tickmill-news

Tickmill Representative

- Messages

- 79

US Treasuries Surge as Yields Reach Critical 5% Level

US Treasuries Surge as Yields Reach Critical 5% Level

In a surprising turn of events, US Treasuries witnessed a sharp rise in demand, driving the 10-Year US yield to a key psychological level of 5%. The sudden surge was not attributed to any specific catalysts, such as new economic data or statements from Federal Reserve officials. Instead, it appears to be a technical pullback, where market participants on both sides recognized the critical importance of the 5% level.

Bill Ackman's comments, suggesting that the US economy might be weaker than it seems, played a role in bolstering the argument for Treasuries. Additionally, according to him, there is a growing sense of key risks accumulating on the downside. Another contributing factor to the Treasuries' rally is the pressure from foreign Treasury holders, who are slowly offloading their holdings, possibly in anticipation of a deterioration in US credit ratings or public finances.

As Treasuries surged, other asset classes responded. The US dollar index dropped to the vicinity of 105.50:

However, the dollar started to recover on Tuesday, causing the EURUSD pair to drift closer to 1.06, while GBPUSD moved to 1.22. USDJPY has been consolidating near the 150 level, a crucial threshold where the Bank of Japan (BoJ) or the Japanese government may initiate interventions to protect the yen.

Gold Corrects Despite Rising Yields

Despite rising yields, gold experienced a correction after nearly touching $2,000 per troy ounce. The price of gold tends to move inversely to yields, as it is a zero-yield asset. However, geopolitical tensions have been the driving force behind gold's rise, and there are no imminent signs that this trend will reverse.

Oil Markets and Currencies

Oil prices are teetering around the $90 mark on Brent, which is considered a significant resistance level. Lower oil prices provide relief for currencies of oil-importing nations, aiding them in their battle against the strong US dollar.

Equity Markets Show Signs of Recovery

US equities and European markets are showing signs of recovery, though gains remain limited to around half a percent. The S&P 500 (SPX) closed yesterday at its lowest level since early June and is currently trading below its 200-day Simple Moving Average (SMA), a key technical support level. This is the second test of the 200-day SMA, indicating that there may not have been enough bullish pressure to initiate a reversal from this critical level.

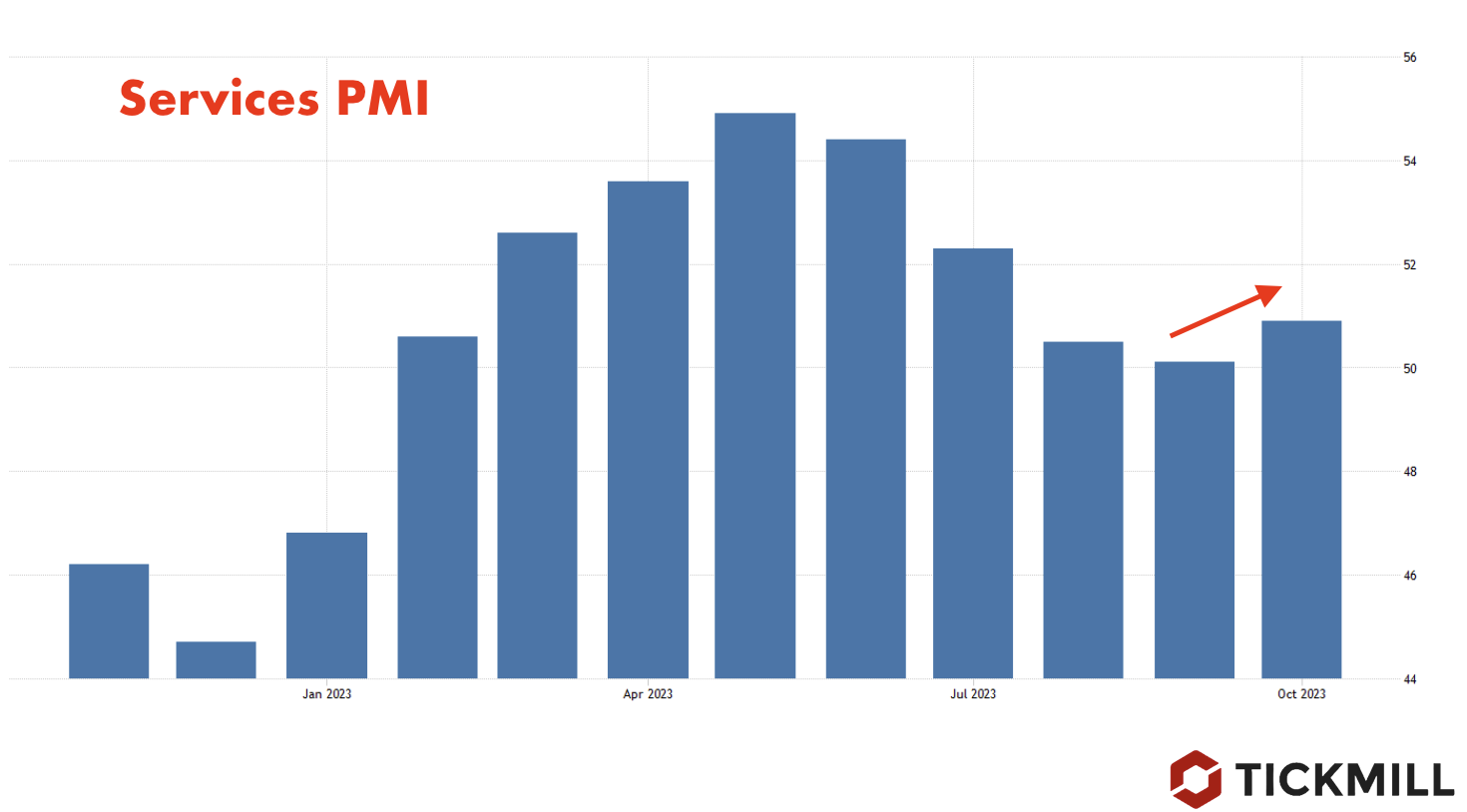

European PMI Indices Disappoint

European economic data added to the day's uncertainty, with German services PMI falling below 50 points to 48, and European services PMI dropping to 47.8, well below the forecast of 48.7 points. These weak data releases seem to coincide with the decline in EURUSD, suggesting that the market may be reacting to the incoming data. The increased risk of stagflation in the European Union creates additional dilemmas for the European Central Bank (ECB), complicating its monetary policy decisions. In PMI data, the 50-point mark divides contraction from expansion.

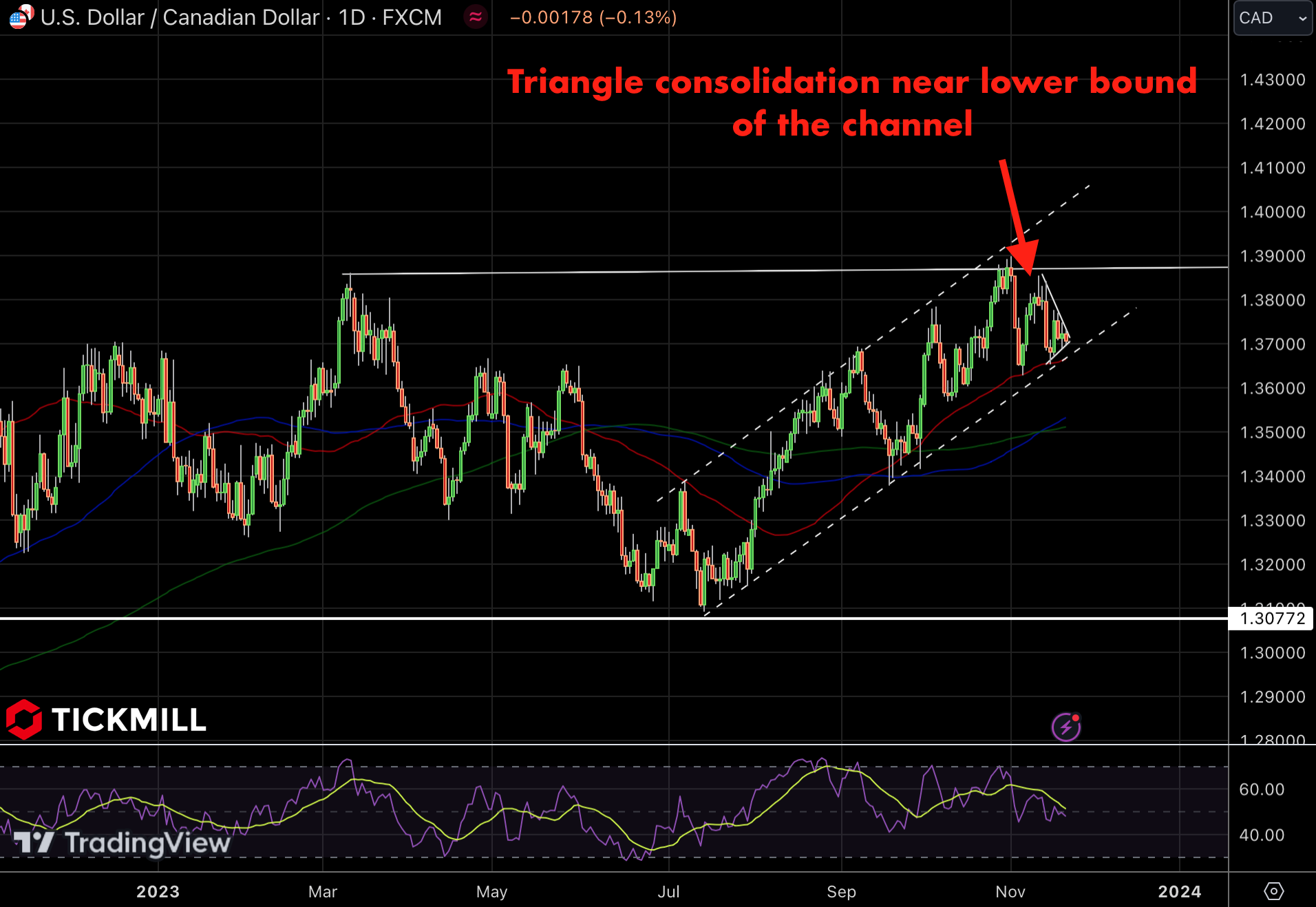

Dollar Index in a Descending Channel

Despite the apparent strength of the US Dollar (DXY), a closer look at the Dollar Index on the daily timeframe reveals a clear descending channel since it reached its high in early October. Considering market sentiment, there is a possibility that the price may gravitate towards the 105 level, where the lower boundary of the channel currently resides:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

US Treasuries Surge as Yields Reach Critical 5% Level

In a surprising turn of events, US Treasuries witnessed a sharp rise in demand, driving the 10-Year US yield to a key psychological level of 5%. The sudden surge was not attributed to any specific catalysts, such as new economic data or statements from Federal Reserve officials. Instead, it appears to be a technical pullback, where market participants on both sides recognized the critical importance of the 5% level.

Bill Ackman's comments, suggesting that the US economy might be weaker than it seems, played a role in bolstering the argument for Treasuries. Additionally, according to him, there is a growing sense of key risks accumulating on the downside. Another contributing factor to the Treasuries' rally is the pressure from foreign Treasury holders, who are slowly offloading their holdings, possibly in anticipation of a deterioration in US credit ratings or public finances.

As Treasuries surged, other asset classes responded. The US dollar index dropped to the vicinity of 105.50:

However, the dollar started to recover on Tuesday, causing the EURUSD pair to drift closer to 1.06, while GBPUSD moved to 1.22. USDJPY has been consolidating near the 150 level, a crucial threshold where the Bank of Japan (BoJ) or the Japanese government may initiate interventions to protect the yen.

Gold Corrects Despite Rising Yields

Despite rising yields, gold experienced a correction after nearly touching $2,000 per troy ounce. The price of gold tends to move inversely to yields, as it is a zero-yield asset. However, geopolitical tensions have been the driving force behind gold's rise, and there are no imminent signs that this trend will reverse.

Oil Markets and Currencies

Oil prices are teetering around the $90 mark on Brent, which is considered a significant resistance level. Lower oil prices provide relief for currencies of oil-importing nations, aiding them in their battle against the strong US dollar.

Equity Markets Show Signs of Recovery

US equities and European markets are showing signs of recovery, though gains remain limited to around half a percent. The S&P 500 (SPX) closed yesterday at its lowest level since early June and is currently trading below its 200-day Simple Moving Average (SMA), a key technical support level. This is the second test of the 200-day SMA, indicating that there may not have been enough bullish pressure to initiate a reversal from this critical level.

European PMI Indices Disappoint

European economic data added to the day's uncertainty, with German services PMI falling below 50 points to 48, and European services PMI dropping to 47.8, well below the forecast of 48.7 points. These weak data releases seem to coincide with the decline in EURUSD, suggesting that the market may be reacting to the incoming data. The increased risk of stagflation in the European Union creates additional dilemmas for the European Central Bank (ECB), complicating its monetary policy decisions. In PMI data, the 50-point mark divides contraction from expansion.

Dollar Index in a Descending Channel

Despite the apparent strength of the US Dollar (DXY), a closer look at the Dollar Index on the daily timeframe reveals a clear descending channel since it reached its high in early October. Considering market sentiment, there is a possibility that the price may gravitate towards the 105 level, where the lower boundary of the channel currently resides:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.