tickmill-news

Tickmill Representative

- Messages

- 79

Three key factors of short-term support of the Dollar

Foreign trade indices of major energy importers continue to hit new lows and markets are increasingly focused on how governments will respond to rising natural gas prices. At the same time, the weakening of the yuan and a number of potential upside surprises for the US economy today decrease the odds of a bearish dollar correction after the rally.

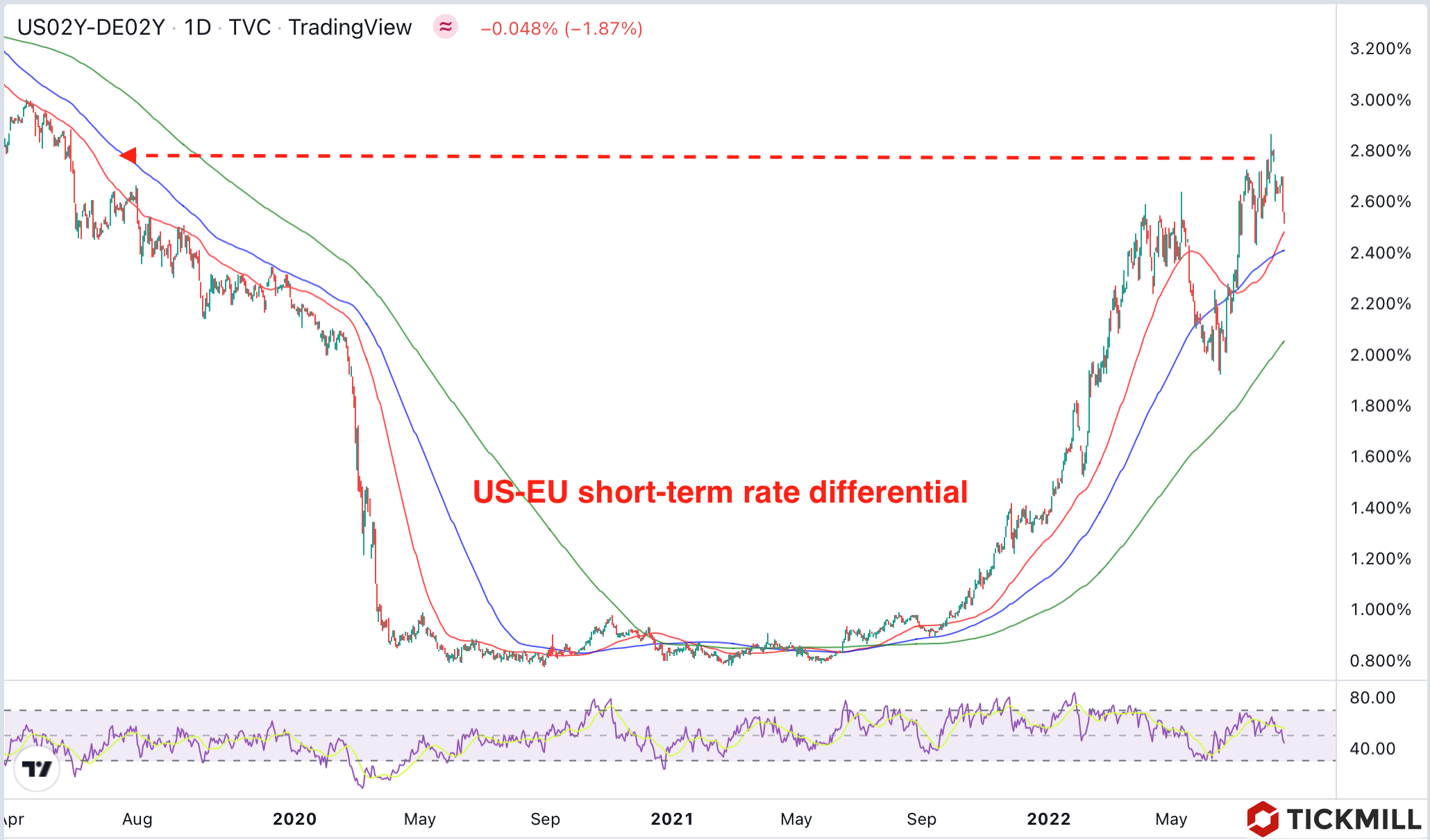

There are now three factors of short-term support for the dollar. The first factor is the supply shock on the gas market, which drove up gas prices, due to which large importers (EU, Asian countries) are faced with a situation where import price increases significantly outpace export price growth, which is a negative income shock. Governments are expected to take measures to mitigate the blow to the economy and what they offer will impact growth outlook, and hence real yield outlook offered by domestic assets. In turn, these expectations will form the demand for national currencies. So far, there are no tangible support measures, so currencies such as the Euro, Pound Sterling and the Yen are again under serious pressure. The US economy is relatively insulated from a gas supply shock by being less dependent on external energy supplies, which is factored into additional demand for the US dollar.

The second factor is a signal from the Chinese Central Bank that the economy needs a weak yuan to stimulate the movement of the economy towards its goals. PBOC cut the medium-term lending rate by 10 bp, which was a signal for USDCNY buying. In a few days, the price added about 1% approaching 6.80 and now the attention is on whether the Central Bank will further weaken the reference rate:

Earlier in April, when USDCNY surged 6%, the dollar rose against a basket of major currencies by about the same amount as well, suggesting that the situation with monetary stimulus in China will also act as a support factor for the dollar.

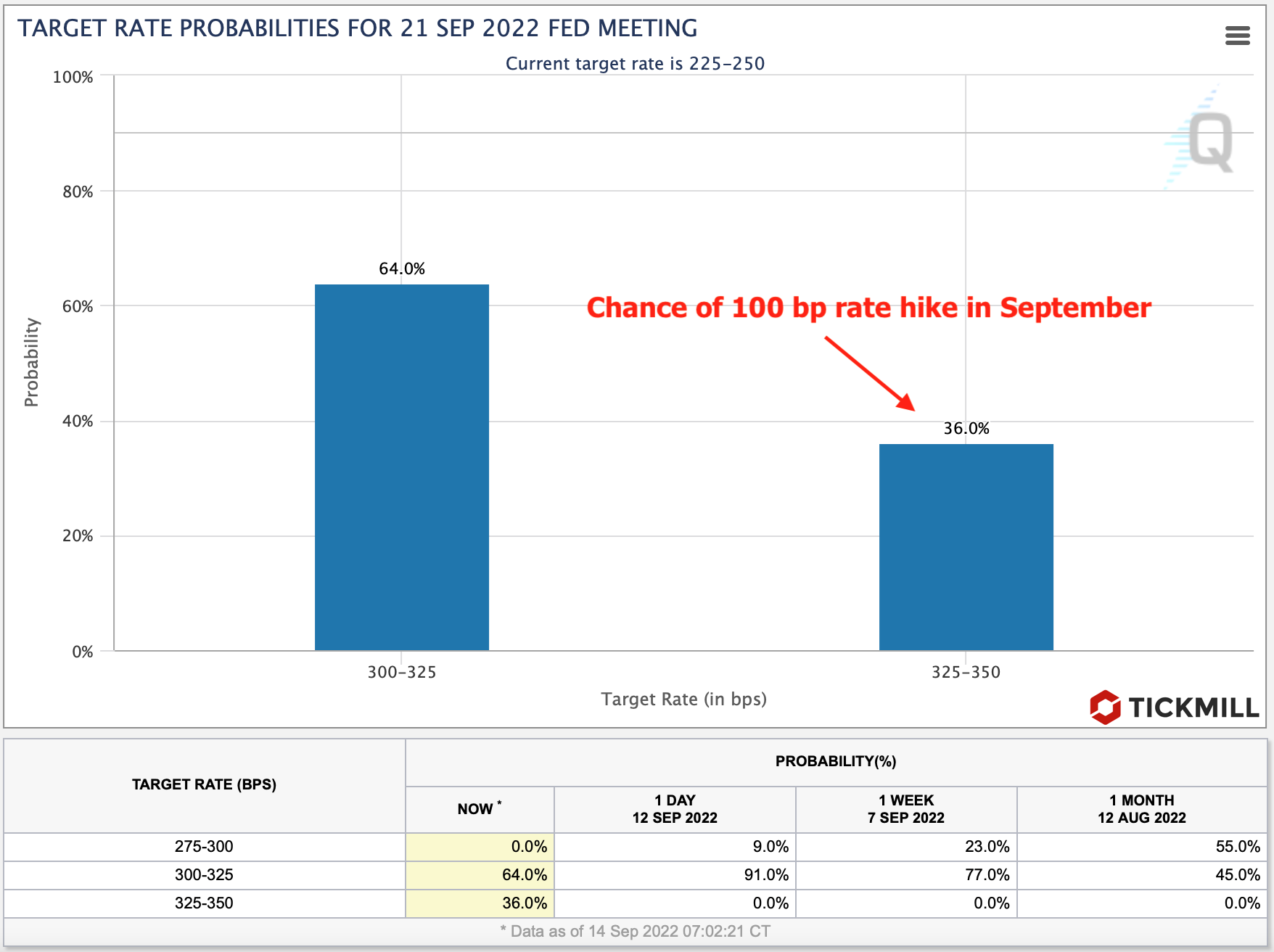

Data on the US economy, which has been surprising on the upside in August, may also be an argument in favor of a strong dollar. Today and tomorrow the reports are due on industrial production and retail sales. Given that the sharp drop in gasoline prices is a positive shock to both supply and demand (lower costs, more consumer spending power), the risks on these two reports are skewed towards a positive surprise. The Fed will put out the Minutes of the last FOMC meeting, given hawkish FOMC members’ bias, despite favorable signals in inflation, a hawkish surprise tomorrow cannot be ruled out.

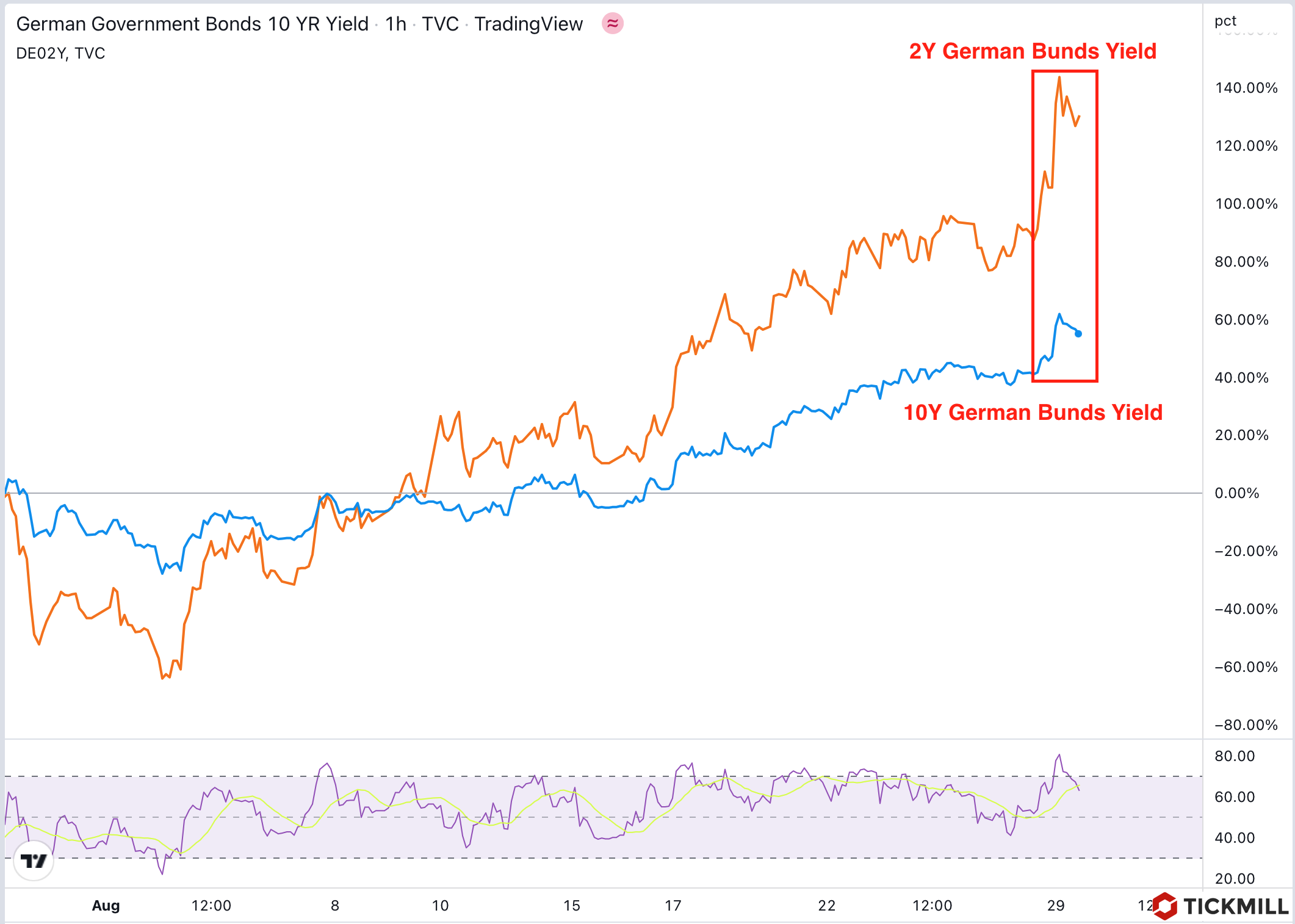

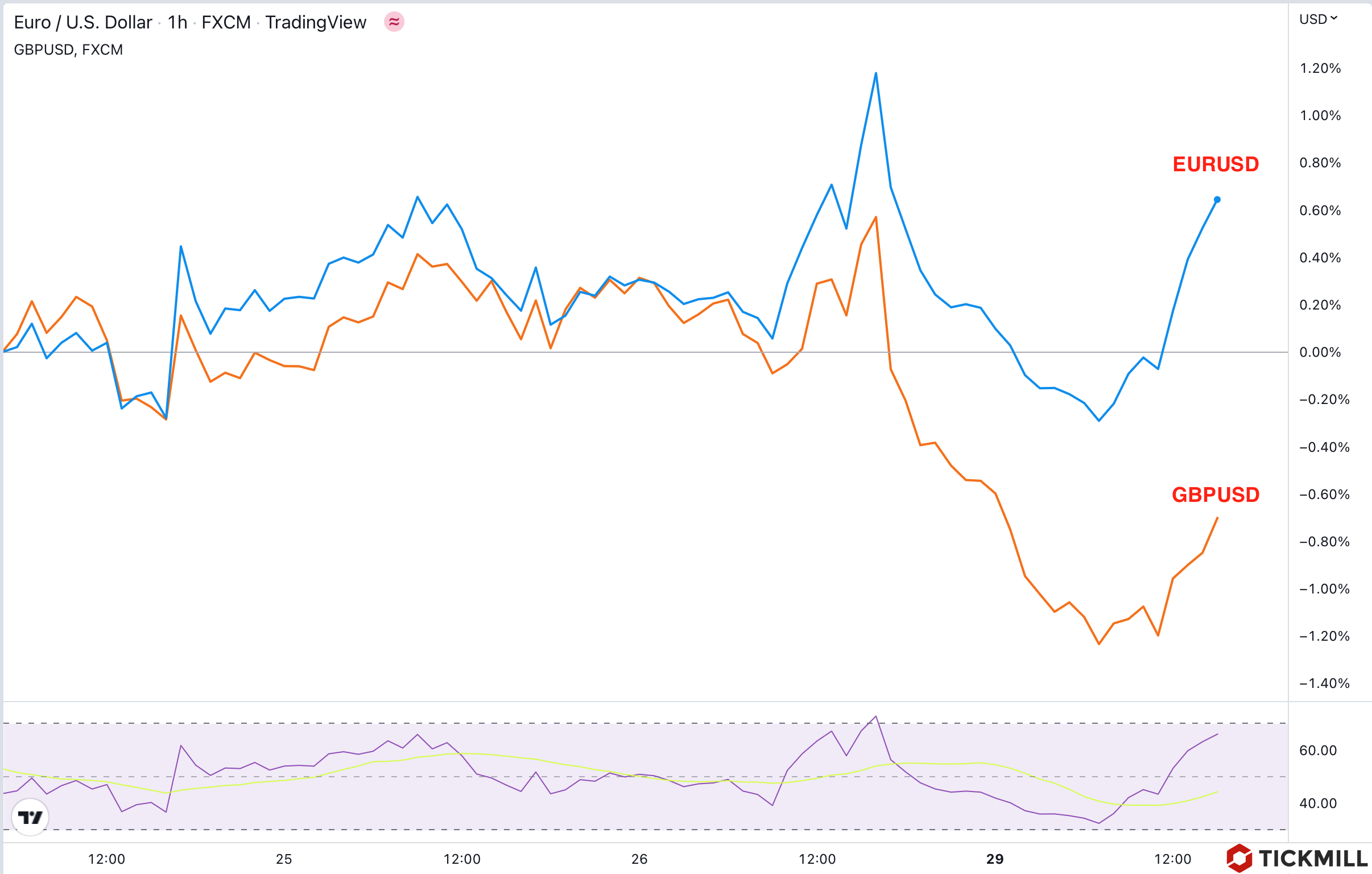

The news that the German government is imposing a gas levy suggests that the government doesn’t have enough means to smooth out the shock and also that inflation may be more persistent. In turn, this may require more tightening by the ECB, however raising rates in a period of fragile growth creates the risk of an accelerated slowdown in the economy. EURUSD is likely to retest 1.00 given the failed upside breakout of the medium-term bearish channel and subsequent downside breakout of the key short-term uptrend line that guided EURUSD recovery after the parity test, indicating that the next support should be expected at the level of 1.00:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Foreign trade indices of major energy importers continue to hit new lows and markets are increasingly focused on how governments will respond to rising natural gas prices. At the same time, the weakening of the yuan and a number of potential upside surprises for the US economy today decrease the odds of a bearish dollar correction after the rally.

There are now three factors of short-term support for the dollar. The first factor is the supply shock on the gas market, which drove up gas prices, due to which large importers (EU, Asian countries) are faced with a situation where import price increases significantly outpace export price growth, which is a negative income shock. Governments are expected to take measures to mitigate the blow to the economy and what they offer will impact growth outlook, and hence real yield outlook offered by domestic assets. In turn, these expectations will form the demand for national currencies. So far, there are no tangible support measures, so currencies such as the Euro, Pound Sterling and the Yen are again under serious pressure. The US economy is relatively insulated from a gas supply shock by being less dependent on external energy supplies, which is factored into additional demand for the US dollar.

The second factor is a signal from the Chinese Central Bank that the economy needs a weak yuan to stimulate the movement of the economy towards its goals. PBOC cut the medium-term lending rate by 10 bp, which was a signal for USDCNY buying. In a few days, the price added about 1% approaching 6.80 and now the attention is on whether the Central Bank will further weaken the reference rate:

Earlier in April, when USDCNY surged 6%, the dollar rose against a basket of major currencies by about the same amount as well, suggesting that the situation with monetary stimulus in China will also act as a support factor for the dollar.

Data on the US economy, which has been surprising on the upside in August, may also be an argument in favor of a strong dollar. Today and tomorrow the reports are due on industrial production and retail sales. Given that the sharp drop in gasoline prices is a positive shock to both supply and demand (lower costs, more consumer spending power), the risks on these two reports are skewed towards a positive surprise. The Fed will put out the Minutes of the last FOMC meeting, given hawkish FOMC members’ bias, despite favorable signals in inflation, a hawkish surprise tomorrow cannot be ruled out.

The news that the German government is imposing a gas levy suggests that the government doesn’t have enough means to smooth out the shock and also that inflation may be more persistent. In turn, this may require more tightening by the ECB, however raising rates in a period of fragile growth creates the risk of an accelerated slowdown in the economy. EURUSD is likely to retest 1.00 given the failed upside breakout of the medium-term bearish channel and subsequent downside breakout of the key short-term uptrend line that guided EURUSD recovery after the parity test, indicating that the next support should be expected at the level of 1.00:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.