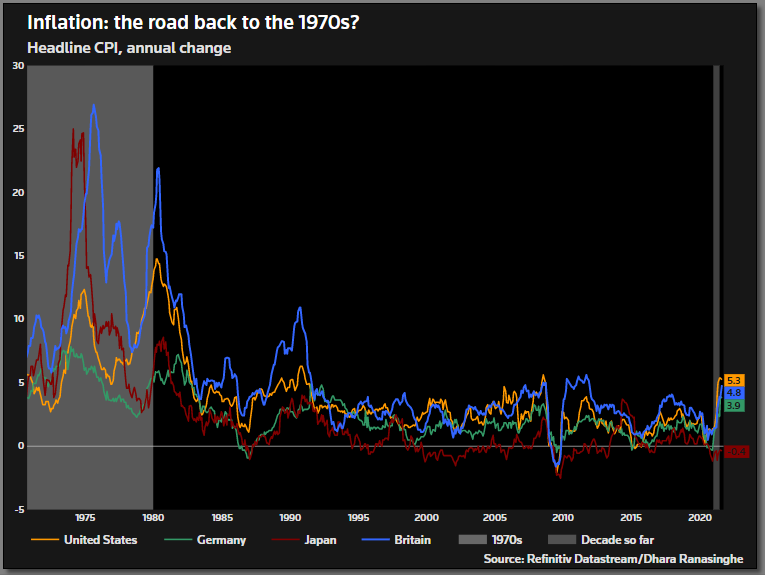

# 5 IMF on global inflation

Power cuts in China, queues at fuel pumps in Britain, soaring energy prices everywhere. Headlines resonate with the 1970s - and nowhere more so than in Britain, where the army will help to alleviate a fuel shortage that has led to gaps on supermarket shelves and fights at gas stations. The end of a COVID jobs support scheme means more uncertainty.

The International Monetary Fund's take on inflation on Wednesday could shed light on whether rampant price pressures akin to the 1970s are taking hold.

So, the euphoria around Fed policy and stronger dollar is becoming obvious. Investors are more and more become aimed on faster Fed reaction. Now we see that global trends are accelerated. The negative sentiment on stock market becomes stronger and US interest rates start rising faster than previously. With delivery and supply problems in many countries - China, EU, GB, it seems that global trend turn to motion. Technical picture also stands favorite to US Dollar and currently it is difficult to find the reasons to go against its strength, at least in long-term.

It seems that we could get only the bounce from strong support area on EUR, but hardly we could pretend on real reversal. Still, I have concern about long-term downside DXY target that has not been met - 87.4, big downside AB-CD on monthly/weekly time frame. What fundamental reasons could make market to reach it?

Whether it will be ignored by new upside trend, or it means that current bullish USD mood is temporal? Currently we do not have answers.

Technicals

Monthly

It is difficult to call September as positive month to EUR. Trend remains bearish and market shows two bearish signs right in single month - confirms downside pennant breakout. Second - forms bearish reversal month in September. Despite that we could get some bounce in October as we've discussed, it seems that bearish saga on EUR is not over yet and could get continuation in Nov-Dec as we come closer to the first hawkish Fed step.

Weekly

To consider possible short-term bounce it would be better to consider Dollar Index that now stands at major resistance area. Here we could recognize some harmony that let us to suggest H&S -looking price action. It means that market could show 50% bounce to form potential right arm. Based on the EUR chart it should be somewhere to 1.20-1.21 area.

It seems that this is the most positive scenario for the EUR. Conversely, the direct upside breakout could happen, although we treat this way as less probable because resistance is rather strong, including previous lows and all major events mostly priced-in already. Whatever NFP, inflation or GDP data we get - barely they change Fed view and expected decisions in November and December.

Daily

Since the support area rather wide and long term, we need to be patient to get the response. Hardly it happens within 1-2 sessions. Here is how approximately it could look like. Now market forms 1.27 extension down, with the possible following to 1.618 one. Both ratios are possible for H&S pattern. Thus, somewhere in the range between them we could keep an eye on intraday chart for bullish reversal patterns. This is first entry setup.

Speaking directly about daily chart - we need to get pattern here as well, and 2nd entry could be possible around right arm of 1.17 area, if EUR keeps the harmony and not break 1.19 resistance directly. Using the same harmony AB-CD pattern leads us precisely to 1.20 area resistance that agrees with DXY chart:

Intraday

Here we have nothing to discuss yet except this one - minor pattern. But it is definitely the one that we're watching for. It is too small. Yes it could trigger upward bounce on Monday, but something of the bigger scale has to be formed, even for intraday purposes. It is too few time spent since market hits the level. Besides UER could slide a bit lower to 1.618 daily extension before bulls turn to action. So, hopefully within 2-3 sessions, we get some hints.

This week we've got few important events and data. First is Dollar Index (and EUR) has hit long-term target and resistance area that let us hope to get some good trading setups within few weeks. Inflation pressure is rising and now accompanied with good numbers on consumption and personal spending that makes people more and more talk about Fed policy change sooner rather than later. Finally, the spike in EU inlfation that mostly was missed by wide market society seems important to us, because it perfectly fits to technical picture that suggest EUR upward bounce. We've discussed this spike in last report and suggest that Germany inflation could peak around 5% in next month. So, this should shake sleeping ECB a bit.

Market overview

The U.S. dollar advanced on Monday, bolstered by the rise in Treasury yields ahead of a slew of Federal Reserve speakers this week who could affirm expectations of the start of asset purchase reduction before the end of the year. U.S. benchmark 10-year Treasury yields hit a three-month high of $1.516%.

The greenback also extended gains after data showed new orders and shipments of key U.S.-made capital goods increased solidly in August, rising 0.5% in August amid strong demand for computers and electronic products.

But the market has been more focused on the U.S. Treasury market. U.S. yields climbed to their highest since late June in anticipation of tighter monetary policy after the Fed announced last week it may start tapering stimulus as soon as November and flagged interest rate increases may follow sooner than expected.

"As much as taper in and of itself is not a surprise, an earlier end to its program will reinforce that downside risks to the U.S. dollar have diminished," Mazen Issa, senior FX strategist at TD Securities, wrote in a research note. TD expects the Fed to end its quantitative easing program by June 2022. If the last taper cycle was any indication, about half of the U.S. dollar's cyclical upswing was observed three months after taper," he added.

The euro largely ignoring developments in German elections over the weekend, with the Social Democrats projected to narrowly defeat the CDU/CSU conservative bloc.

"The buck has no real reason to decline from where it is, so it will be about looking for what may actually change that as we hear from various sides this week: a new German leadership, a new Japanese head of state, and the U.S. Congress," said Juan Perez, FX strategist and trader at Tempus Inc in Washington.

"Yields are generally moving higher as rising inflation expectations weigh on the relative attractiveness of government bonds, but are climbing even faster in the United States as traders bet the Federal Reserve will move more quickly than its global counterparts," said Karl Schamotta, chief market strategist at Cambridge Global Payments in Toronto. Rate differentials are tilting toward the dollar, weakening low-yielders and putting pressure on economies with significant borrowing needs."

Risk aversion exacerbated the currency market moves, said Neil Jones, head of FX sales at Mizuho, with Wall Street shares down.

U.S. Treasury Secretary Janet Yellen, said on Tuesday that U.S. inflation at the end of the year would be closer to 4%, double the Fed target.

"One theme that seems to be gaining traction is that the market lies on the cusp of reassessing the path for the Fed tightening cycle," ING strategists wrote in a note to clients. A big move higher in the short-end is the key reason why we are bullish on the dollar, particularly from 2Q next year, but we will closely monitor and reassess whether that move needs to come earlier - largely a function of timing the take-off in short-end rates."

The dollar surged on Wednesday to a one-year high against major currencies, boosted by increased expectations for a reduction in the U.S. Federal Reserve's asset purchases starting in November and an interest rate hike, possibly in late 2022.

The greenback also fared well despite an impasse in Washington over the U.S. debt ceiling that threatened to plunge the government into a shutdown. The world's largest reserve currency, seen as a safe-haven bet at times of market stress, has strengthened in recent days as investors instead focused on fears of a global slowdown, a rise in energy prices and higher U.S. Treasury yields.

Traders are also concerned that the Fed will start to withdraw policy support just as global growth slows.

"Fed has sounded the starting gun on monetary policy normalization," Kit Juckes, macro strategist at Societe Generale, wrote in his latest research note. As the U.S. escapes the interest rate zero-bound, leaving the Eurozone and Japan behind, the global savings glut is set to be drawn towards the dollar, which can outperform the majority of other currencies in the coming year, and may start its move earlier than we expected," Juckes added.

Erik Nelson, macro strategist at Wells Fargo in New York, sees a further 2% to 3% upside in the dollar index.

The dollar began the last quarter of 2021 near its highest levels of the year and headed for its best week since June, as currency markets braced for U.S. interest rates to rise before those of major peers.

A Federal Reserve meeting last week reinforced expectations for asset purchase tapering beginning this year and rate hikes starting in 2022 or early in 2023.

"As long as markets remain confident that the U.S. is going to start tightening monetary policy within a reasonable timeframe, the dollar should remain well supported and eventually rise 5-10% from current levels," said Societe Generale strategist Kit Juckes. "The prospect of the European Central Bank keeping rates below zero while the Fed hikes should keep euro/dollar in the post-2014 range, with a centre of gravity around $1.12-1.16," he said.

Commodity currencies made a bounce on the dollar on Thursday following a Bloomberg report which said China had ordered energy companies to secure supplies for the winter at all costs, citing unnamed people familiar with the matter. Beijing is scrambling to deliver more coal to utilities to restore supply amid a power crunch that has unsettled markets due to the likely hit to economic growth.

“The reasons to suspect an energy supply crunch in China are more deeply rooted and largely boil down to China’s new policy aimed at reducing greenhouse emissions, which have put increasing curbs on domestic coal output,” said Francesco Pesole, G10 FX strategist at ING. “At the same time, a historic import route – the one with Australia – has recently come under pressure amid geopolitical and trade tensions between the two countries, which recently saw China impose duties on Australian coal. One way this is affecting the FX market is through the notion that the Chinese central bank is now welcoming a stronger yuan in an attempt to insulate the country against soaring commodity prices, Pesole said. It appears that markets have increasingly sunk their teeth into this narrative, and CNY’s resilience to the Evergrande saga looks like a testament to this.”

Cautious market sentiment due to COVID-19 concerns, wobbles in China’s growth and a Washington gridlock ahead of a looming deadline to lift the U.S. government’s borrowing limit also lent support to the dollar which is seen as a safe-haven asset.

“Last week’s Fed meeting added fresh life into the debate about a potential hike in the fed funds rate in 2022,” said Jane Foley, head of FX strategy at Rabobank. This is positive for the USD on two fronts. Firstly the USD looks better on a straightforward interest rate differential perspective. Secondly a hike in U.S. rates and a stronger USD will weigh on the growth outlook in EM. The growth outlook for emerging markets is already suffering on concerns of a slowdown in China and on fears of an energy crunch, Foley said. The result is that the USD benefits from a drop in risk appetite and flows out of higher risk EM markets.”

Benchmark 10-year Treasury yields are up for a sixth straight week and real 10-year yields, discounted for inflation, are rising far more quickly than counterparts in Europe.

U.S. consumer spending surged in August, but outlays adjusted for inflation were weaker than initially thought in the prior month, reinforcing expectations that economic growth slowed in the third quarter as COVID-19 infections flared up. Consumer spending, which accounts for more than two-thirds of U.S. economic activity, rebounded 0.8% in August. Data for July was revised down to show spending dipping 0.1% instead of gaining 0.3% as previously reported.

Inflation maintained its upward trend in August, though price pressures have probably peaked. The personal consumption expenditures (PCE) price index, excluding the volatile food and energy components, climbed 0.3% after increasing by the same margin in July. In the 12 months through August, the so-called core PCE price index increased 3.6%, matching July's gain.

The core PCE price index is the Federal Reserve's preferred inflation measure for its flexible 2% target. The U.S. central bank last week upgraded its core PCE inflation projection for this year to 3.7% from 3.0% back in June.

Inflation could remain high for a while. A survey from the Institute for Supply Management on Friday showed manufacturers experienced longer delays getting raw materials delivered to factories and paid higher prices for inputs in September.

High inflation is cutting into spending. Real consumer spending rose 0.4% in August following a downwardly revised 0.5% drop in July. With the August and July data in hand, economists predicted that growth in consumer spending would probably brake to around a 1% annualized rate in the third quarter.

The Atlanta Fed cut its GDP estimate for the quarter to a 2.3% rate from a 3.2% pace. Slower growth was reinforced by a third report from the Commerce Department showing construction spending flat in August.

"Even with the softening growth picture, we continue to expect the Fed to announce the start of tapering at the early November meeting," said Michael Feroli, chief U.S. economist at JPMorgan in New York.

The economy remains supported by record corporate profits. Households accumulated at least $2.5 trillion in excess savings during the pandemic. Coronavirus infections are trending down, which is already leading to a rise in demand for travel and other high-contact services. Businesses need to replenish depleted inventories, which will keep factories humming.

U.S. manufacturing activity picked up further in September, but factories experienced longer delays getting raw materials delivered and paid higher prices for inputs.

The Institute for Supply Management (ISM) said on Friday its index of national factory activity increased to a reading of 61.1 last month from 59.9 in August.

Euro zone and British manufacturing growth remained strong but activity suffered from logistical issues, product shortages and a labour crunch that are likely to persist and keep inflationary pressures high. IHS Markit's final manufacturing Purchasing Managers' Index (PMI) sank to 58.6 in September from August's 61.4 and Britain's PMI fell for a fourth month in a row, dropping to 57.1 from 60.3.

Inflation in the common currency area jumped to a 13-year high of 3.4% last month, preliminary official data showed on Friday, well above the European Central Bank's 2.0% target.

"We think there are high chances that this inflation is less transitory than all central banks, including the ECB, are suggesting," BNP Paribas economist Luigi Speranza said. Consumers may start demanding higher wages and corporations may accommodate them, on the basis they could pass on higher cost via higher final prices."

Core inflation excluding food and energy rose to 1.9% from 1.6%, as did a narrower measure that also excludes alcohol and tobacco.

A grinding rally in the dollar is picking up speed, fueled by a hawkish tilt from the Federal Reserve, rising Treasury yields and concerns over the possibility of a drawn-out battle to raise the U.S. debt ceiling.

The greenback is up 4.7% year-to-date and stands near its highest level in a year against a basket of currencies. Net bets on the dollar in futures markets are at a more than 18-month high, according to data from the CFTC.

"The U.S. dollar move we're seeing at present is due to a confluence of factors that are all aligning to create the perfect storm," said Simon Harvey, senior FX market analyst at Monex Europe in London.

Yields on 10-year United States Treasury Inflation Protected Securities , which strip out inflation, have risen by about 37 basis points since early August, compared with a gain of only 5 basis points for its German counterpart. That has increased the attractiveness of dollar-denominated Treasuries compared with their foreign counterparts.

"It seems the consensus view that (the) Fed taper was in the price of the dollar was incorrect," said Richard Benson, co-chief investment officer, at Millennium Global in London. "We've had a 20-30 basis-point backup in yields which has supported the dollar."

COT Report

We do not see yet how results of this week impact the net position, but I dare to suggest that hardly it is very positive to EUR. Meantime, last week performance has negative impact on EUR net position. It has dropped, keeping downside trend that is started in June of last year.

COT data shows that net short position has increased this week as traders have opened more short positions. Open interest has increased for 10K. That combination suggests that overall sentiment stands moderately bearish for EUR.

Next week to watch

#1 US NFP Data

In September, the U.S. Fed said trimming monthly bond purchases could be warranted "soon"; Chair Jerome Powell noted it'll take one more "decent" jobs report to set the wheels in motion - not a "super-strong" one, just one that's "reasonably good". Will Friday's September nonfarm numbers - the last official jobs report before the Fed's November meeting - do the trick?

A Reuters poll expects 500,000 jobs were added after August's massive miss. Stronger-than-expected numbers might fuel fears the Fed could wind down easy-money policies faster than anticipated, potentially causing more market turbulence.

#2 Rates decision in Australia and NZ

Rates decisions are due in Australia and New Zealand - two countries separated geographically only by the Tasman Sea but worlds apart on monetary policy.

The Reserve Bank of New Zealand looks set to pull the trigger on Wednesday, with markets all but certain of a quarter point increase in the key rate to 0.5% RBNZWATCH. Governor Adrian Orr and crew were ready to become the first in the developed world to hike in August, but a COVID outbreak coinciding with the policy meeting scuppered those plans, leaving the Norges Bank to take the honours.

Australia's Reserve Bank meets on Tuesday and sits at the other end of the hawk-dove spectrum. Despite a red-hot housing market, Governor Philip Lowe threw cold water on markets recently, saying he found it "difficult to understand why rate rises are being priced in next year or early 2023."

#3 OPEC + Decision

When ministers from OPEC+ - the Organization of Petroleum Exporting Countries and allies led by Russia - meet on Monday to review output policy they face oil prices at three-year highs above $80 a barrel and consumer pressure for more supply.

Until recently, sources expected the group to stick to the existing plan agreed in July and boost output by 400,000 barrels per day (bpd) a month to phase out 5.8 million bpd in cuts.

But with prices boosted by unplanned U.S. outages and a strong demand recovery after the pandemic, that thinking might be shifting: OPEC+ sources said adding more oil was being looked at as a scenario. The White House, which raised concerns about high prices, said it was in communication with OPEC and looking at how to address the cost of oil.

# 4 China difficulties

It's been quite a ride over the past three months: Chinese markets suffered some of their heaviest falls ever, energy prices spiralled, shipping and commodity costs soared and the clearest signs yet have emerged that central banks are starting to turn off the money taps. Analysts predict a bumpy ride ahead with markets pricing the end of the "Goldilocks" scenario - when growth and inflation are neither too high nor too low. Time for investors to be aware of the bears.

# 5 IMF on global inflation

Power cuts in China, queues at fuel pumps in Britain, soaring energy prices everywhere. Headlines resonate with the 1970s - and nowhere more so than in Britain, where the army will help to alleviate a fuel shortage that has led to gaps on supermarket shelves and fights at gas stations. The end of a COVID jobs support scheme means more uncertainty.

The International Monetary Fund's take on inflation on Wednesday could shed light on whether rampant price pressures akin to the 1970s are taking hold.

So, the euphoria around Fed policy and stronger dollar is becoming obvious. Investors are more and more become aimed on faster Fed reaction. Now we see that global trends are accelerated. The negative sentiment on stock market becomes stronger and US interest rates start rising faster than previously. With delivery and supply problems in many countries - China, EU, GB, it seems that global trend turn to motion. Technical picture also stands favorite to US Dollar and currently it is difficult to find the reasons to go against its strength, at least in long-term.

It seems that we could get only the bounce from strong support area on EUR, but hardly we could pretend on real reversal. Still, I have concern about long-term downside DXY target that has not been met - 87.4, big downside AB-CD on monthly/weekly time frame. What fundamental reasons could make market to reach it?

Whether it will be ignored by new upside trend, or it means that current bullish USD mood is temporal? Currently we do not have answers.

Technicals

Monthly

It is difficult to call September as positive month to EUR. Trend remains bearish and market shows two bearish signs right in single month - confirms downside pennant breakout. Second - forms bearish reversal month in September. Despite that we could get some bounce in October as we've discussed, it seems that bearish saga on EUR is not over yet and could get continuation in Nov-Dec as we come closer to the first hawkish Fed step.

Weekly

To consider possible short-term bounce it would be better to consider Dollar Index that now stands at major resistance area. Here we could recognize some harmony that let us to suggest H&S -looking price action. It means that market could show 50% bounce to form potential right arm. Based on the EUR chart it should be somewhere to 1.20-1.21 area.

It seems that this is the most positive scenario for the EUR. Conversely, the direct upside breakout could happen, although we treat this way as less probable because resistance is rather strong, including previous lows and all major events mostly priced-in already. Whatever NFP, inflation or GDP data we get - barely they change Fed view and expected decisions in November and December.

Daily

Since the support area rather wide and long term, we need to be patient to get the response. Hardly it happens within 1-2 sessions. Here is how approximately it could look like. Now market forms 1.27 extension down, with the possible following to 1.618 one. Both ratios are possible for H&S pattern. Thus, somewhere in the range between them we could keep an eye on intraday chart for bullish reversal patterns. This is first entry setup.

Speaking directly about daily chart - we need to get pattern here as well, and 2nd entry could be possible around right arm of 1.17 area, if EUR keeps the harmony and not break 1.19 resistance directly. Using the same harmony AB-CD pattern leads us precisely to 1.20 area resistance that agrees with DXY chart:

Intraday

Here we have nothing to discuss yet except this one - minor pattern. But it is definitely the one that we're watching for. It is too small. Yes it could trigger upward bounce on Monday, but something of the bigger scale has to be formed, even for intraday purposes. It is too few time spent since market hits the level. Besides UER could slide a bit lower to 1.618 daily extension before bulls turn to action. So, hopefully within 2-3 sessions, we get some hints.

Last edited: