IvanGlobalPrime

Company Representative

- Messages

- 36

Find my latest market thoughts

Yen Crosses Plummet As Risk-Off Returns

The recovery in risk appetite has been rather ephemeral, with the circuit breaker via Central Banks' easing (Fed, RBA, BOC) no having the desired effects to contain the fears of the coronavirus quickly evolving into a global pandemic. The disregard towards the macro-policy stimulus is an admission by Mr. Market of the limited effects this is going to have on a pick up in economic activity. As a result, the behavior of the markets remain reminiscent of an acceptance that a global recession is a forgone conclusion. Amid this backdrop, funding currencies rule.

The Daily Edge is authored by Ivan Delgado, 10y Forex Trader veteran & Market Insights Commentator at Global Prime. Feel free to follow Ivan on Twitter & Youtube weekly show. You can also subscribe to the mailing list to receive Ivan’s Daily wrap. The purpose of this content is to provide an assessment of the conditions, taking an in-depth look of market dynamics - fundamentals and technicals - determine daily biases and assist one’s trading decisions.

Let’s get started…

Quick Take

So far, the easing measures by the Fed, RBA and BOC have provided a very limited relief rally to the underlying risk-off dynamics, with the funding currencies’ complex still the place to be. Even the added groovy vibes via the major boost of Biden winning the Democration nomination have lasted barely 24h, with the market psyche still deeply rooted towards the COVID-19 as the big macro theme of 2020 as fears of widespread community transmissions in the US mount. As the day went on, risk trades softened and this led to Yen buying, while the Swiss Franc and the Euro followed in lockstep, although the buying flows were not as strong.

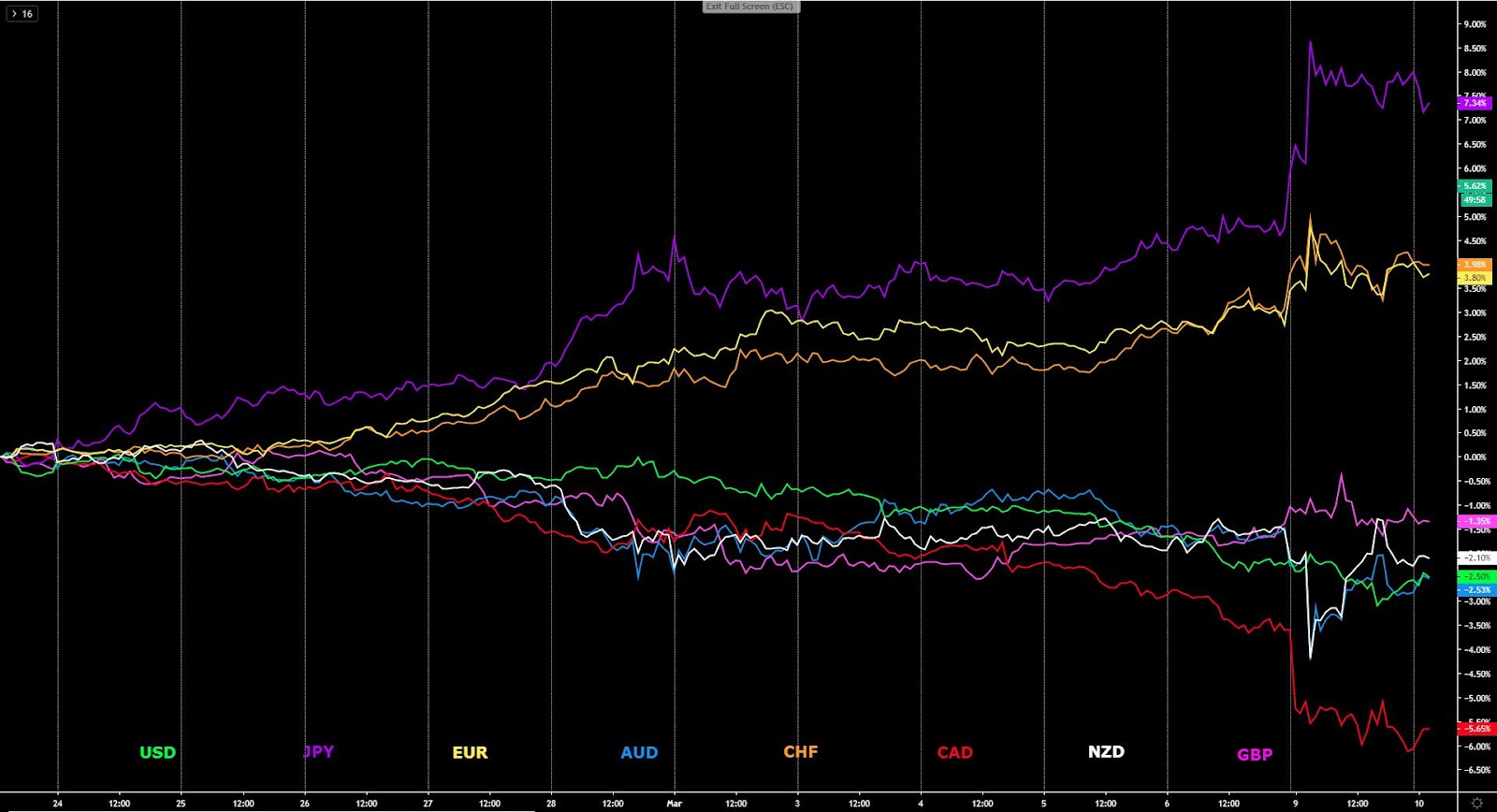

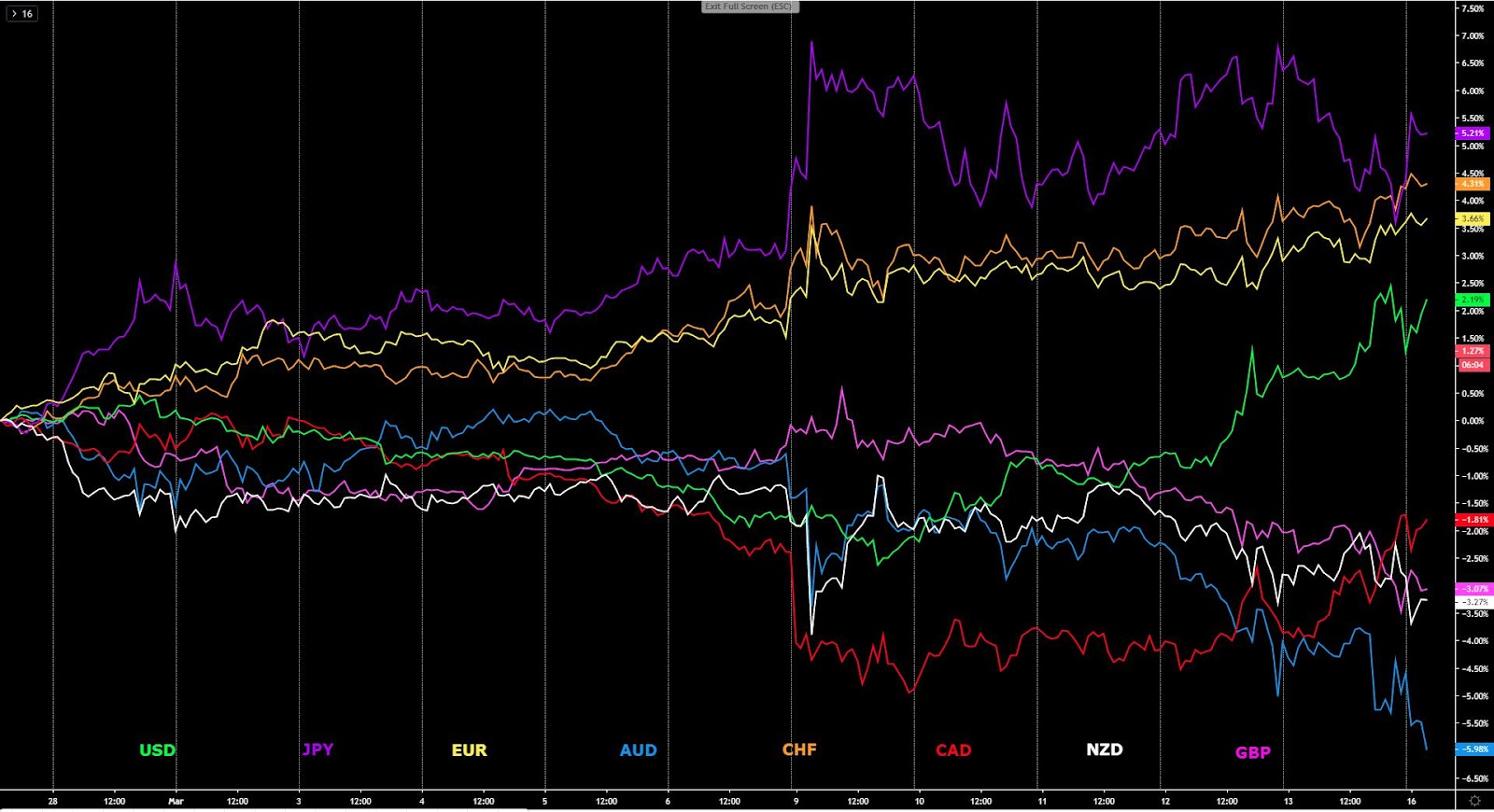

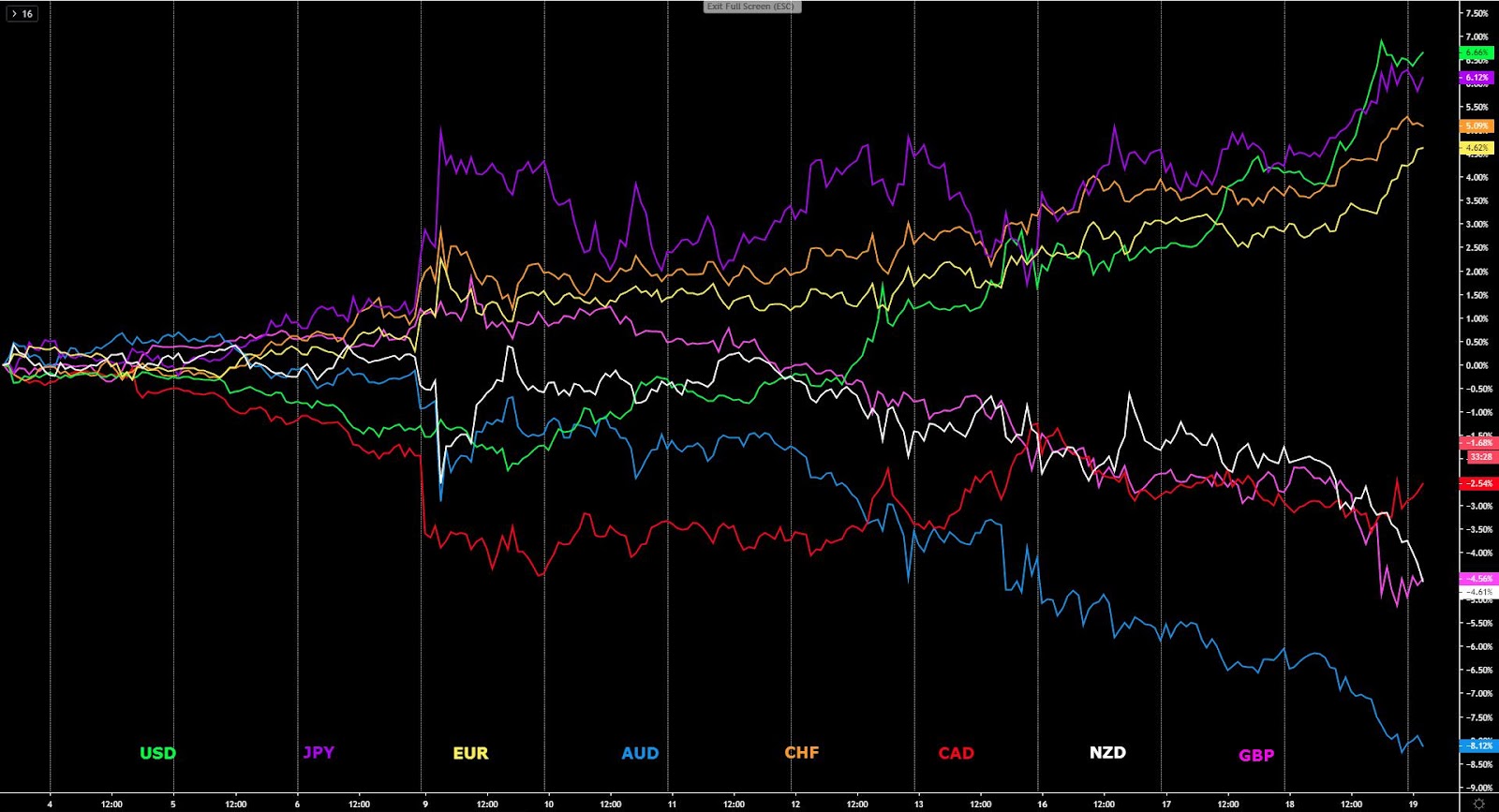

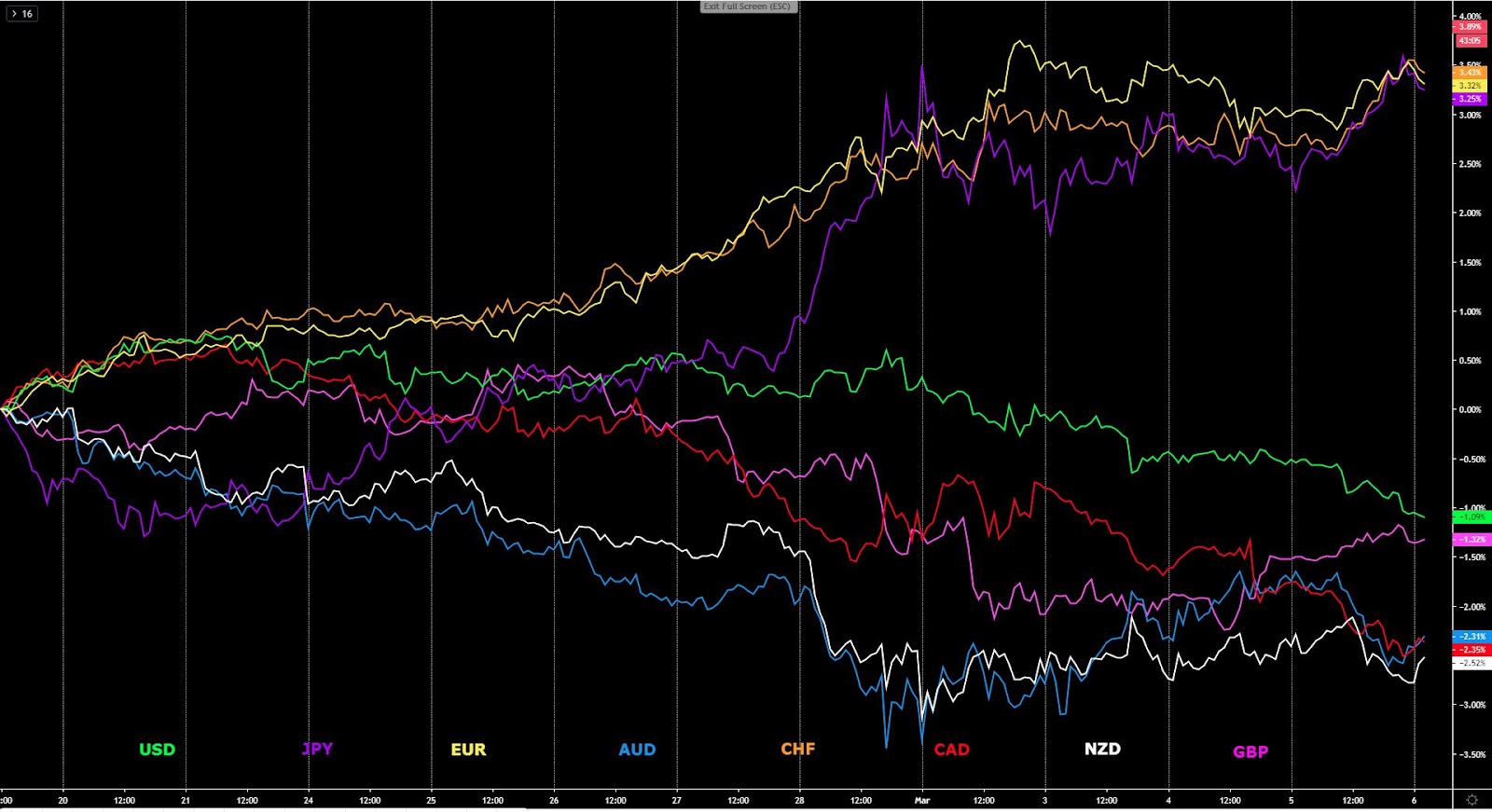

The G8 FX indices below illustrates the massive gap that has opened up as a result of the unwind of carry trades with hedges/margin calls favoring funding currencies amid a sky-high VIX. The snowball effect of bailing out carry trade long structures is the decay of the USD & CAD attractiveness, with the aggressive reduction in rates this week fueling the supply flows. The dicey environment created by the COVID-19 impact on world-wide economies is keeping the outlook for the Aussie and New Zealand Dollar very negative as the race to the bottom by the RBA/RBNZ is on as the market is now fixated on RBA’s QE measures later this year.

Amid such huge uncertainty for the global economy this year, the perky Pound has been gaining ground quietly, even if the negative backdrop of tough trade talks between the EU and the UK, coupled with a BOE that may follow the same path of other Central Banks, threatens the sustainability of this run. All in all, the trend this week has been well defined, with funding currencies the safest bets while carry long currencies (USD, CAD) and Oceanic (AUD, NZD) are suffering.

The indices show the performance of a particular currency vs G8 FX. An educational video on how to interpret these indices can be found in the Global Prime's Research section.

If you found the content in this section valuable, give us a share by just clicking here!

Narratives In Financial Markets

* The Information is gathered after scanning top publications including the FT, WSJ, Reuters, Bloomberg, ForexLive, Twitter, Institutional Bank Research reports.

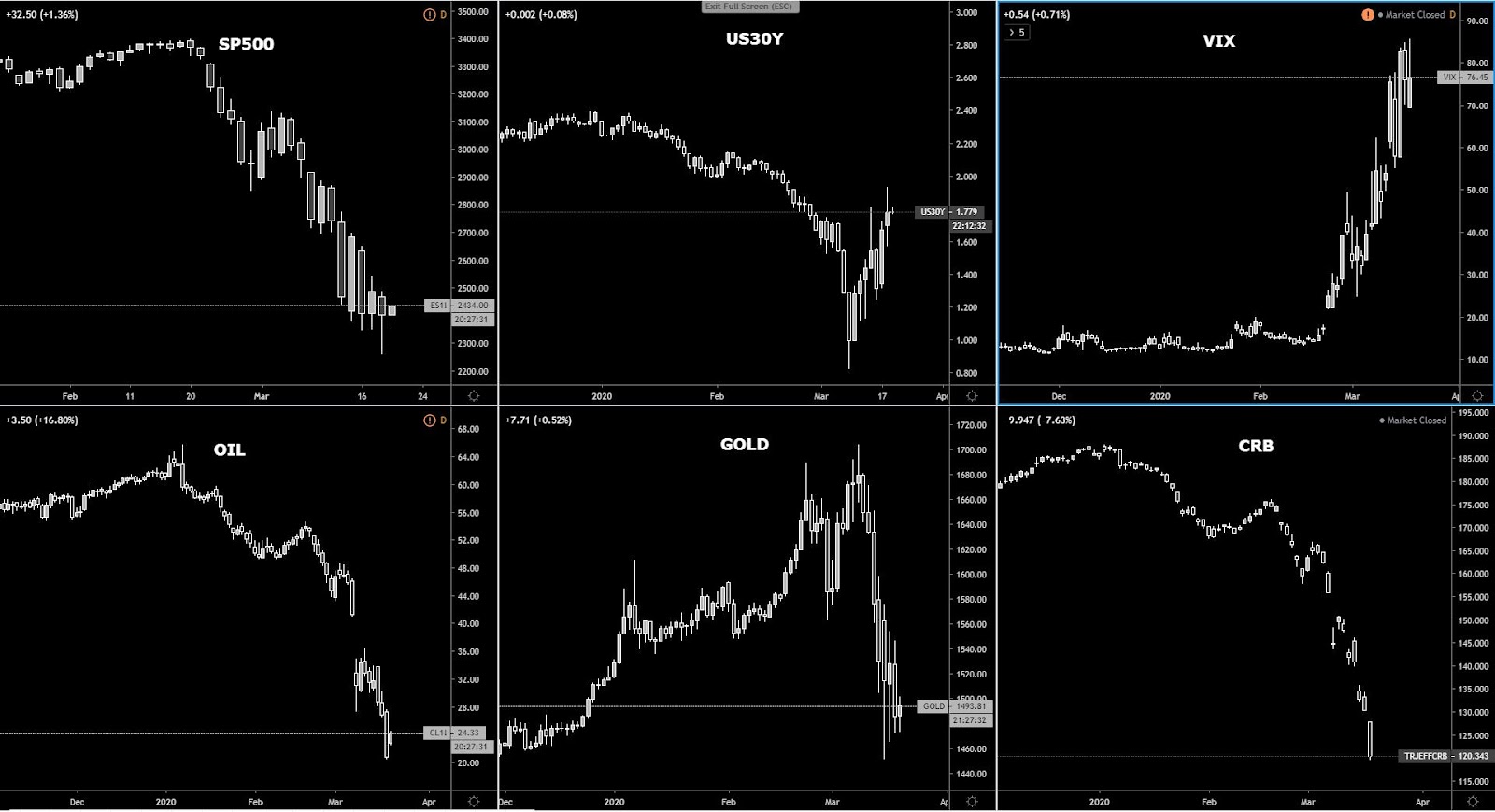

Risk-off returns: The cheerful mood in equities and bond yields following the political events in the US, where Biden has taken the front seat as the favorite Democrat nominee for the Presidential race, was all evaporated as the COVID-10 continues to dominate proceedings. The S&P 500, as the bellwether of the US stock market, registered a loss of -4% while the US 30-yr bond yield retests fresh record lows. The 10yr Treasury was -13.4bps to 0.92%, while the USD index, still weighted by the aggressive U-turn by the Fed in policies, also took a hit.

Funding currencies best performers: The interest towards funding currencies (EUR, CHF, JPY) is back as risk unwinds and vol increases. This combination was especially impactful for the interest of Yen bulls on Thursday. Remember, under the current conditions, as a byproduct of increases in the vol environment, it no longer becomes appealing for speculators to trade these currencies hoping to profit from the spread or carry trade between the low-interest fiat and a higher-yielding currency purchased with the funding strategy. For a more in-depth look into funding currencies, one can watch this video presentation I put together.

Fear of virus community spread in the US: The markets remain spooked of community transmission of the COVID-19 in the US and other countries around the globe. A few days back, the Washington Post reported that the virus has probably been spreading undetected for about six weeks in Washington state, noting that “a genetic analysis suggests that the cases are linked through community transmission and that this has been going on for weeks, with hundreds of infections likely in the state.” There is further evidence that this trend is now playing out.

‘Probability neglect’ behind COVID-19 over-reaction: At the core of this crisis by the coronavirus, even if numbers prove that way more people die of cancer, heart diseases or diabetes, and are good to put things into perspective, unfortunately , the human psyche is deeply rooted towards a cognitive bias called ‘probability neglect’. It is this bias that makes society panic and government over-react as a result. For a more detailed explanation, I highly recommend you to read this article by Bloomberg.

Untraceable transmissions = more uncertainty: We also learnt in recent days that Dr. Anthony Fauci - the director of the US National Institute of Allergy and Infectious Diseases, said "community spread" (infection via unknown origin) of the new coronavirus will be more common throughout the US. According to Fauci, “this was something that was entirely expected when you have diffuse infections throughout the world, sooner or later there are going to be cases in your country that you can’t directly trace…” Untraceable transmissions means more uncertainty about the full scope of the impact that COVID-19 will have on the global economy and for how long.

RBA’s YCC as favorite tool? As the RBA exhausts its conventional policy-setting tools, there is talk that as part of the conversations about QE, RBA’s preference would be to use an approach by which it targets a Yield Curve Control (YCC). According to Tapas Strickland from the National Australian Bank, “YCC is seen as the RBA’s least-worst option. YCC would entail the RBA setting a target on part of the yield curve, with the RBA only buying government bonds when the market tested the RBA’s credibility in maintaining the target. The end result would likely be an even flatter yield curve which could lower longer-end borrowing rates and perhaps risk premiums by reinforcing the commitment to keep the cash rate low for an extended period.”

Warren withdraws from the race: Elizabeth Warren is the last candidate to have dropped out of the Democratic nomination race even if she is yet to endorse a nominee. The betting markets are keeping Biden as the frontrunner with the chances of getting the Democrat nomination to run against Trump at around 85% after Super Tuesday’s victory and the support received by Bloomberg after he too pulled out of the race earlier this week. There has also been an improving trend for Democrats to get both the House and Senate in the election day.

GBP keeps rallying: The Pound continues to find further strength as the BoE is not yet fully committed to resort to rate cuts next week, judging by Governor Carney’s comments. He said that the collective response to virus will be powerful and timely with tools including special liquidity and macroprudential measures along with monetary policy instruments, noting that “we still have a lot of ammunition but we have to use space effectively .” Besides, EU’s Barnier reiterated that “there are many serious divergences with the UK on future relationship”, adding “we can get a good agreement for both sides despite 'very, very difficult' differences.”

BoC Poloz keeps door wide open to more cuts: BOC's Poloz made follow up comments after the decision by the Central Bank to cut rates by 50bp earlier this week. He said that he was shifted toward a rate cut regardless of the virus. There was plenty to sink in as part of his remarks, noting that “downside risks were more than enough to offset worries about leverage and financial vulnerabilities”, and that “Canada is headed for at least another quarter of weak GDP and Q2 could be weak as well.” Bottom line, the Central Bank, in Poloz’s words, “remains ready to cut further if necessary.”

Focus will briefly shift to the US NFP numbers: The data will refer to February and consensus looks for a solid print of 175k with unchanged unemployment at 3.6% and wages growth of 3%. These estimates are a subtle downgrade from the previous month. Note, given the extraordinary times we are living with the COVID-19, the US NFP is seen as a secondary indication to change the Fed’s policy path. That said, there are some significant risks that a softer number may help justify further rate cuts by the Fed, while a strong one will likely be dismissed on the basis that the print is yet to reflect the slowdown that the COVID-19 is set to cause.

Nomura’s take on the COVID-19 and Why CB action won’t cut it: In expectations of further coordinated responses by Central Banks, Nomura's economists cautioned that "macroeconomic policies are less well equipped to help (or “can only help so much”). If health security controls fail to contain the spread of COVID-19, financial markets may soon have to accept that a global recession is a forgone conclusion." Nomura predicts that the COVID-19 cases are yet to skyrocket to a projected 1.5 million worldwide.

Oil back under pressure: Oil has also shed its recent gains this week, down more than 2% below $46.00 after news broke out that OPEC members would agree to a 1.5m barrel a day cut conditional to Russia also joining, which is not looking as a high likelihood at this point.

If you found this fundamental summary helpful, just click here to share it!

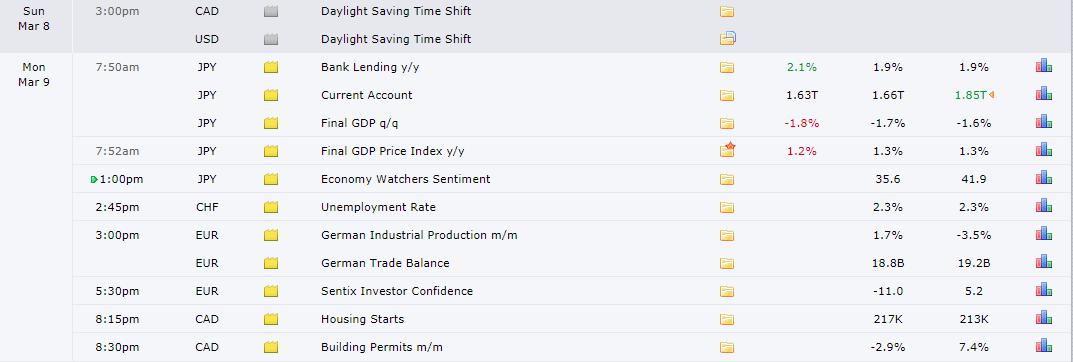

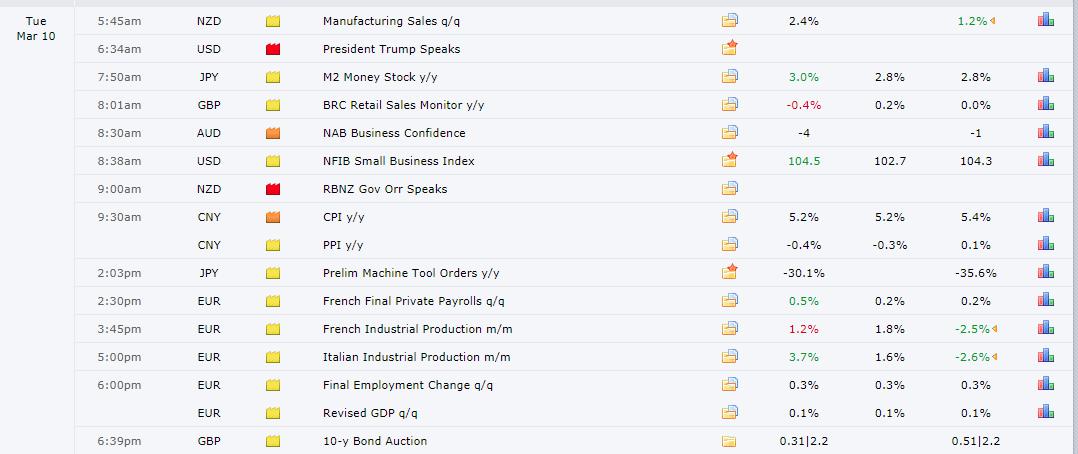

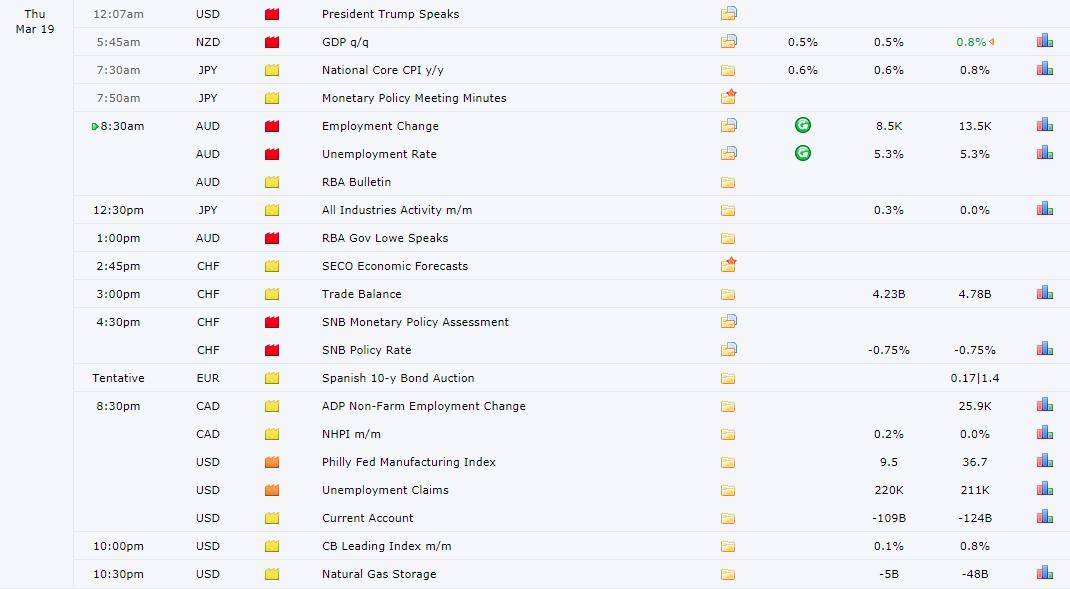

Recent Economic Indicators & Events Ahead

Source: Forexfactory

If interested in the best ‘free of charge’ News Indicator that can display data on past and future news in the Forex market via MT4, check this YouTube video I produced. The indicator allows you to save time, avoid mistakes. It’s spot on!

Insights Into Forex Flows

The indices show the performance of a particular currency vs G8 FX. An educational video on how to interpret these indices can be found in the Global Prime's Research section. The idea of this analysis is to complement one’s daily bias so that traders can make better and smarter decisions by accounting for the aggregation of flows.

If you found the content in this section valuable, give us a share by just clicking here!

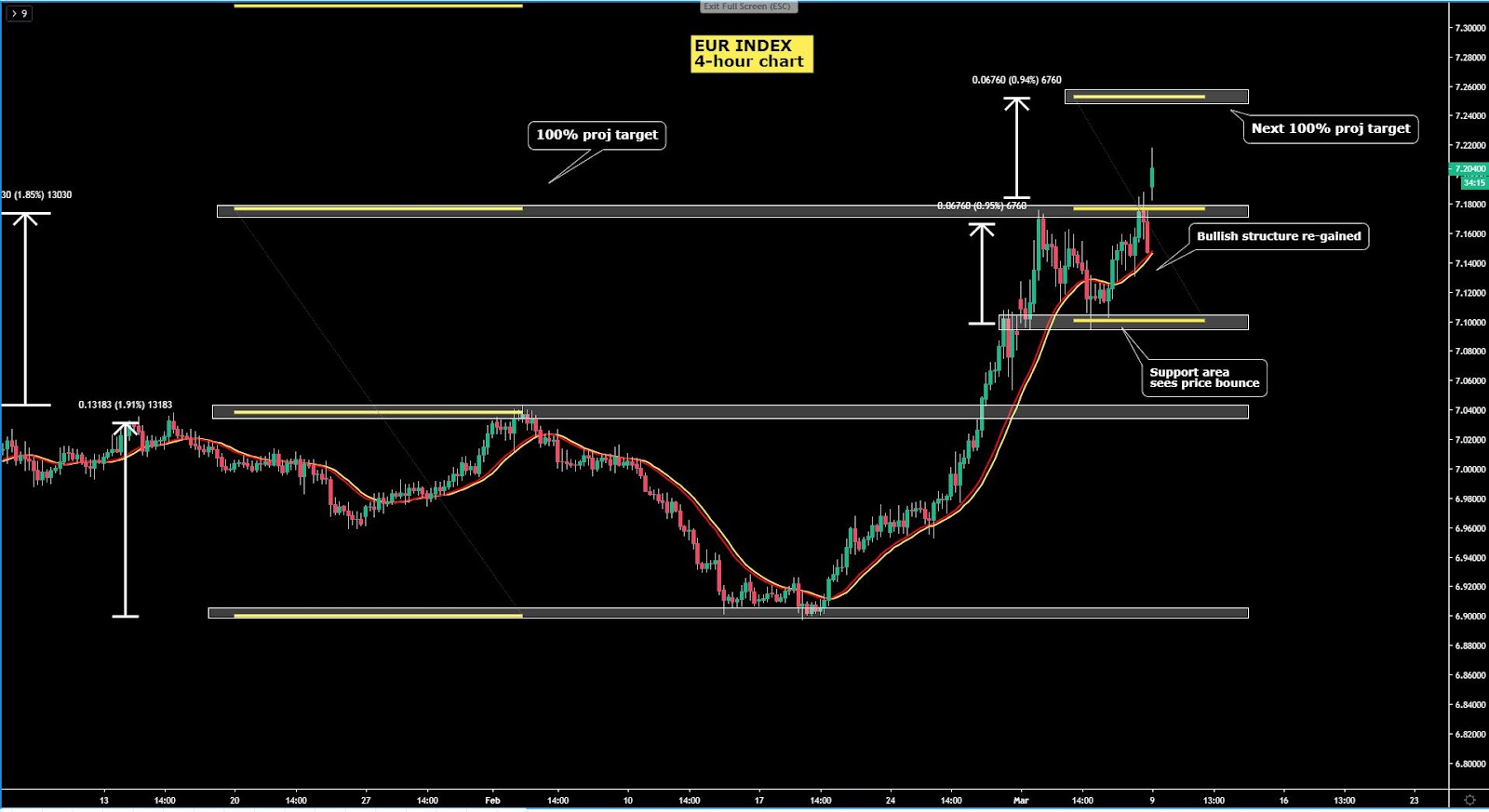

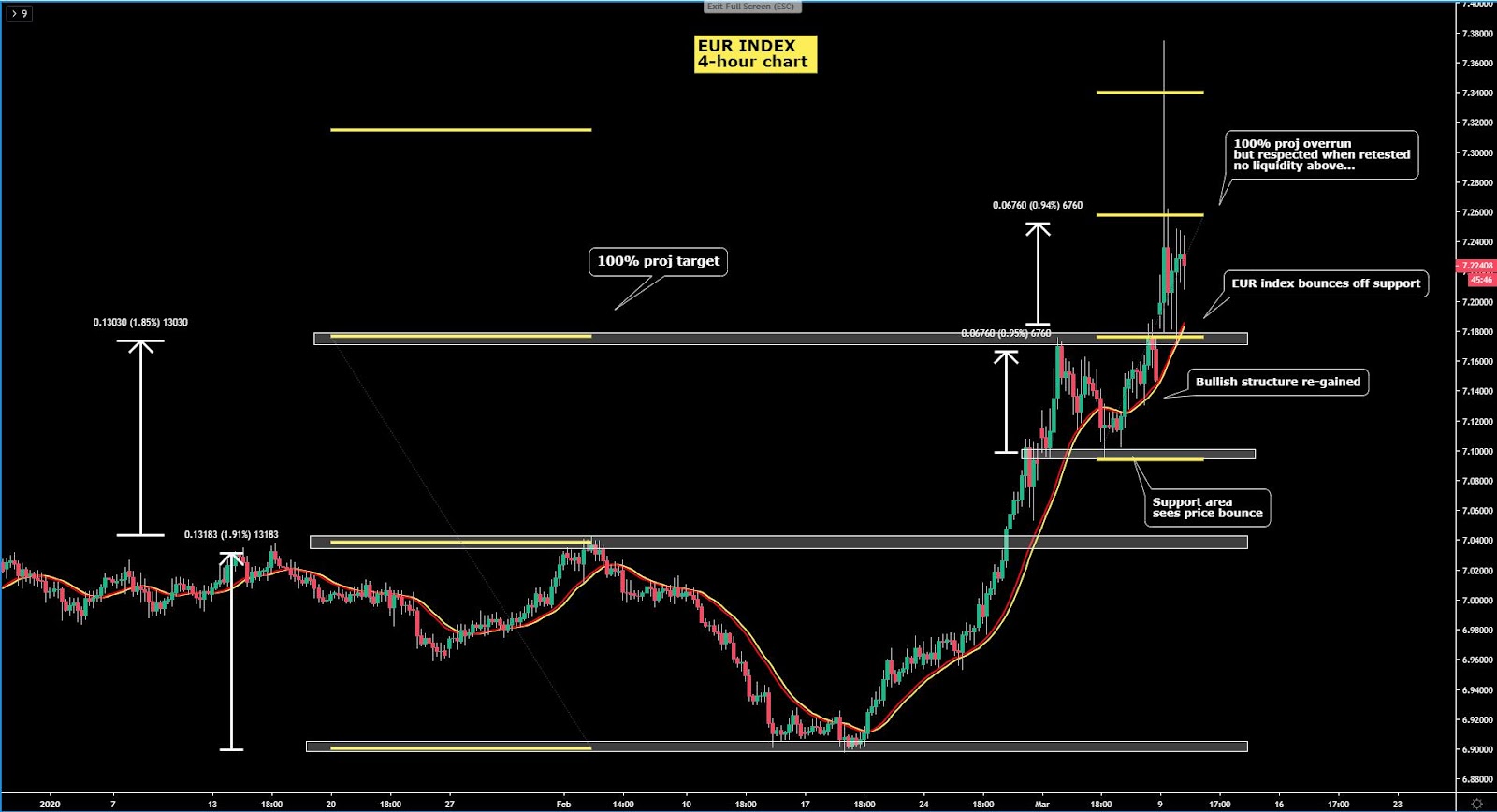

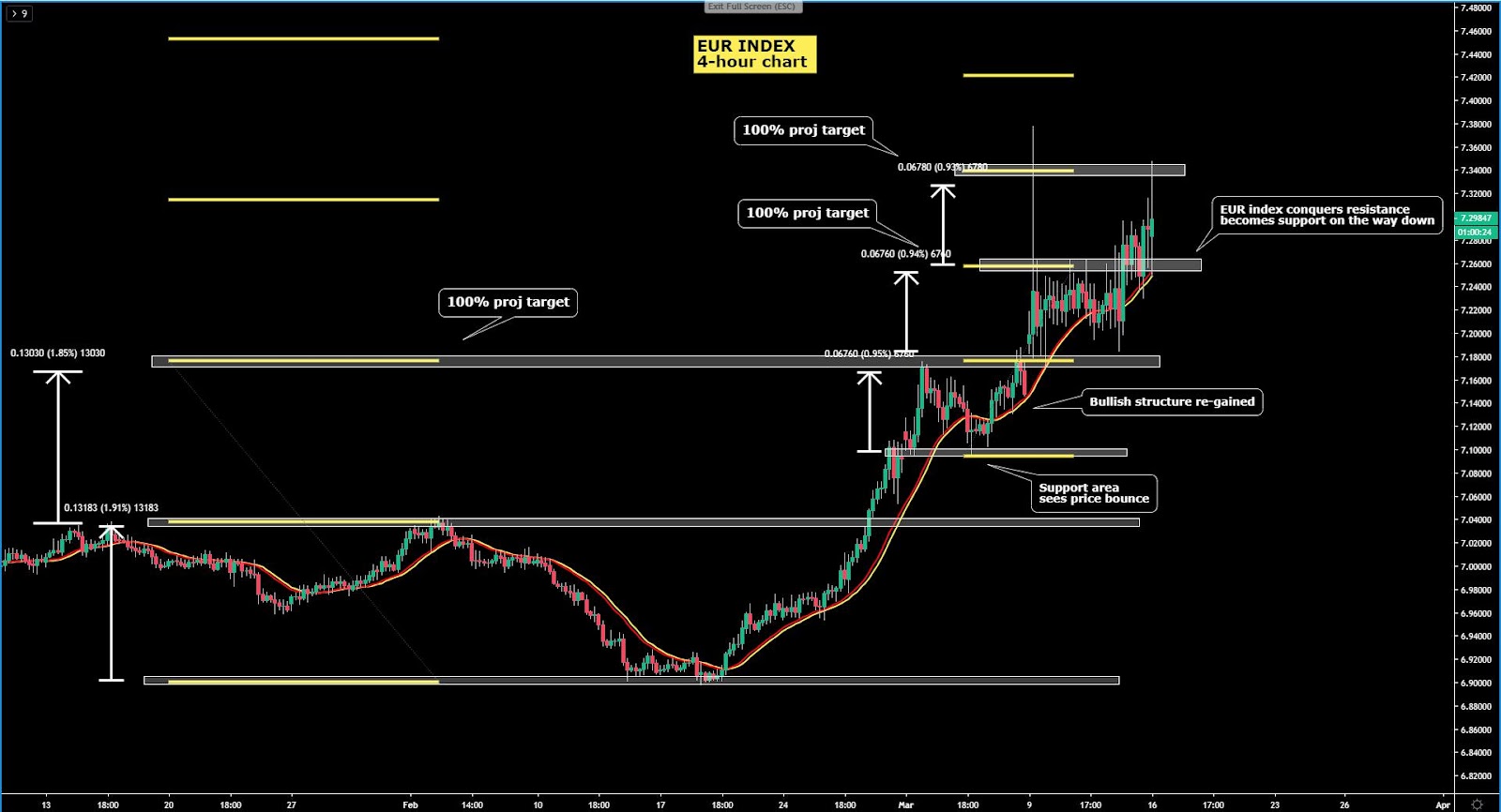

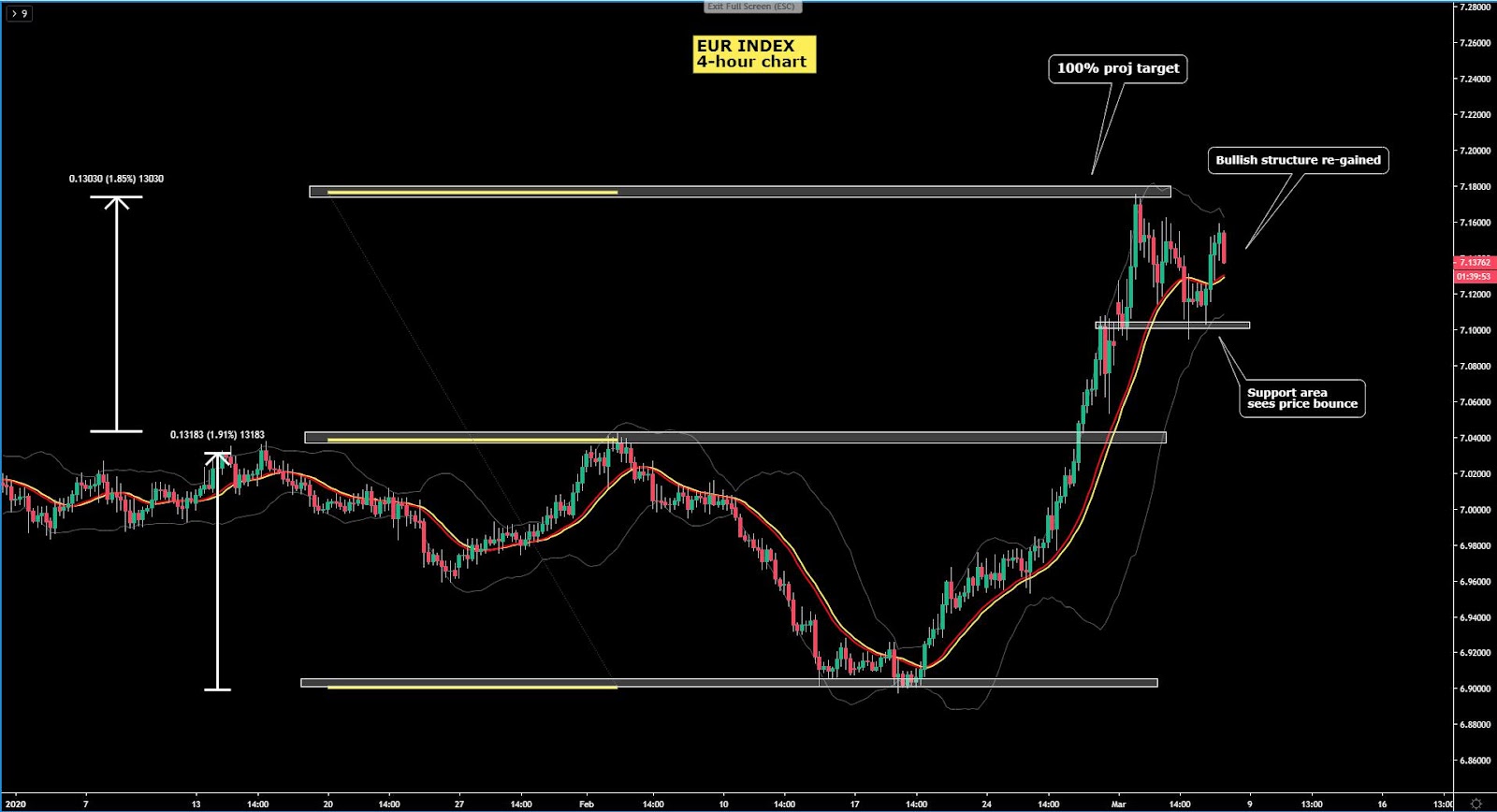

The EUR index regained the upside as the 4-hour chart below shows. The chart is still capped by the 100% projection target but is undeniable that at this stage, it remains very risky to be shorting the Euro as further unwind of carry trades remains a tail risk. Notice, the smart money tracker has also reversed its course back up, shifting the focus to a retest of the previous highs.

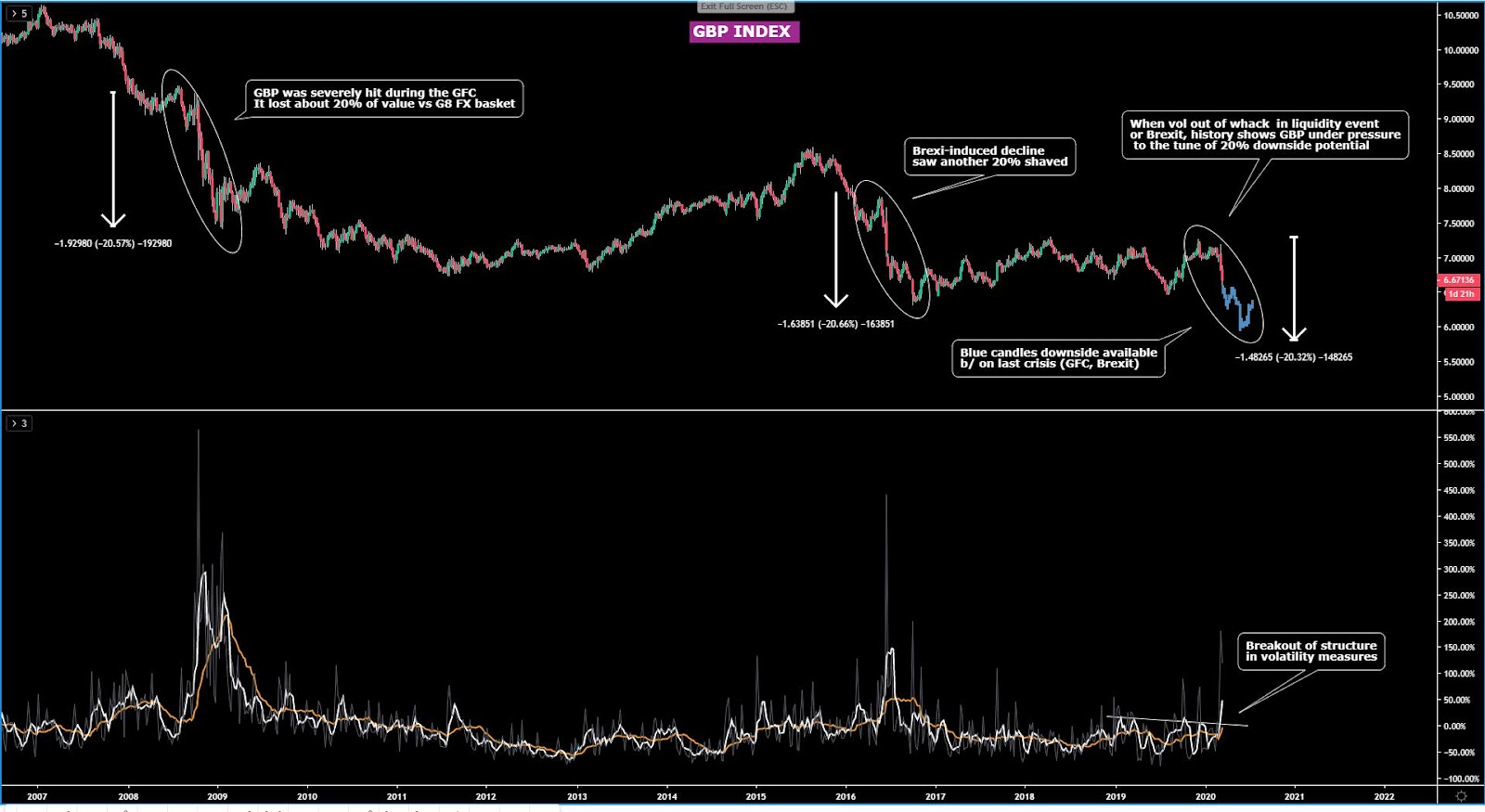

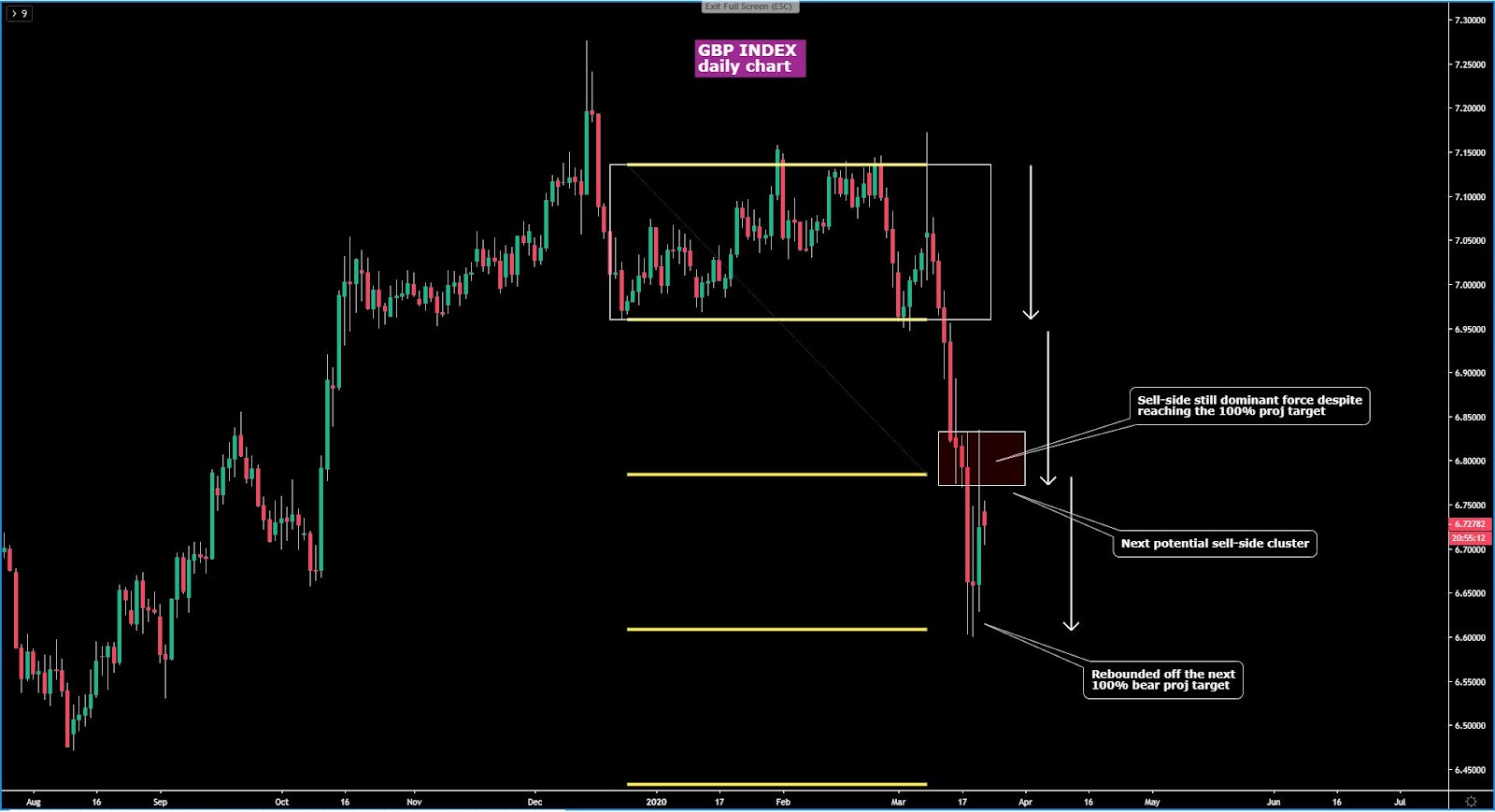

The GBP index, on the back of a rebound off a macro level of support after printing a compression off the lows, it finally found a strong pocket of supply by revisiting a key level of resistance where the currency is struggling. While the 4-hour outlook in the GBP chart has turned more positive, this area is definitely a candidate location for the sell-side pressure emanating off the daily chart to return, be aware of that.

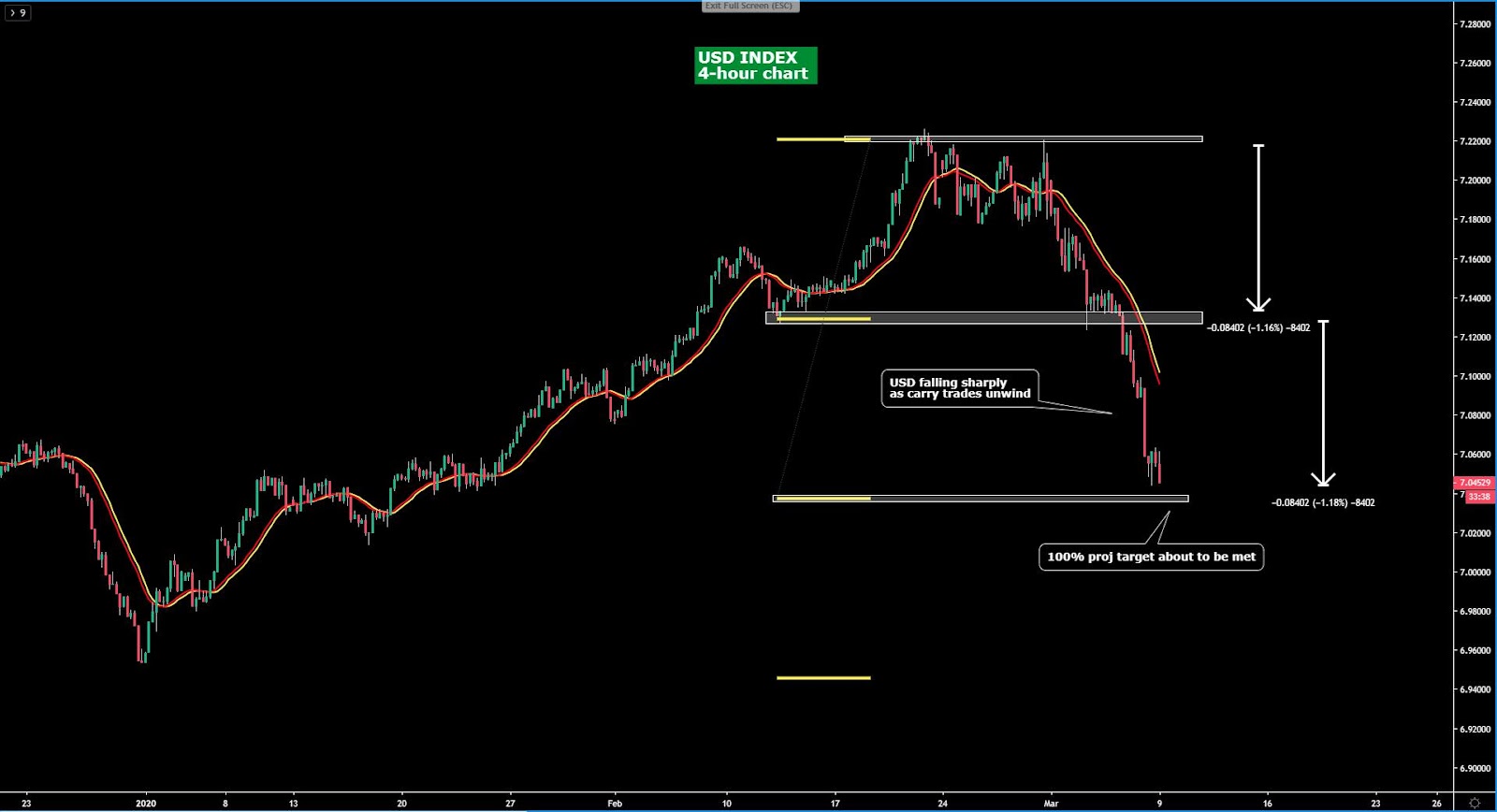

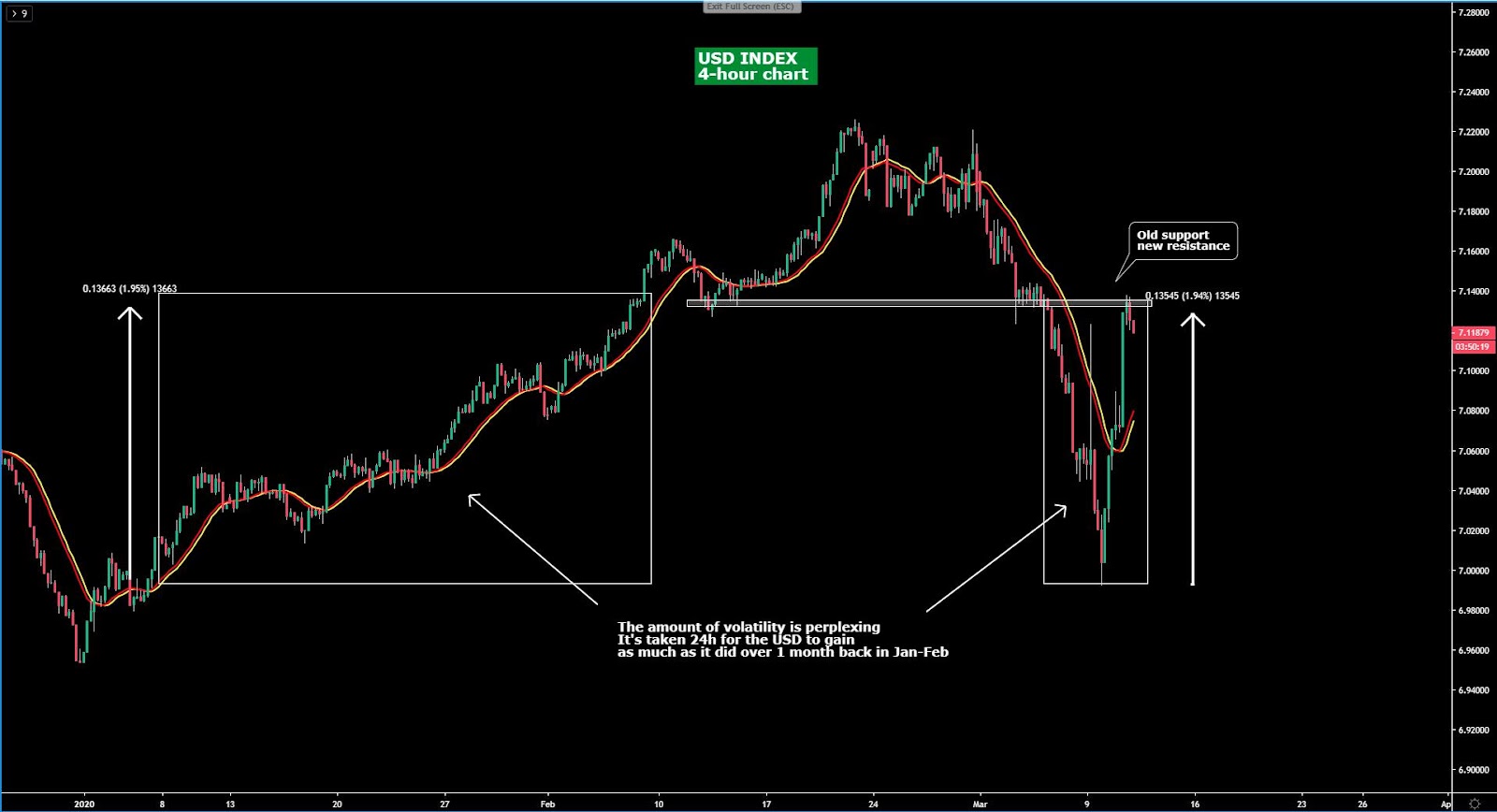

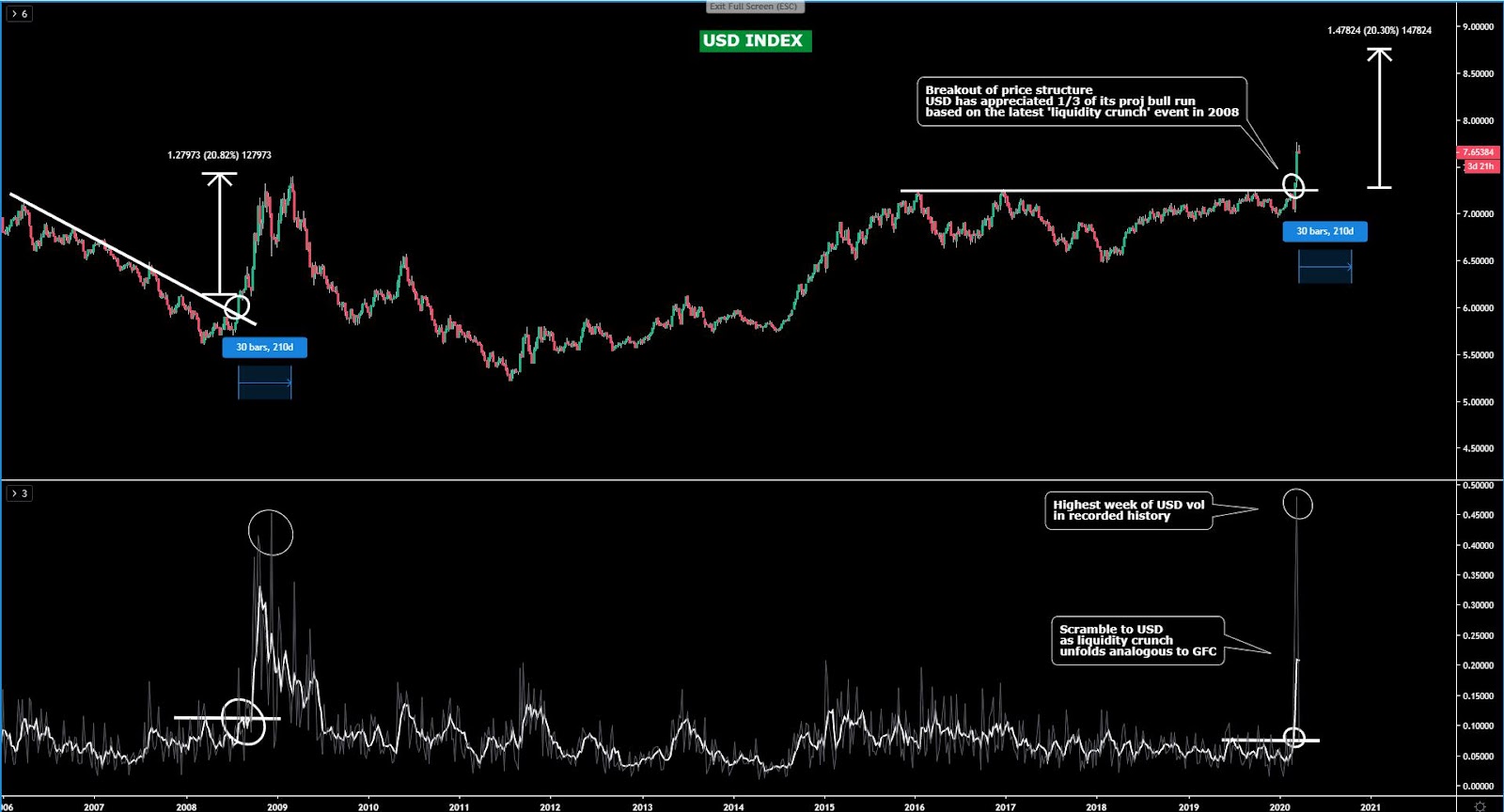

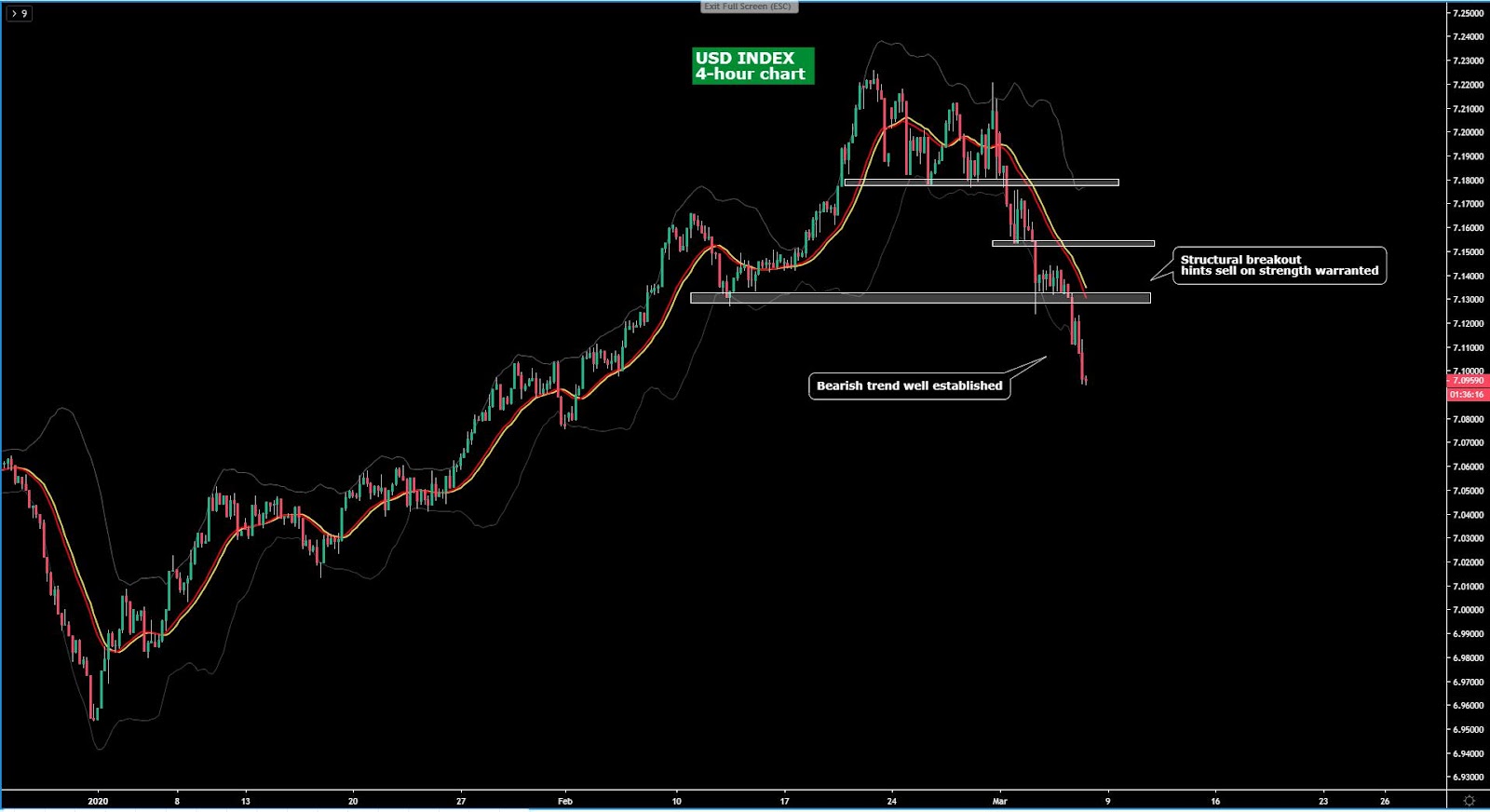

The USD index has finally cracked a level of key support which reinforces the bearish bias as the picture continues to deteriorate. The market keeps pricing in further Fed easing, which along with the escape of long carry trade structures makes the USD vulnerable. Bottom line, there is renewed technical evidence that the USD is a sell on strength currency at the moment.

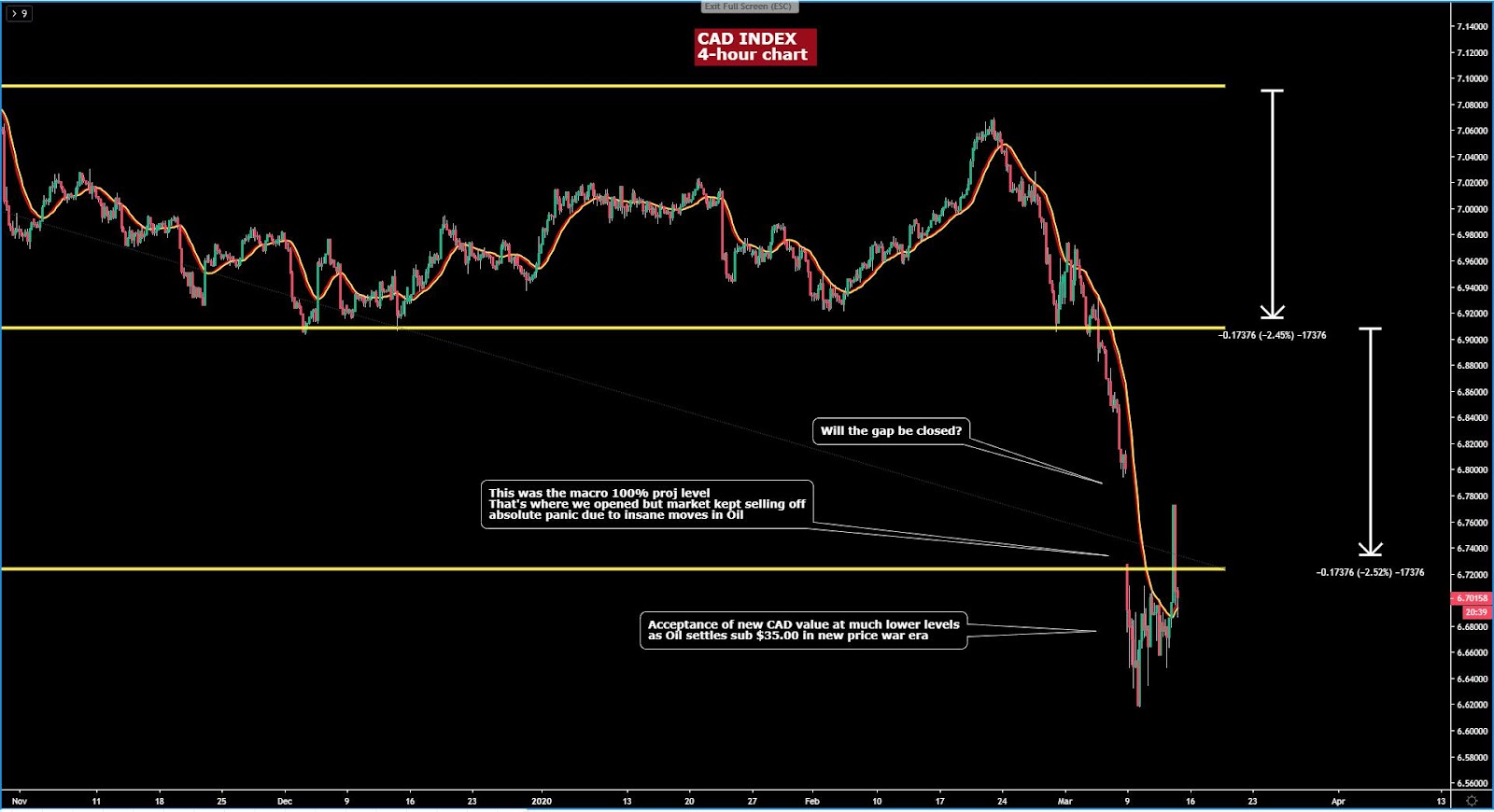

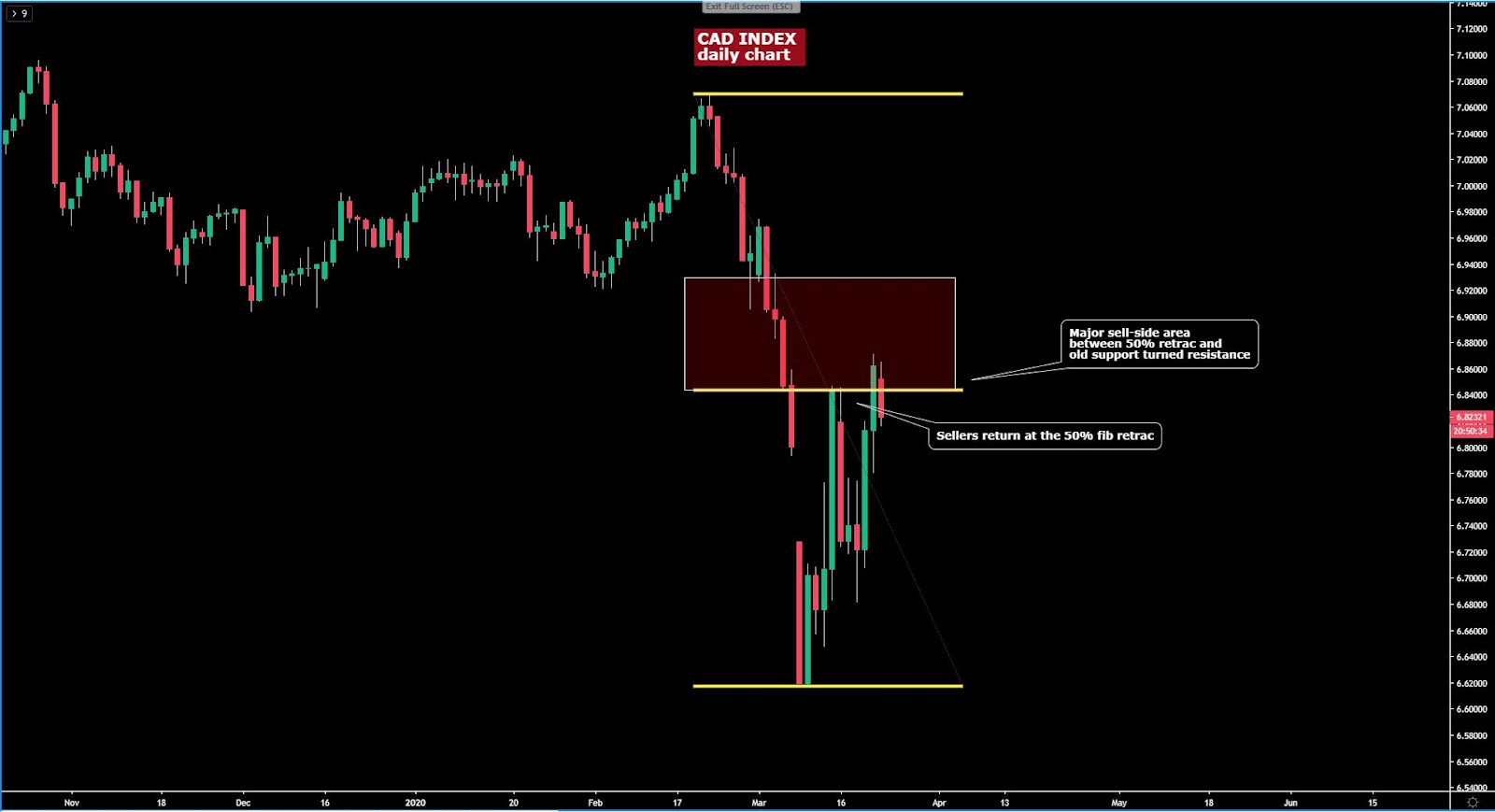

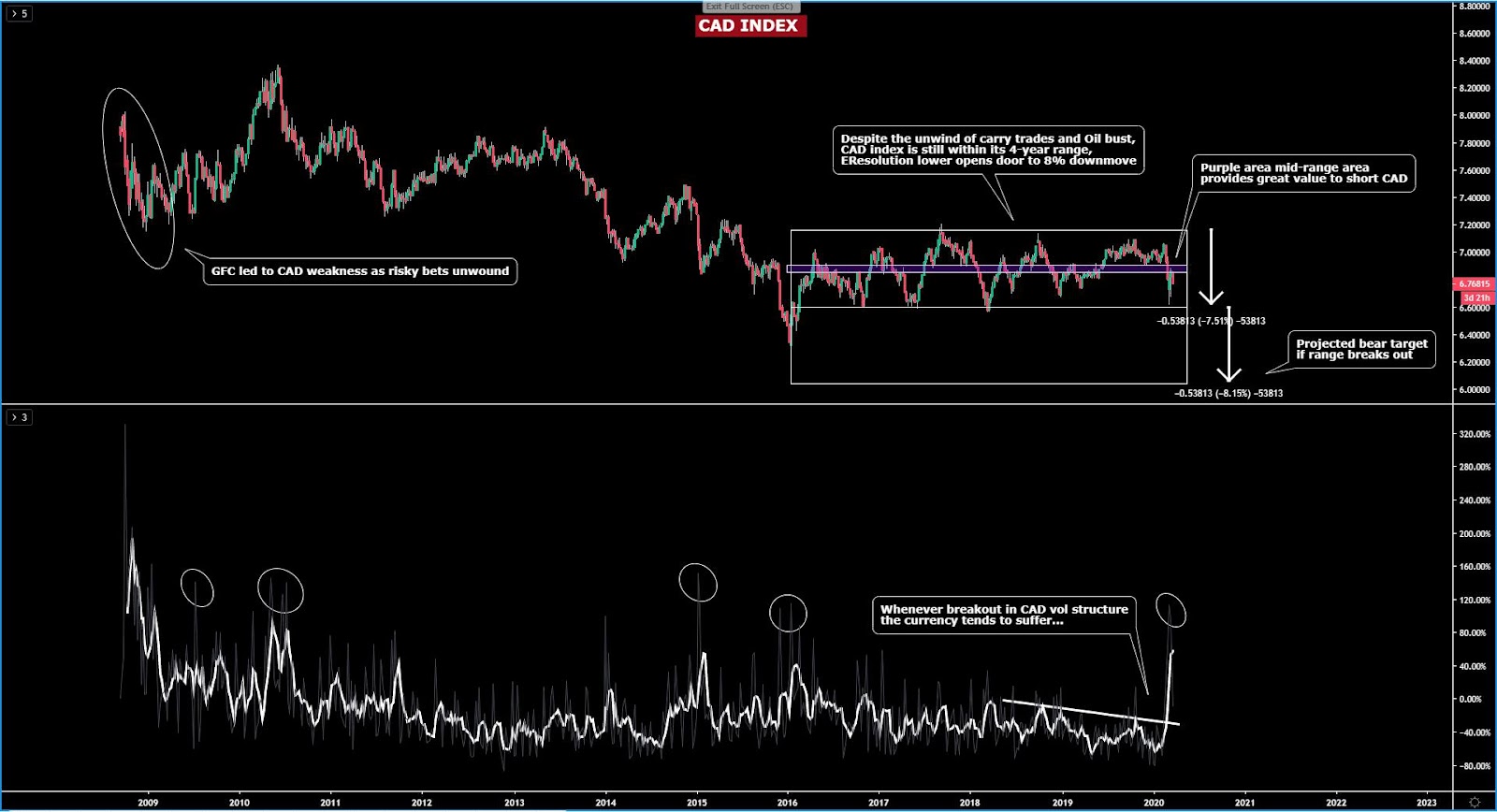

The CAD index keeps selling off on a perfect bearish storm of further unwind of carry trades and a bold move by the BOC to cut rates by 50bp but most importantly, hint at more cuts. The impulsive drop in the currency has now reached what I interpret as oversold conditions, which is what happens when the 100% proj target is met. The validation of the bearish cycle with follow through supply going through the books makes the CAD a sell on strength but note that the position it trades at offers an awful pricing to keep adding shorts unless it corrects higher.

The JPY index, with risk aversion back in vogue, has risen to retest a key level of resistance, which corresponds to the origin of last year’s supply imbalance area. The bias off the 4-hour chart remains bullish and as a result, the safest bet is to keep betting for Yen strength until technicals prove otherwise. Just be aware that the bias doesn’t imply buying Yens off the bat as the level it trades at I consider it to be rather expensive and straight into resistance. Allowing the release of the buy-side pressure towards lower levels will give better entry points.

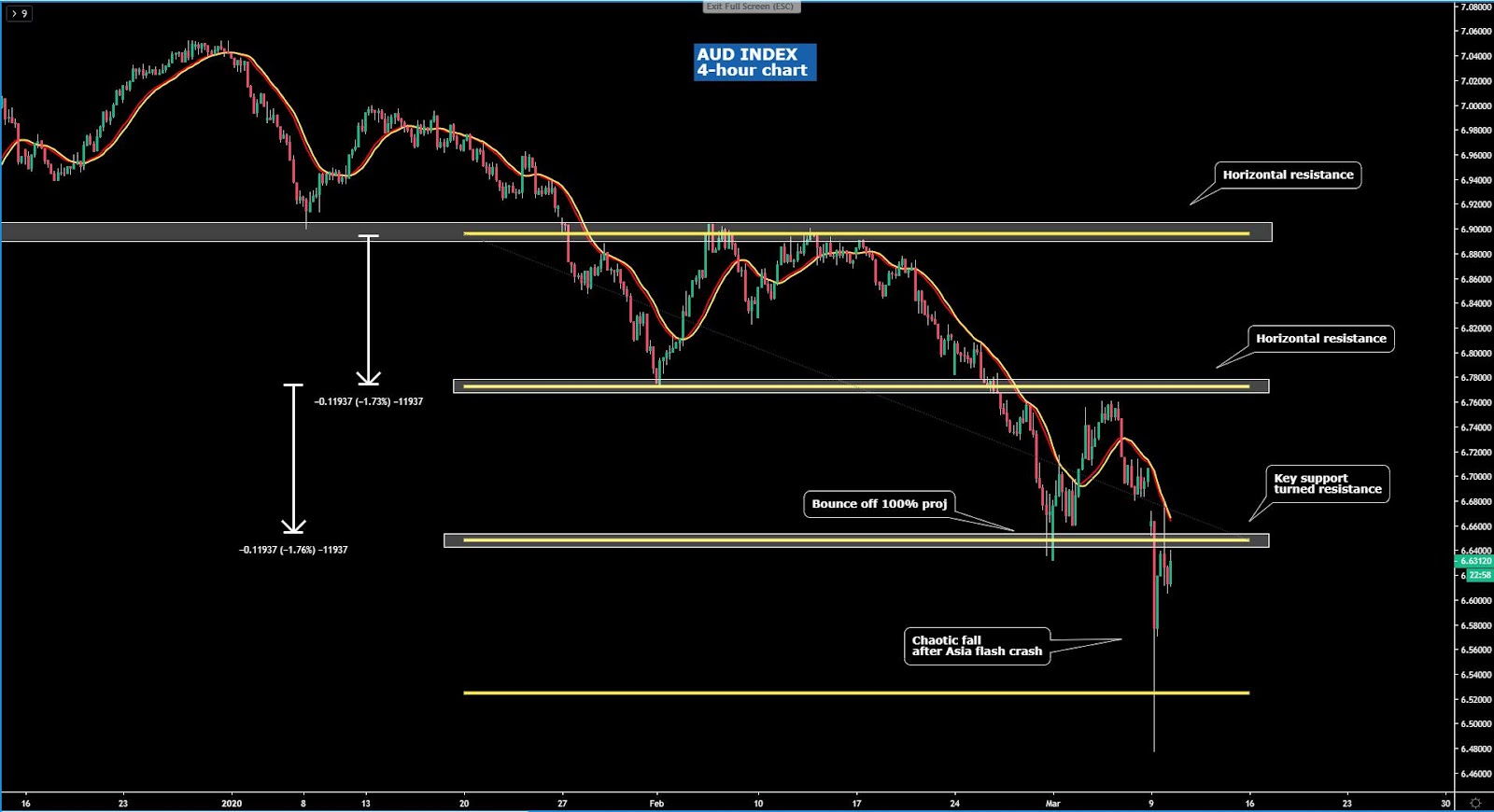

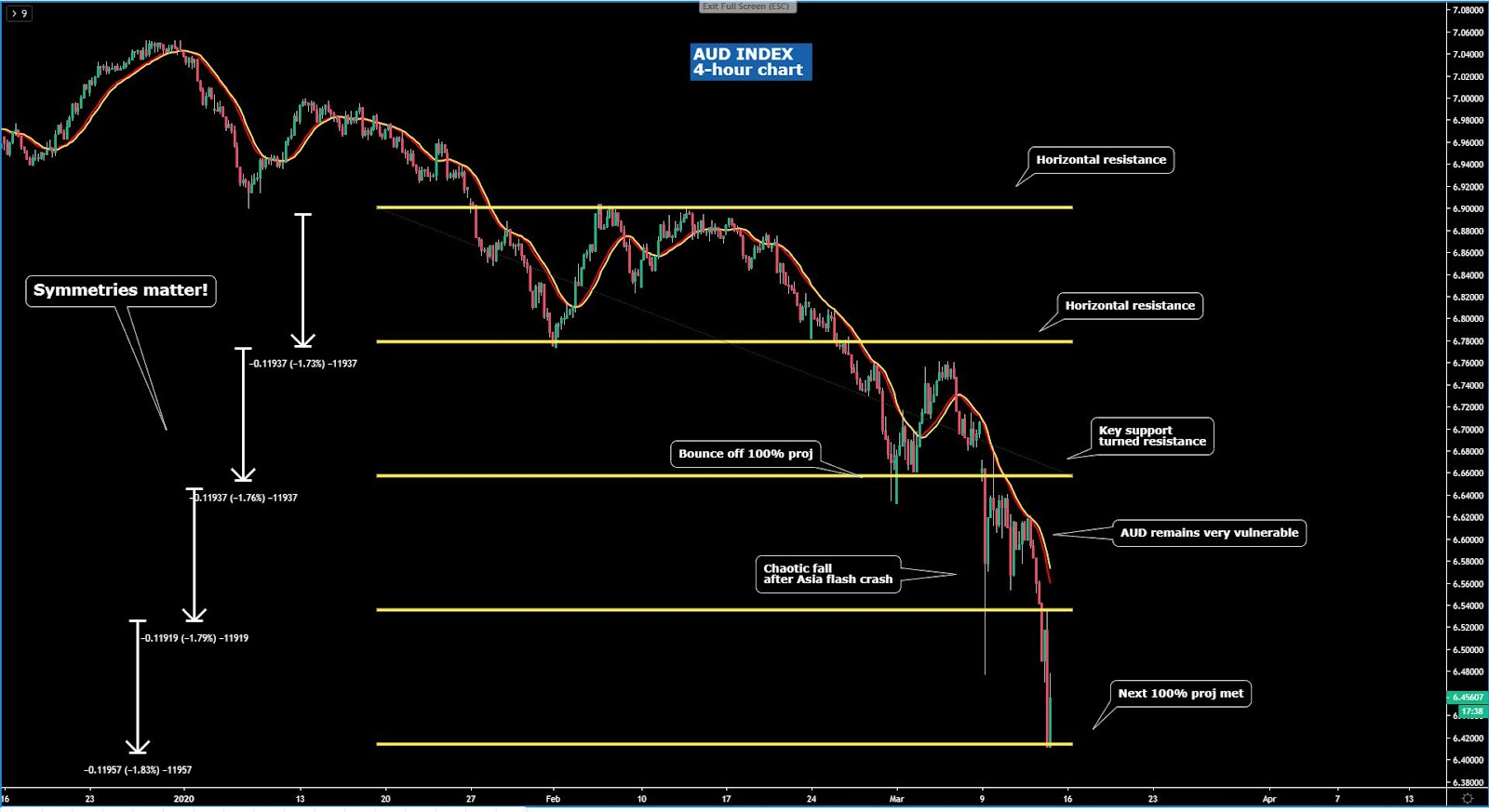

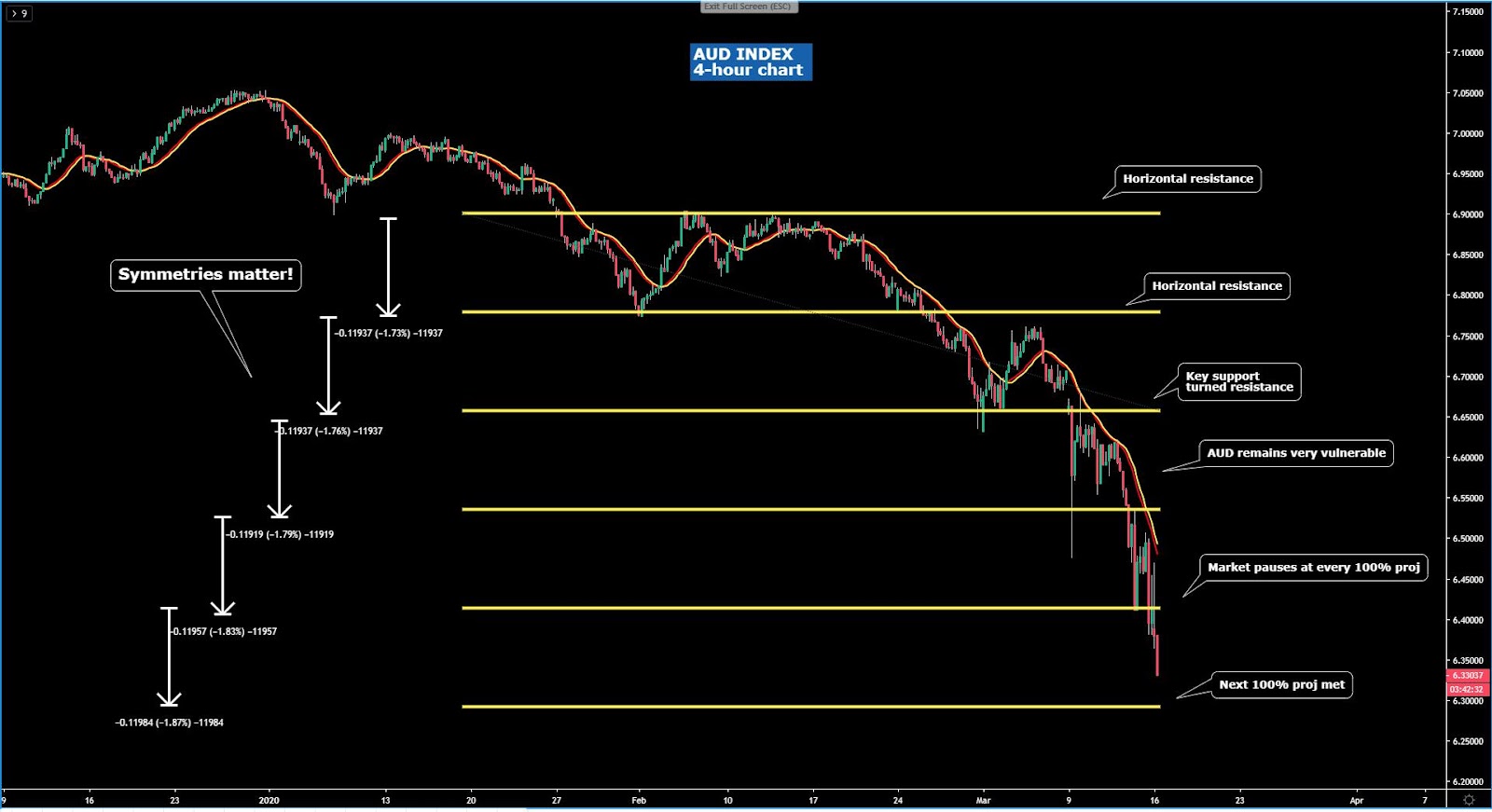

The AUD index has invalidated its short-term positive dynamics as the market structure returns back to bearish with the positive flow effects off the 100% bearish projection target overwhelmed by the return of the risk averse conditions in the market. There is again re-alignment between the macro and the trend in lower time frames, so the AUD is once again, a solid candidate to project weaker levels in coming sessions.

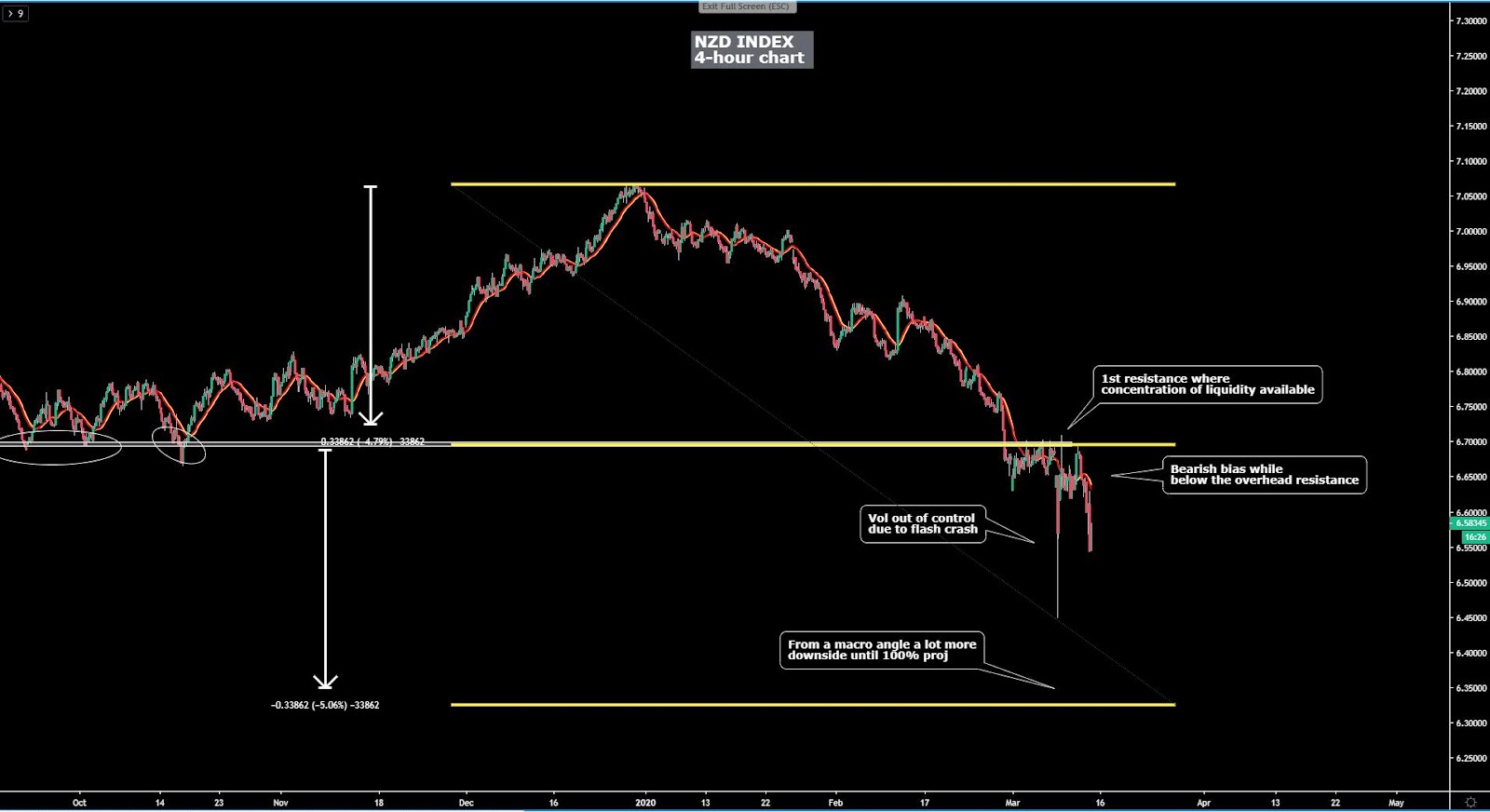

The NZD index still shows fragility. I made the point yesterday that the NZD remains the most vulnerable currency out of the G8 FX space. My reasoning is that even on the ephemeral return of risk appetite due to Super Tuesday, the currency saw very limited buy-side flows, with the immediate resistance acting as sellers’ strongholds for now. My base case remains, which is, don’t be a hero being long this currency intraday as technicals paint a bleak picture.

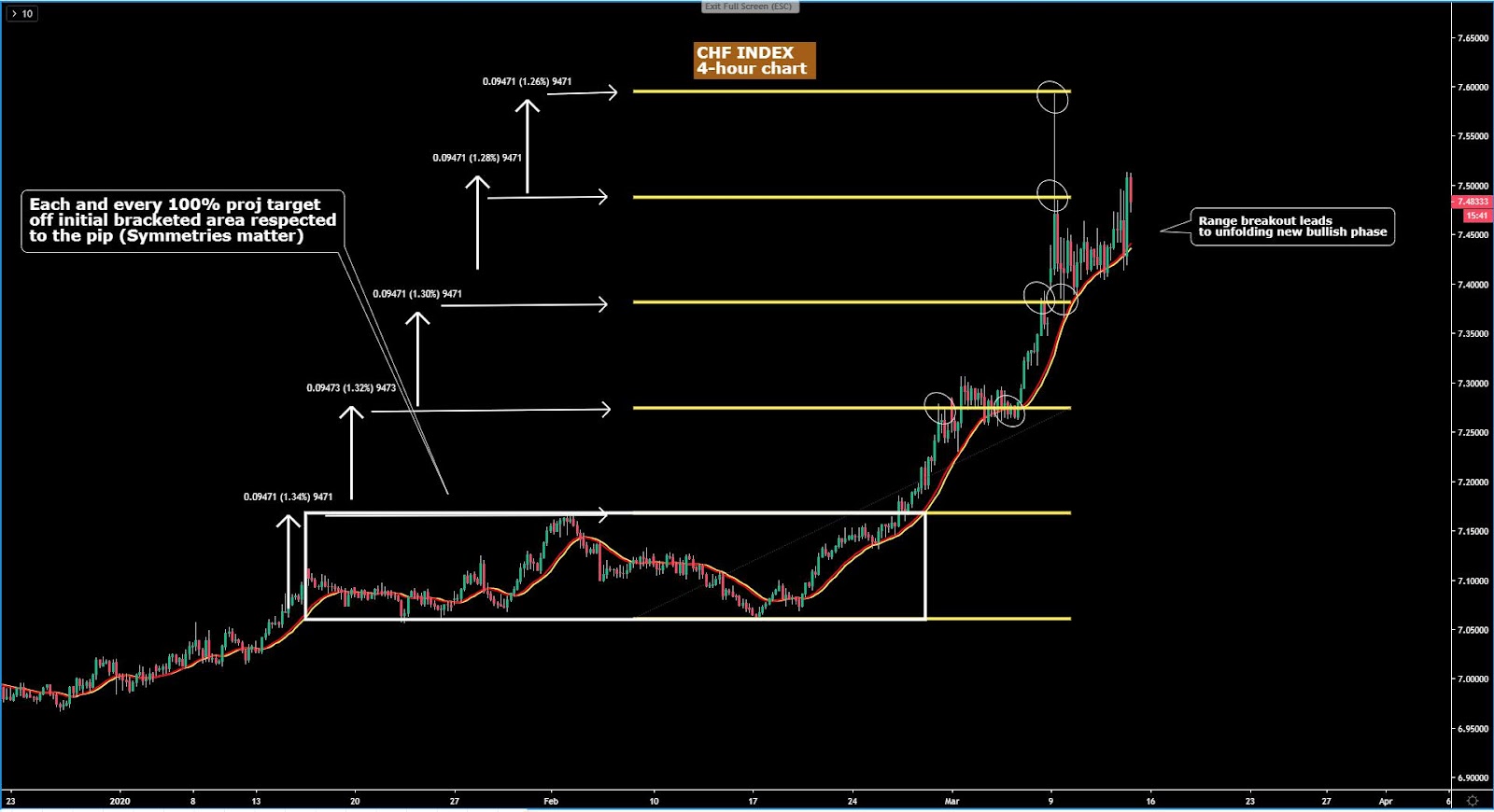

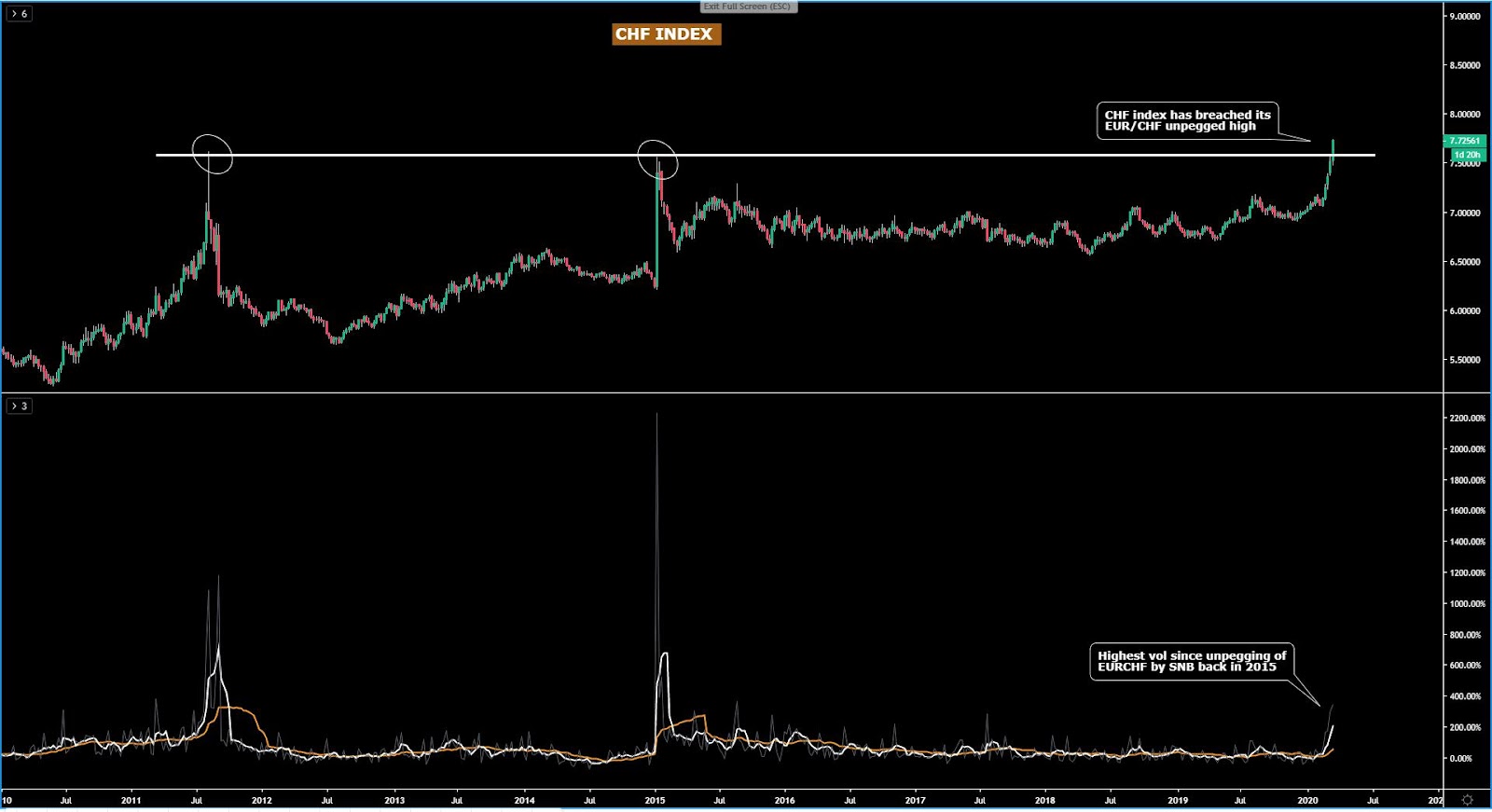

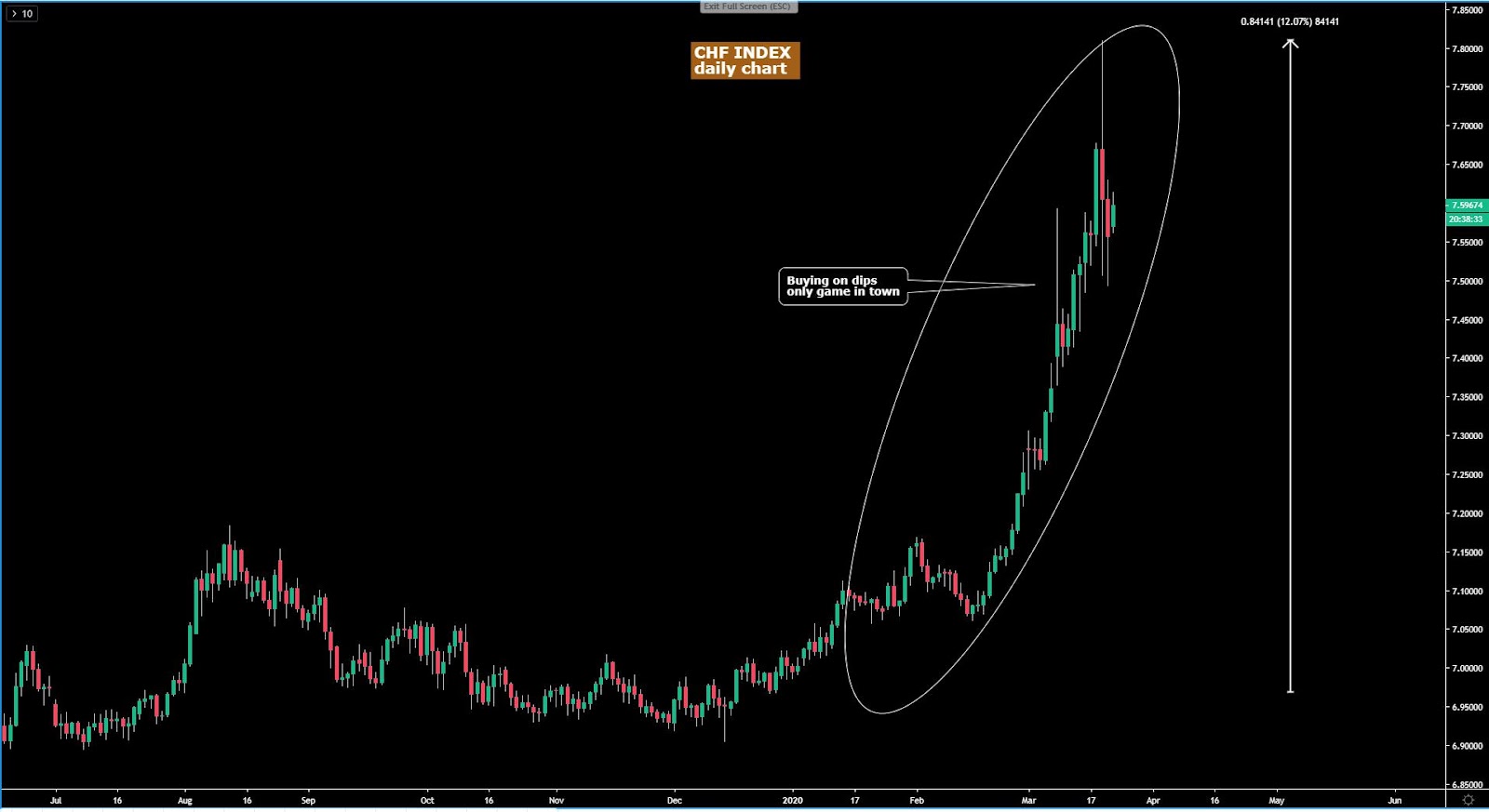

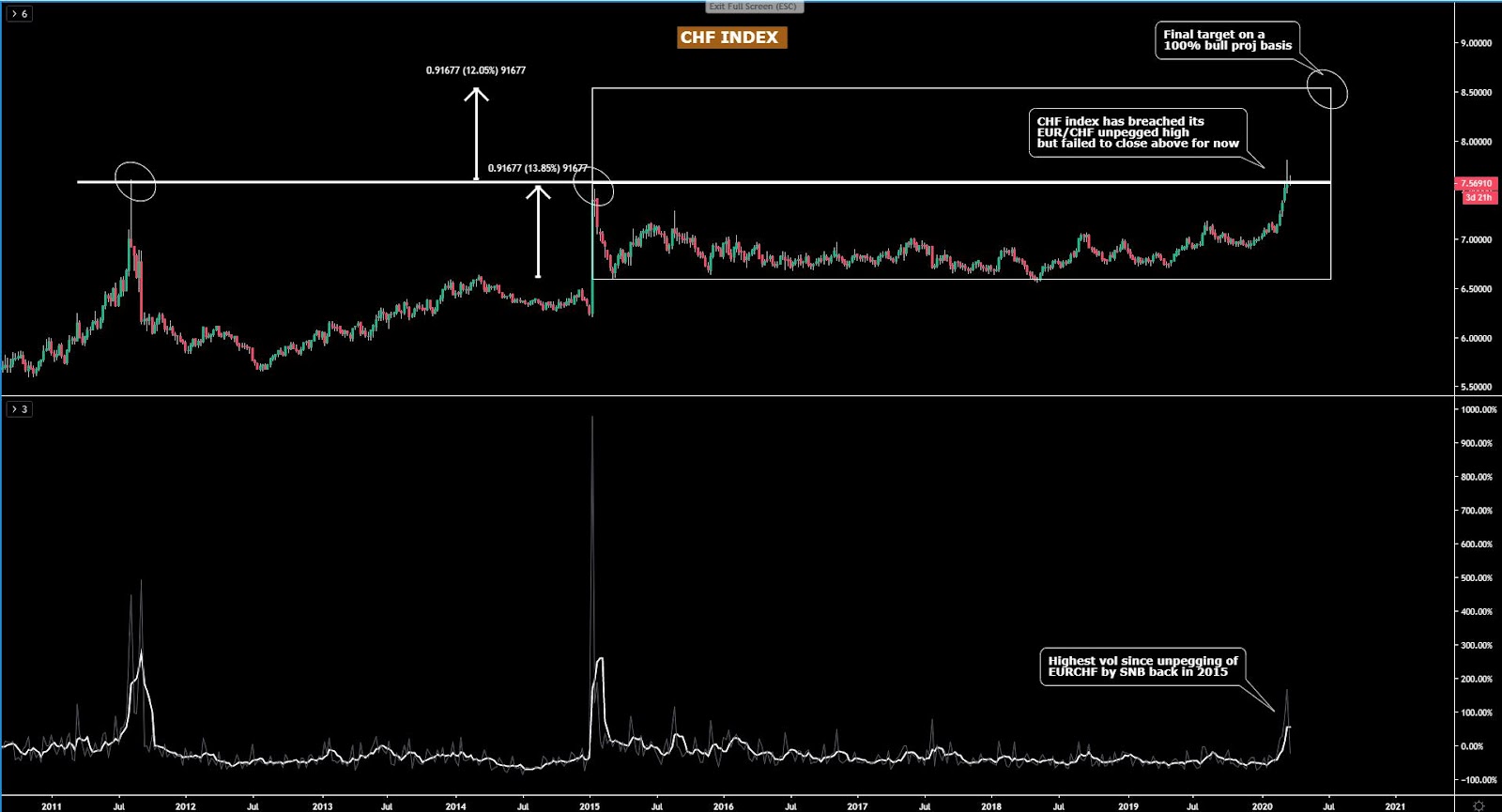

The CHF index has shown a greater level of buy side commitment than the Euro this week, as reflected by the fact that the currency broke and held above its 100% bullish proj target. The aggregated flows into the Swiss Franc now show that the index has finally expanded into new highs, what I refer to as a successful bullish rotation. This new buy-side commitment should attract buy on dip strategies in line with the macro/micro trends.

Important Footnotes

Yen Crosses Plummet As Risk-Off Returns

The recovery in risk appetite has been rather ephemeral, with the circuit breaker via Central Banks' easing (Fed, RBA, BOC) no having the desired effects to contain the fears of the coronavirus quickly evolving into a global pandemic. The disregard towards the macro-policy stimulus is an admission by Mr. Market of the limited effects this is going to have on a pick up in economic activity. As a result, the behavior of the markets remain reminiscent of an acceptance that a global recession is a forgone conclusion. Amid this backdrop, funding currencies rule.

The Daily Edge is authored by Ivan Delgado, 10y Forex Trader veteran & Market Insights Commentator at Global Prime. Feel free to follow Ivan on Twitter & Youtube weekly show. You can also subscribe to the mailing list to receive Ivan’s Daily wrap. The purpose of this content is to provide an assessment of the conditions, taking an in-depth look of market dynamics - fundamentals and technicals - determine daily biases and assist one’s trading decisions.

Let’s get started…

- Quick Take

- Narratives in Financial Markets

- Recent Economic Indicators

- Insights Into Forex Flows

- Educational Material

Quick Take

So far, the easing measures by the Fed, RBA and BOC have provided a very limited relief rally to the underlying risk-off dynamics, with the funding currencies’ complex still the place to be. Even the added groovy vibes via the major boost of Biden winning the Democration nomination have lasted barely 24h, with the market psyche still deeply rooted towards the COVID-19 as the big macro theme of 2020 as fears of widespread community transmissions in the US mount. As the day went on, risk trades softened and this led to Yen buying, while the Swiss Franc and the Euro followed in lockstep, although the buying flows were not as strong.

The G8 FX indices below illustrates the massive gap that has opened up as a result of the unwind of carry trades with hedges/margin calls favoring funding currencies amid a sky-high VIX. The snowball effect of bailing out carry trade long structures is the decay of the USD & CAD attractiveness, with the aggressive reduction in rates this week fueling the supply flows. The dicey environment created by the COVID-19 impact on world-wide economies is keeping the outlook for the Aussie and New Zealand Dollar very negative as the race to the bottom by the RBA/RBNZ is on as the market is now fixated on RBA’s QE measures later this year.

Amid such huge uncertainty for the global economy this year, the perky Pound has been gaining ground quietly, even if the negative backdrop of tough trade talks between the EU and the UK, coupled with a BOE that may follow the same path of other Central Banks, threatens the sustainability of this run. All in all, the trend this week has been well defined, with funding currencies the safest bets while carry long currencies (USD, CAD) and Oceanic (AUD, NZD) are suffering.

The indices show the performance of a particular currency vs G8 FX. An educational video on how to interpret these indices can be found in the Global Prime's Research section.

If you found the content in this section valuable, give us a share by just clicking here!

Narratives In Financial Markets

* The Information is gathered after scanning top publications including the FT, WSJ, Reuters, Bloomberg, ForexLive, Twitter, Institutional Bank Research reports.

Risk-off returns: The cheerful mood in equities and bond yields following the political events in the US, where Biden has taken the front seat as the favorite Democrat nominee for the Presidential race, was all evaporated as the COVID-10 continues to dominate proceedings. The S&P 500, as the bellwether of the US stock market, registered a loss of -4% while the US 30-yr bond yield retests fresh record lows. The 10yr Treasury was -13.4bps to 0.92%, while the USD index, still weighted by the aggressive U-turn by the Fed in policies, also took a hit.

Funding currencies best performers: The interest towards funding currencies (EUR, CHF, JPY) is back as risk unwinds and vol increases. This combination was especially impactful for the interest of Yen bulls on Thursday. Remember, under the current conditions, as a byproduct of increases in the vol environment, it no longer becomes appealing for speculators to trade these currencies hoping to profit from the spread or carry trade between the low-interest fiat and a higher-yielding currency purchased with the funding strategy. For a more in-depth look into funding currencies, one can watch this video presentation I put together.

Fear of virus community spread in the US: The markets remain spooked of community transmission of the COVID-19 in the US and other countries around the globe. A few days back, the Washington Post reported that the virus has probably been spreading undetected for about six weeks in Washington state, noting that “a genetic analysis suggests that the cases are linked through community transmission and that this has been going on for weeks, with hundreds of infections likely in the state.” There is further evidence that this trend is now playing out.

‘Probability neglect’ behind COVID-19 over-reaction: At the core of this crisis by the coronavirus, even if numbers prove that way more people die of cancer, heart diseases or diabetes, and are good to put things into perspective, unfortunately , the human psyche is deeply rooted towards a cognitive bias called ‘probability neglect’. It is this bias that makes society panic and government over-react as a result. For a more detailed explanation, I highly recommend you to read this article by Bloomberg.

Untraceable transmissions = more uncertainty: We also learnt in recent days that Dr. Anthony Fauci - the director of the US National Institute of Allergy and Infectious Diseases, said "community spread" (infection via unknown origin) of the new coronavirus will be more common throughout the US. According to Fauci, “this was something that was entirely expected when you have diffuse infections throughout the world, sooner or later there are going to be cases in your country that you can’t directly trace…” Untraceable transmissions means more uncertainty about the full scope of the impact that COVID-19 will have on the global economy and for how long.

RBA’s YCC as favorite tool? As the RBA exhausts its conventional policy-setting tools, there is talk that as part of the conversations about QE, RBA’s preference would be to use an approach by which it targets a Yield Curve Control (YCC). According to Tapas Strickland from the National Australian Bank, “YCC is seen as the RBA’s least-worst option. YCC would entail the RBA setting a target on part of the yield curve, with the RBA only buying government bonds when the market tested the RBA’s credibility in maintaining the target. The end result would likely be an even flatter yield curve which could lower longer-end borrowing rates and perhaps risk premiums by reinforcing the commitment to keep the cash rate low for an extended period.”

Warren withdraws from the race: Elizabeth Warren is the last candidate to have dropped out of the Democratic nomination race even if she is yet to endorse a nominee. The betting markets are keeping Biden as the frontrunner with the chances of getting the Democrat nomination to run against Trump at around 85% after Super Tuesday’s victory and the support received by Bloomberg after he too pulled out of the race earlier this week. There has also been an improving trend for Democrats to get both the House and Senate in the election day.

GBP keeps rallying: The Pound continues to find further strength as the BoE is not yet fully committed to resort to rate cuts next week, judging by Governor Carney’s comments. He said that the collective response to virus will be powerful and timely with tools including special liquidity and macroprudential measures along with monetary policy instruments, noting that “we still have a lot of ammunition but we have to use space effectively .” Besides, EU’s Barnier reiterated that “there are many serious divergences with the UK on future relationship”, adding “we can get a good agreement for both sides despite 'very, very difficult' differences.”

BoC Poloz keeps door wide open to more cuts: BOC's Poloz made follow up comments after the decision by the Central Bank to cut rates by 50bp earlier this week. He said that he was shifted toward a rate cut regardless of the virus. There was plenty to sink in as part of his remarks, noting that “downside risks were more than enough to offset worries about leverage and financial vulnerabilities”, and that “Canada is headed for at least another quarter of weak GDP and Q2 could be weak as well.” Bottom line, the Central Bank, in Poloz’s words, “remains ready to cut further if necessary.”

Focus will briefly shift to the US NFP numbers: The data will refer to February and consensus looks for a solid print of 175k with unchanged unemployment at 3.6% and wages growth of 3%. These estimates are a subtle downgrade from the previous month. Note, given the extraordinary times we are living with the COVID-19, the US NFP is seen as a secondary indication to change the Fed’s policy path. That said, there are some significant risks that a softer number may help justify further rate cuts by the Fed, while a strong one will likely be dismissed on the basis that the print is yet to reflect the slowdown that the COVID-19 is set to cause.

Nomura’s take on the COVID-19 and Why CB action won’t cut it: In expectations of further coordinated responses by Central Banks, Nomura's economists cautioned that "macroeconomic policies are less well equipped to help (or “can only help so much”). If health security controls fail to contain the spread of COVID-19, financial markets may soon have to accept that a global recession is a forgone conclusion." Nomura predicts that the COVID-19 cases are yet to skyrocket to a projected 1.5 million worldwide.

Oil back under pressure: Oil has also shed its recent gains this week, down more than 2% below $46.00 after news broke out that OPEC members would agree to a 1.5m barrel a day cut conditional to Russia also joining, which is not looking as a high likelihood at this point.

If you found this fundamental summary helpful, just click here to share it!

Recent Economic Indicators & Events Ahead

Source: Forexfactory

If interested in the best ‘free of charge’ News Indicator that can display data on past and future news in the Forex market via MT4, check this YouTube video I produced. The indicator allows you to save time, avoid mistakes. It’s spot on!

Insights Into Forex Flows

The indices show the performance of a particular currency vs G8 FX. An educational video on how to interpret these indices can be found in the Global Prime's Research section. The idea of this analysis is to complement one’s daily bias so that traders can make better and smarter decisions by accounting for the aggregation of flows.

If you found the content in this section valuable, give us a share by just clicking here!

The EUR index regained the upside as the 4-hour chart below shows. The chart is still capped by the 100% projection target but is undeniable that at this stage, it remains very risky to be shorting the Euro as further unwind of carry trades remains a tail risk. Notice, the smart money tracker has also reversed its course back up, shifting the focus to a retest of the previous highs.

The GBP index, on the back of a rebound off a macro level of support after printing a compression off the lows, it finally found a strong pocket of supply by revisiting a key level of resistance where the currency is struggling. While the 4-hour outlook in the GBP chart has turned more positive, this area is definitely a candidate location for the sell-side pressure emanating off the daily chart to return, be aware of that.

The USD index has finally cracked a level of key support which reinforces the bearish bias as the picture continues to deteriorate. The market keeps pricing in further Fed easing, which along with the escape of long carry trade structures makes the USD vulnerable. Bottom line, there is renewed technical evidence that the USD is a sell on strength currency at the moment.

The CAD index keeps selling off on a perfect bearish storm of further unwind of carry trades and a bold move by the BOC to cut rates by 50bp but most importantly, hint at more cuts. The impulsive drop in the currency has now reached what I interpret as oversold conditions, which is what happens when the 100% proj target is met. The validation of the bearish cycle with follow through supply going through the books makes the CAD a sell on strength but note that the position it trades at offers an awful pricing to keep adding shorts unless it corrects higher.

The JPY index, with risk aversion back in vogue, has risen to retest a key level of resistance, which corresponds to the origin of last year’s supply imbalance area. The bias off the 4-hour chart remains bullish and as a result, the safest bet is to keep betting for Yen strength until technicals prove otherwise. Just be aware that the bias doesn’t imply buying Yens off the bat as the level it trades at I consider it to be rather expensive and straight into resistance. Allowing the release of the buy-side pressure towards lower levels will give better entry points.

The AUD index has invalidated its short-term positive dynamics as the market structure returns back to bearish with the positive flow effects off the 100% bearish projection target overwhelmed by the return of the risk averse conditions in the market. There is again re-alignment between the macro and the trend in lower time frames, so the AUD is once again, a solid candidate to project weaker levels in coming sessions.

The NZD index still shows fragility. I made the point yesterday that the NZD remains the most vulnerable currency out of the G8 FX space. My reasoning is that even on the ephemeral return of risk appetite due to Super Tuesday, the currency saw very limited buy-side flows, with the immediate resistance acting as sellers’ strongholds for now. My base case remains, which is, don’t be a hero being long this currency intraday as technicals paint a bleak picture.

The CHF index has shown a greater level of buy side commitment than the Euro this week, as reflected by the fact that the currency broke and held above its 100% bullish proj target. The aggregated flows into the Swiss Franc now show that the index has finally expanded into new highs, what I refer to as a successful bullish rotation. This new buy-side commitment should attract buy on dip strategies in line with the macro/micro trends.

Important Footnotes

- Market structure: Markets evolve in cycles followed by a period of distribution and/or accumulation. To understand the principles applied in the assessment of cycles, refer to the tutorial How To Read Market Structures In Forex

- Horizontal Support/Resistance: Unlike levels of dynamic support or resistance or more subjective measurements such as fibonacci retracements, pivot points, trendlines, or other forms of reactive areas, the horizontal lines of support and resistance are universal concepts used by the majority of market participants. It, therefore, makes the areas the most widely followed and relevant to monitor. The Ultimate Guide To Identify Areas Of High Interest In Any Market

- Fundamentals: It’s important to highlight that the daily market outlook provided in this report is subject to the impact of the fundamental news. Any unexpected news may cause the price to behave erratically in the short term.

- Projection Targets: The usefulness of the 100% projection resides in the symmetry and harmonic relationships of market cycles. By drawing a 100% projection, you can anticipate the area in the chart where some type of pause and potential reversals in price is likely to occur, due to 1. The side in control of the cycle takes profits 2. Counter-trend positions are added by contrarian players 3. These are price points where limit orders are set by market-makers. You can find out more by reading the tutorial on The Magical 100% Fibonacci Projection