tickmill-news

Tickmill Representative

- Messages

- 79

Bearish ECB signal sets the stage for further EURUSD decline, 1.05 level in sight

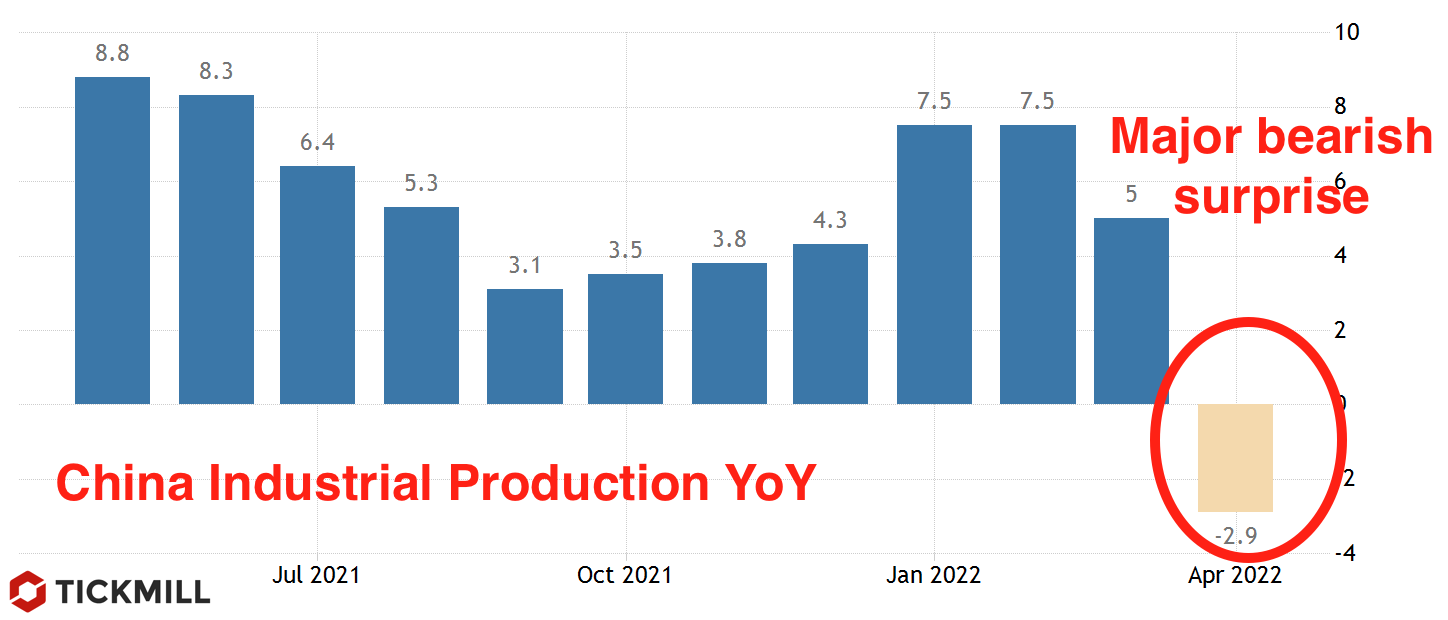

Costly in terms of economic costs, the policy of “zero covid cases” forced the Chinese Central Bank to cut reserve ratio for banks by 25 bp on Monday. According to the PBOC, this should boost liquidity in the banking sector by 530 billion yuan which should in turn stimulate lending. The easing measures taken by the PBOC send a warning signal to global asset markets about potential setback in China growth in 2Q. Data on the Chinese economy for 1Q came out better than expected, except for retail sales, which plunged in March by 3.5% YoY, more than twice as much as expected. Unemployment rose from 5.5% to 5.8%.

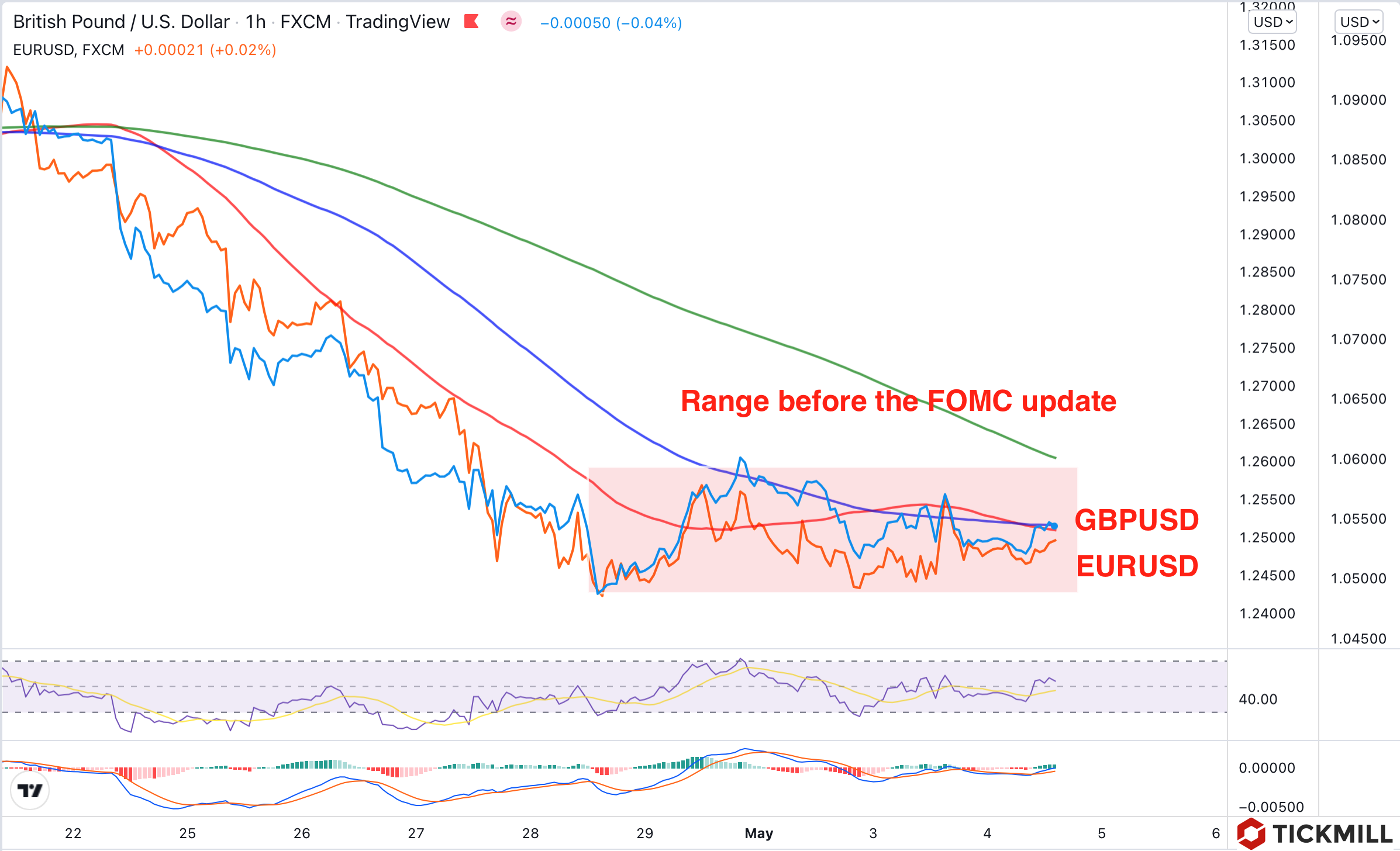

EURUSD struggles to recover after collapse on last Thursday below the previous local low, to 1.0750:

The catalyst for selling was the ECB meeting, in particular Lagarde's downbeat comments, which showed a high level of concern about macroeconomic stability. Together with very modest initiatives to use monetary tools to combat the blow from inflation, the ECB basically acknowledged that there is little it can do in the current juncture. Lagarde said that the downside risks to the economy rose substantially and inflation became broader (dimming hopes that inflation will subside as oil prices pull back). The eagerness of the ECB to respond was quite disappointing - according to Lagarde, quantitative tightening (selling bonds from the balance sheet) is not yet discussed, and QE will end only in the third quarter. Bloomberg, citing its sources, reports that ECB policymakers “still see it as possible” to raise interest rate in July, that is, the baseline scenario is that there will be no rate increase at the next meeting, the first increase is expected to happen only after the end of APP, i.e., in the 4Q of this year.

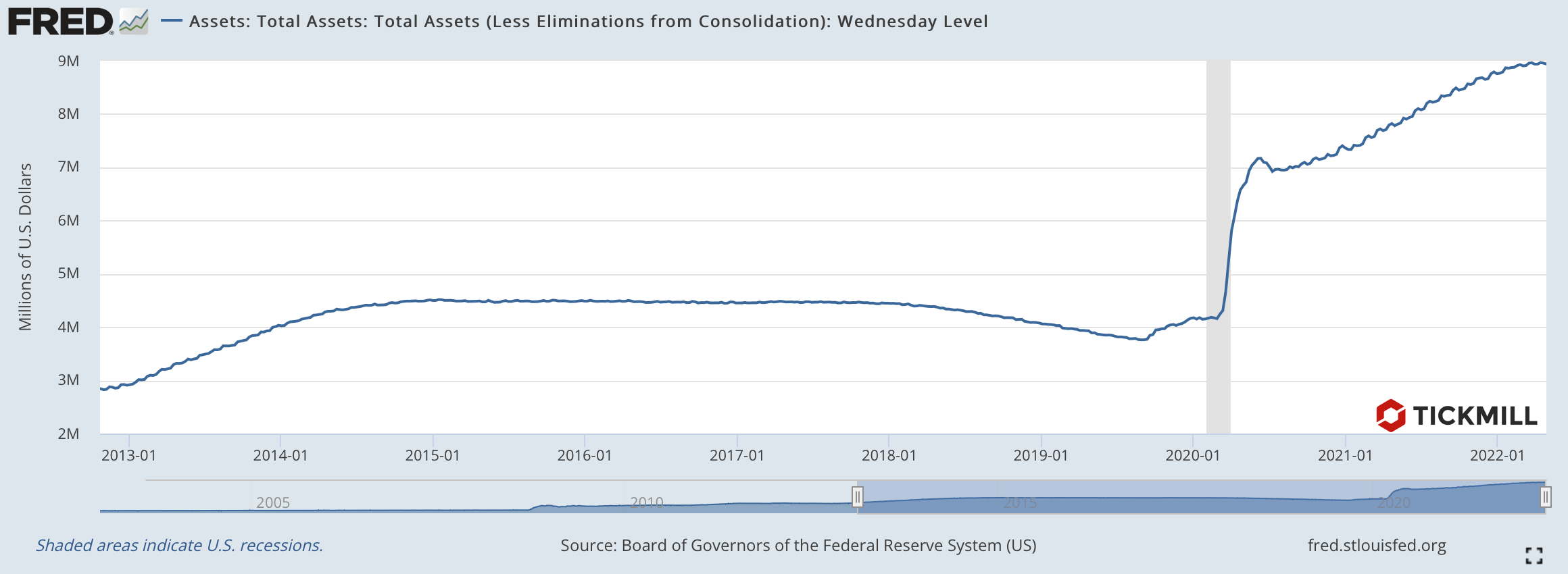

The contrast between the policy stances of the ECB and the Fed reveals more and more nuances that speak in favor of a weaker Euro. The Fed pledged not only to raise rates at a high pace, but also hinted that balance sheet runoff may begin as early as July. The ECB is not only not going to catch up, but also hints that the pace of tightening may slow down due to "significant risks" to growth. In this regard, the risks for EURUSD, in my opinion, are skewed towards further decline.

From the viewpoint of technical analysis, a rebound in EURUSD within the current downtrend can be expected at 1.0650 (March 2020 low), a reversal - in the range of 1.045 - 1.05:

In one of the previous articles, I discussed new local highs for the dollar and gold. Now we see the dollar index has broken through 100.50, and gold has approached $2000. I do not think that this is the limit, primarily because hopes for a peaceful resolution of the conflict in Ukraine are fading before our eyes, and the rhetoric is increasingly concentrated around the scenario of a protracted confrontation. All this promises a long period of high inflation coupled with low output rate. In this economic regime, the dollar and gold are usually seen as one of the best instruments for hedging.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Costly in terms of economic costs, the policy of “zero covid cases” forced the Chinese Central Bank to cut reserve ratio for banks by 25 bp on Monday. According to the PBOC, this should boost liquidity in the banking sector by 530 billion yuan which should in turn stimulate lending. The easing measures taken by the PBOC send a warning signal to global asset markets about potential setback in China growth in 2Q. Data on the Chinese economy for 1Q came out better than expected, except for retail sales, which plunged in March by 3.5% YoY, more than twice as much as expected. Unemployment rose from 5.5% to 5.8%.

EURUSD struggles to recover after collapse on last Thursday below the previous local low, to 1.0750:

The catalyst for selling was the ECB meeting, in particular Lagarde's downbeat comments, which showed a high level of concern about macroeconomic stability. Together with very modest initiatives to use monetary tools to combat the blow from inflation, the ECB basically acknowledged that there is little it can do in the current juncture. Lagarde said that the downside risks to the economy rose substantially and inflation became broader (dimming hopes that inflation will subside as oil prices pull back). The eagerness of the ECB to respond was quite disappointing - according to Lagarde, quantitative tightening (selling bonds from the balance sheet) is not yet discussed, and QE will end only in the third quarter. Bloomberg, citing its sources, reports that ECB policymakers “still see it as possible” to raise interest rate in July, that is, the baseline scenario is that there will be no rate increase at the next meeting, the first increase is expected to happen only after the end of APP, i.e., in the 4Q of this year.

The contrast between the policy stances of the ECB and the Fed reveals more and more nuances that speak in favor of a weaker Euro. The Fed pledged not only to raise rates at a high pace, but also hinted that balance sheet runoff may begin as early as July. The ECB is not only not going to catch up, but also hints that the pace of tightening may slow down due to "significant risks" to growth. In this regard, the risks for EURUSD, in my opinion, are skewed towards further decline.

From the viewpoint of technical analysis, a rebound in EURUSD within the current downtrend can be expected at 1.0650 (March 2020 low), a reversal - in the range of 1.045 - 1.05:

In one of the previous articles, I discussed new local highs for the dollar and gold. Now we see the dollar index has broken through 100.50, and gold has approached $2000. I do not think that this is the limit, primarily because hopes for a peaceful resolution of the conflict in Ukraine are fading before our eyes, and the rhetoric is increasingly concentrated around the scenario of a protracted confrontation. All this promises a long period of high inflation coupled with low output rate. In this economic regime, the dollar and gold are usually seen as one of the best instruments for hedging.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.