tickmill-news

Tickmill Representative

- Messages

- 79

Currency Shifts, Oil Decline, and Speculative Assets: Analyzing Market Trends and Powell's Impact in the Week Ahead

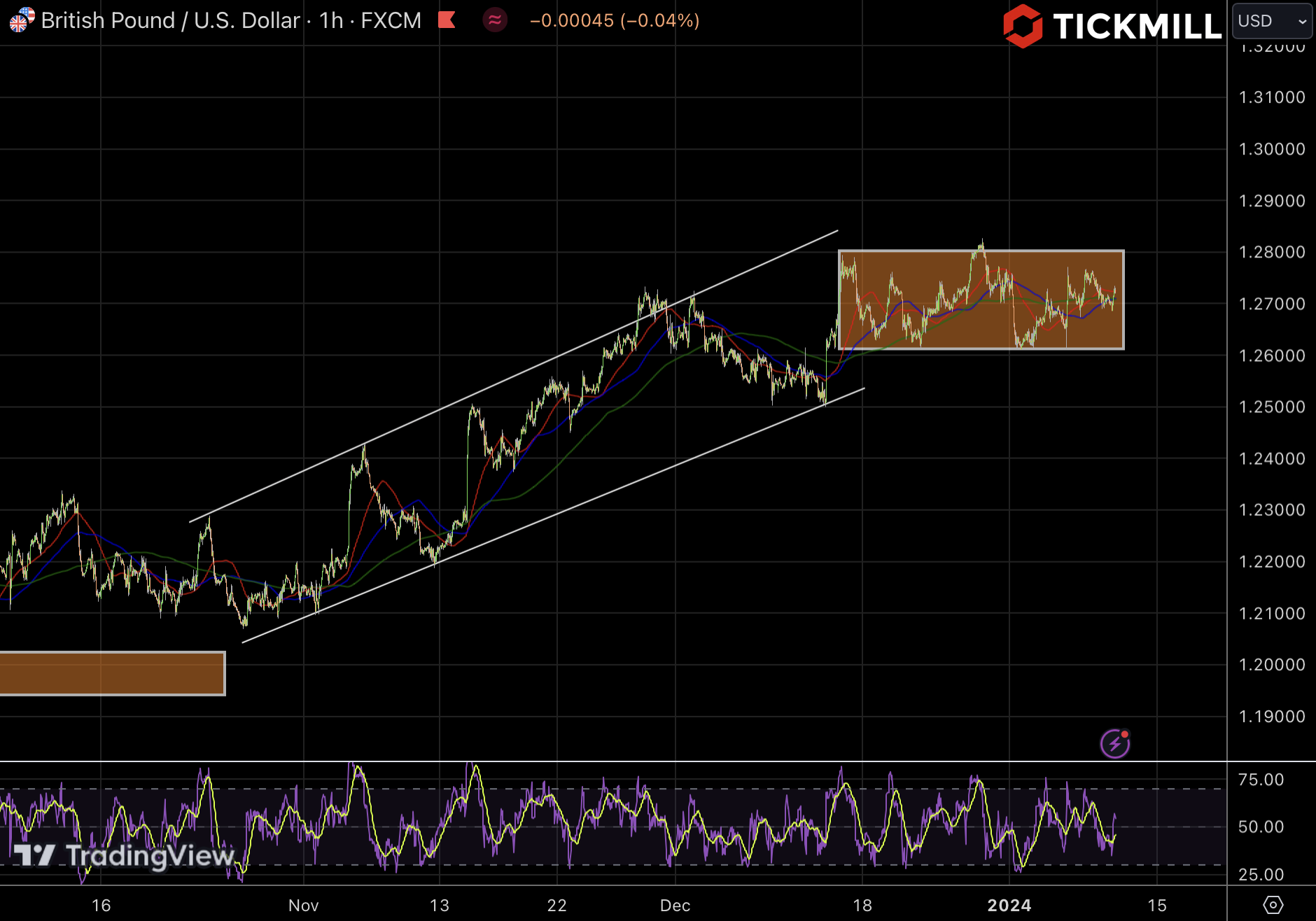

European currencies experienced a continued decline on Monday, with EURUSD finding support around 1.0850, and GBPUSD sliding from its recent peak of 1.27 to 1.2650. Both currency pairs have been consolidating near their local highs since the beginning of last week as the wave of selling the dollar started to taper off. This shift was prompted by changing expectations regarding the actions of the European Central Bank, following the recent EU inflation figures that indicated a significant decrease in price pressures across the bloc. Markets reacted by anticipating similar developments in the UK, putting a halt to the rise of the Pound. Additionally, relatively dovish comments from ECB officials on Friday suggested that, barring inflation shocks, the ECB's tightening cycle may be over, and the central bank could consider policy easing in 2024. The slowdown in EU inflation prevented interest rate differentials from narrowing, which would have favored the European currency. Over the past week, this spread increased by 10 basis points, rising from 1.8% to 1.9%. Interestingly, this spread has largely stayed within a corridor since September, despite the rise in the Euro, raising questions about the sustainability of the European currency rally.

The change in market expectations for short-term real yields in a country, all else being equal, impacts demand for its currency. When it declines, demand drops, and vice versa. However, it's crucial to assess the relative change in yield compared to the real interest rate in a country with similar investment opportunities. This is why the differential between EU and US expected real yields is crucial in evaluating the performance of EURUSD.

On another note, oil prices extended their decline on Monday, partly due to a disappointing OPEC agreement to extend production quotas released last week, indicating potential disagreements among OPEC members on production levels. Additionally, markets may be pricing in a European economic slowdown following unexpectedly dovish inflation figures, which could affect the energy market. From a technical perspective, prices are nearing the mid-November low, and the next support level will be the yearly minimums, particularly for WTI in the range of $68-70 per barrel.

Expectations that interest rates will soon fall have fueled bets on speculative assets like Bitcoin and safe-heaven Gold, which has an inverse relationship with rate expectations. Bitcoin surpassed the $40K resistance without significant resistance from sellers, while gold prices spiked and broke through the $2100 level, reaching an all-time high. Although gold prices later erased intraday gains, they continue to trade near all-time highs around the 2070 level. Remarks from Powell on Friday further supported gold, as he signaled the Fed's increasing confidence that no more rate hikes are needed to combat inflation, but they won't hesitate to act if inflation pressures rise again.

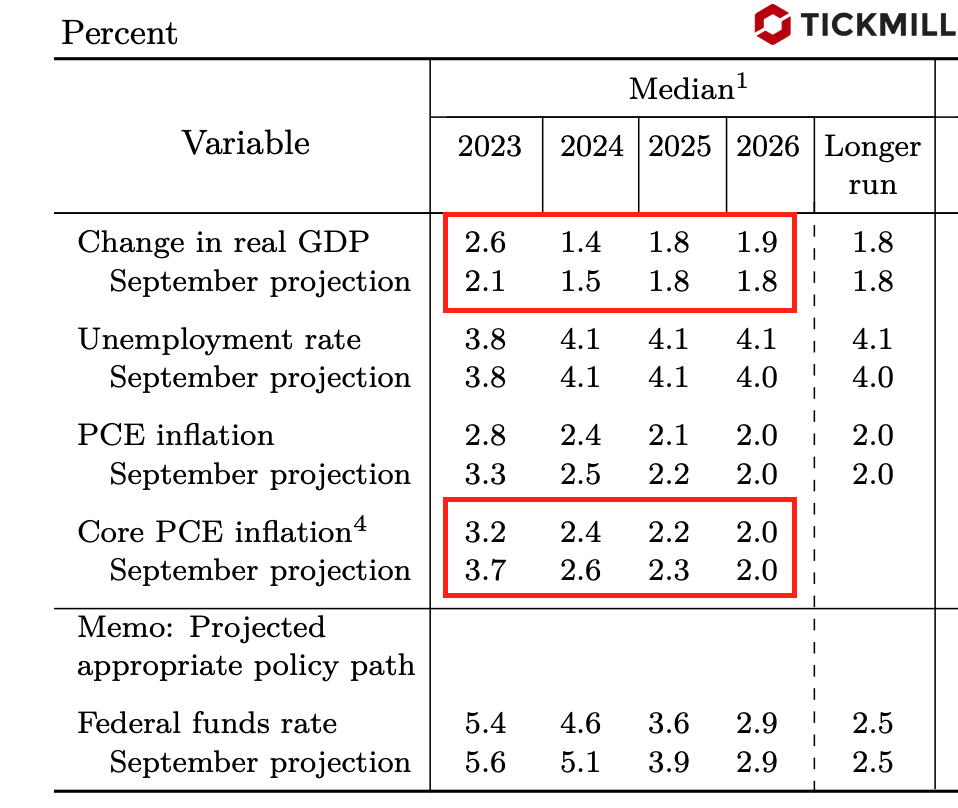

There's a growing consensus in the market that an inflation comeback is unlikely, and global central banks' monetary policies and credit conditions are expected to become softer in 2024. This environment is fertile ground for the rise of assets benefiting from declining investment opportunities and lower bond yields.

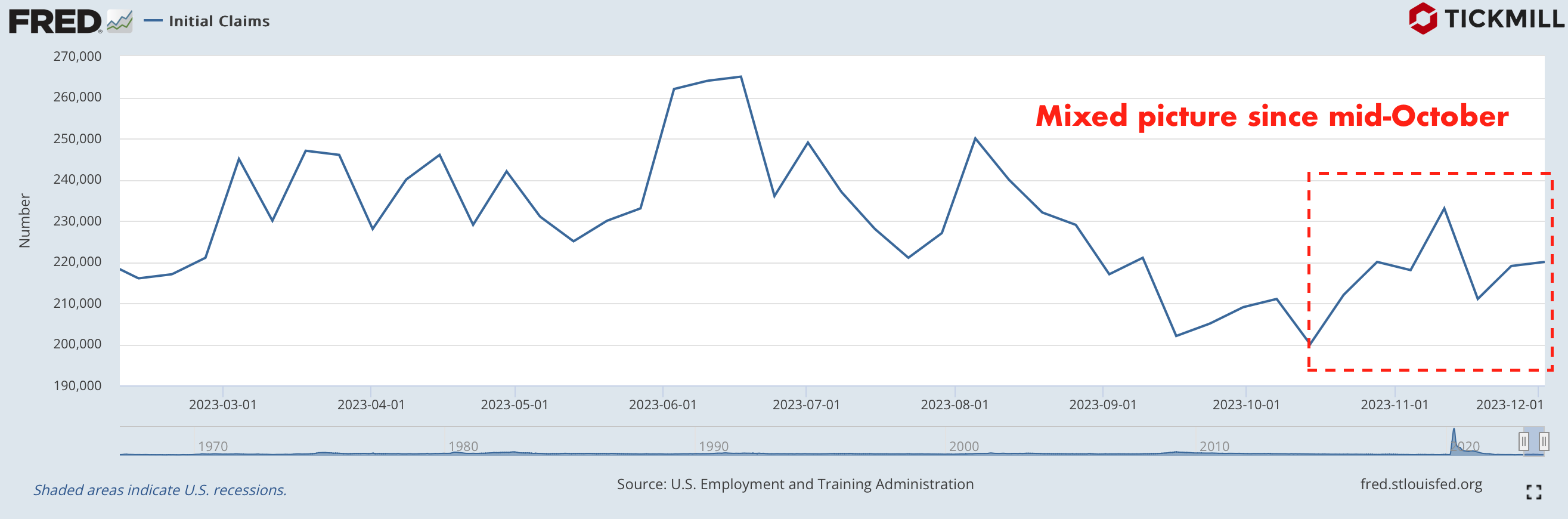

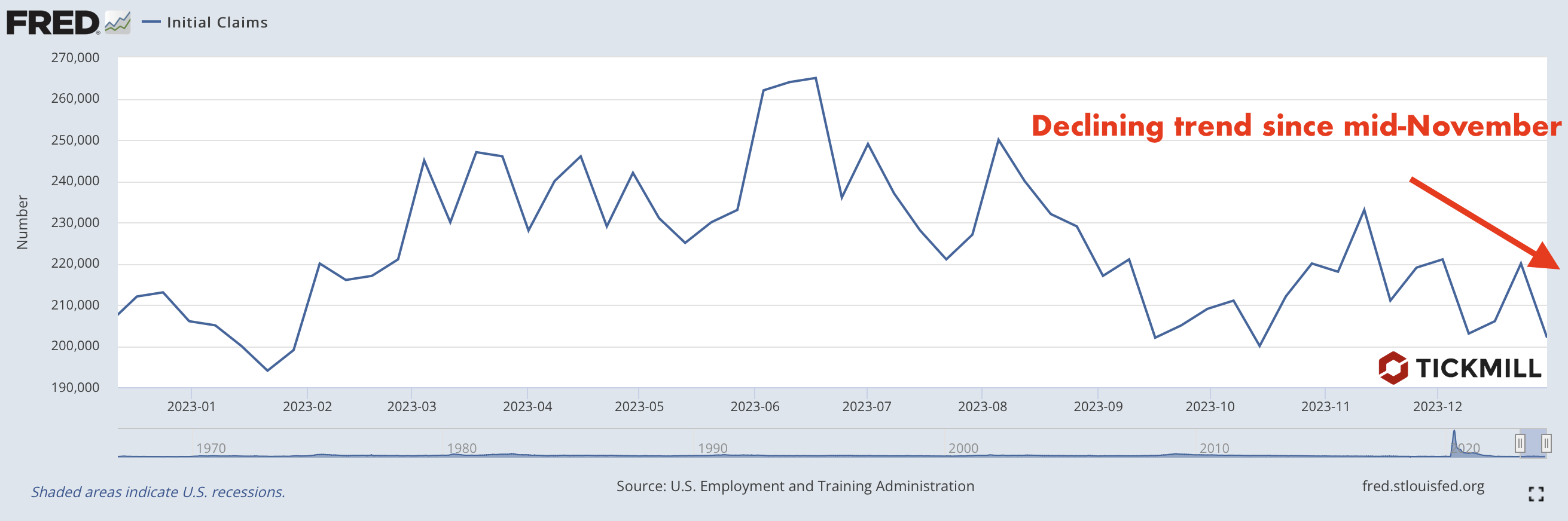

Looking ahead, this week is packed with fundamental data from the US. The market will be closely watching the ADP jobs report, services PMI from ISM, and the official unemployment report from BLS on Friday. The consensus estimate is 180K jobs, and a print near this forecast is expected to have a mildly negative impact on the dollar. A weaker-than-expected report could prompt a resumption of the upside trend in European currencies, with last week's decline seen as a pullback within the overall trend.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

European currencies experienced a continued decline on Monday, with EURUSD finding support around 1.0850, and GBPUSD sliding from its recent peak of 1.27 to 1.2650. Both currency pairs have been consolidating near their local highs since the beginning of last week as the wave of selling the dollar started to taper off. This shift was prompted by changing expectations regarding the actions of the European Central Bank, following the recent EU inflation figures that indicated a significant decrease in price pressures across the bloc. Markets reacted by anticipating similar developments in the UK, putting a halt to the rise of the Pound. Additionally, relatively dovish comments from ECB officials on Friday suggested that, barring inflation shocks, the ECB's tightening cycle may be over, and the central bank could consider policy easing in 2024. The slowdown in EU inflation prevented interest rate differentials from narrowing, which would have favored the European currency. Over the past week, this spread increased by 10 basis points, rising from 1.8% to 1.9%. Interestingly, this spread has largely stayed within a corridor since September, despite the rise in the Euro, raising questions about the sustainability of the European currency rally.

The change in market expectations for short-term real yields in a country, all else being equal, impacts demand for its currency. When it declines, demand drops, and vice versa. However, it's crucial to assess the relative change in yield compared to the real interest rate in a country with similar investment opportunities. This is why the differential between EU and US expected real yields is crucial in evaluating the performance of EURUSD.

On another note, oil prices extended their decline on Monday, partly due to a disappointing OPEC agreement to extend production quotas released last week, indicating potential disagreements among OPEC members on production levels. Additionally, markets may be pricing in a European economic slowdown following unexpectedly dovish inflation figures, which could affect the energy market. From a technical perspective, prices are nearing the mid-November low, and the next support level will be the yearly minimums, particularly for WTI in the range of $68-70 per barrel.

Expectations that interest rates will soon fall have fueled bets on speculative assets like Bitcoin and safe-heaven Gold, which has an inverse relationship with rate expectations. Bitcoin surpassed the $40K resistance without significant resistance from sellers, while gold prices spiked and broke through the $2100 level, reaching an all-time high. Although gold prices later erased intraday gains, they continue to trade near all-time highs around the 2070 level. Remarks from Powell on Friday further supported gold, as he signaled the Fed's increasing confidence that no more rate hikes are needed to combat inflation, but they won't hesitate to act if inflation pressures rise again.

There's a growing consensus in the market that an inflation comeback is unlikely, and global central banks' monetary policies and credit conditions are expected to become softer in 2024. This environment is fertile ground for the rise of assets benefiting from declining investment opportunities and lower bond yields.

Looking ahead, this week is packed with fundamental data from the US. The market will be closely watching the ADP jobs report, services PMI from ISM, and the official unemployment report from BLS on Friday. The consensus estimate is 180K jobs, and a print near this forecast is expected to have a mildly negative impact on the dollar. A weaker-than-expected report could prompt a resumption of the upside trend in European currencies, with last week's decline seen as a pullback within the overall trend.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.