Blockchain and Bitcoin Imperfections

Let's discuss some of blockchain important features and debunk a few myths. At the moment, the dominant view is that the blockchain is a breakthrough, which will change everything in the world.This view is supported by many publications, which emphasize its beneficial features, such as “Blockchain: Blueprint for a New Economy” by Melany Swan, “Blockchain Revolution: How the Technology Behind Bitcoin Is Changing Money, Business, and the World” by Dan and Alex Tapscott, and many others. While we do not object that blockchain technology could be perfected and widely used in the future, not much is said about the limitations of its classic form at least.

In this article, we will discuss classic blockchain technology and bitcoin. New inventions and technologies have emerged that significantly improve the technology overall and eliminate some flaws in the algorithm. This will be the subject of our next meeting. In this article, we will examine seven major features and try to assess the degree to which the widely accepted beliefs about them are true.

Statement #1: The blockchain has P2P architecture. It is decentralized, so it can’t be destroyed.

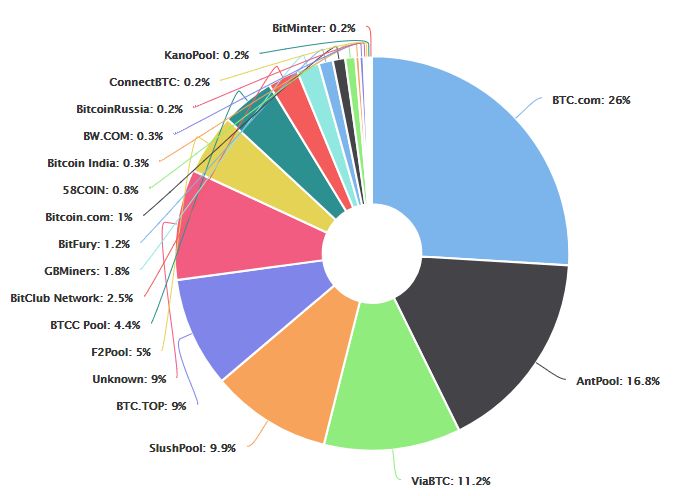

While this statement is true in theory, in reality, the situation is very different. Someone who has access to the necessary resources, such an intelligence agency, could not only take control of the blockchain but also shut it down. This is possible because, at present, miners form pools in order to accumulate enormous calculation power. As we’ve already explained, bitcoins are rewards for creating new blocks in the blockchain. The reward for one block is approximately 12.5 bitcoins. However, this happens very rarely, once in 1000 years or more. Creating pools allows miners to unite their resources and receive small but stable earnings, which are distributed among them.All an intelligence agency would have to do is take control of the mining pools. The four largest pools control more than 60% of the blockchain. We only need to mention the “Attack 51%” risk to support this point. So, if you took control of 4 major servers, you could spend your bitcoins again and again. That’s right, again and again... This not only damages the reputation of bitcoin and blockchain technology, but also limits their value, I suppose.

Source: Blockchain.info

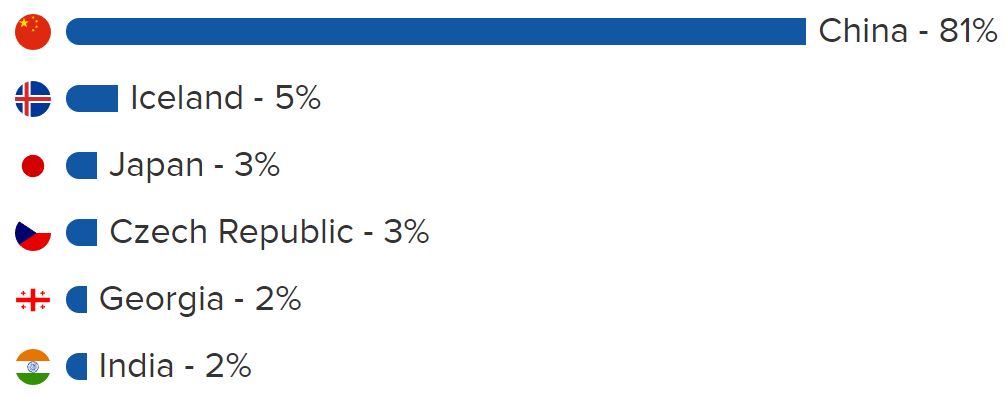

However, the situation is even worse. We have already shown this chart in our first article:

Source: buybitcoinworldwide.com

So, it is even simpler to take under control of 80% of the blockchain in one country, something that a government could do either openly or secretly.

Statement #2: The blockchain has an open structure and all transactions are anonymous. Anonymity is good.

At first glance, this statement is true, until you do your first transaction. In addition, you could recognize the “bad guys” by their intentions. Since the blockchain is open, when you initiate a transaction, your counterparty can gain access to things such as your transaction history (i.e. where you have spent your bitcoins), including the total amount of bitcoins that you have. While this is certainly not pleasant for individuals, imagine how detrimental it could be for companies and corporations if such information were extracted…Even for the “bad guys,” doing transactions on the blockchain is not as smooth as they would like it to be. After they sell drugs or extort money, they could be traced by their wallet number. When they try to exchange bitcoins for cash they could be caught. Besides, the vast majority of trading and exchange transactions from bitcoins to fiat money (dollars, euros) are carried out on exchanges like Bitfinex. All trading accounts require identification (KYC). Bitcoin ATMs also require identification.

Although bitcoin “laundries” do exist – where “dirty” bitcoins are mixed with “clean” ones and washed – this is an expensive service. In addition, you can never know who controls this “laundry.”

So, the transparency of blockchain technology is more a flaw (a big flaw, I would say), rather than an advantage.

Statement #3: The blockchain is infinite; no information can be lost and it lasts forever.

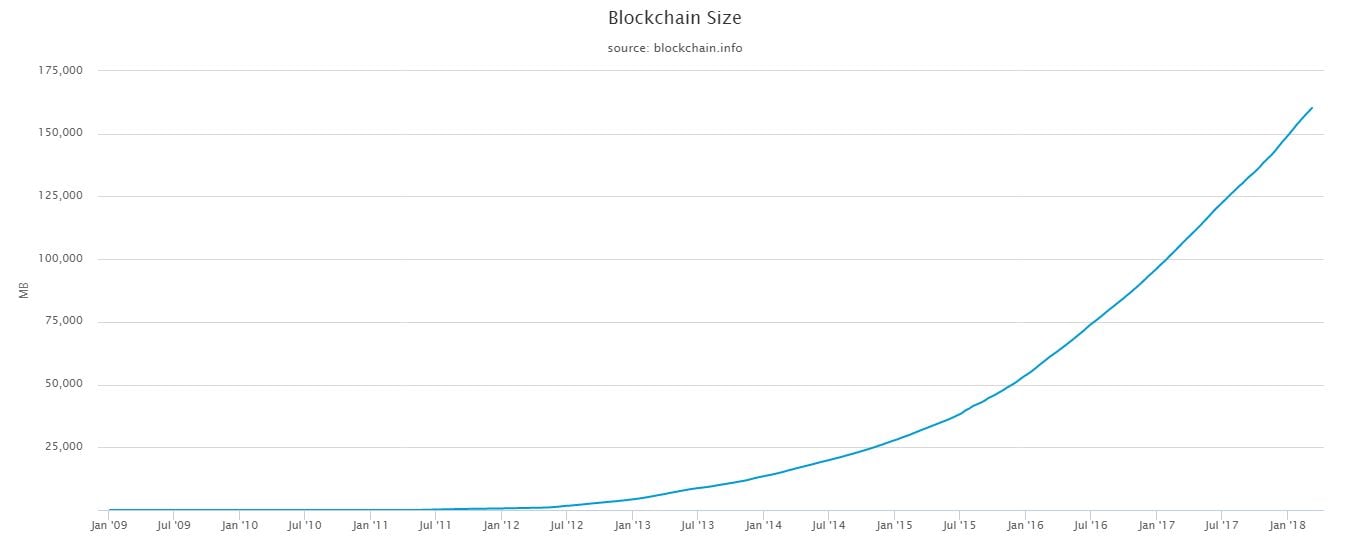

In Statement #2, we discussed how information is kept by all blockchain members. The amount of information is growing, however; it has been growing geometrically in fact, especially in the last two years. The more members appear on the blockchain, the more transactions are made. Hence, more and more storage is required. At present, the entire transaction history is approximately 160 Gb. It’s not that much and, with any luck, you could download it in 2-3 days.Total Blockchain Size.

Source: Blockchain.info

Now, if we look at the idea that the blockchain is “infinite,” it would appear that its growth is limited by hard drive size, unless new technology is invented. Considering the pace of its growth and the size of the modern hard drive, the limit would be reached in 10-15 years, I suppose. But, as we’ve said, size is only one concern. The second concern is the ability to download this information. Have you ever tried downloading 1-2 Tb? Keep in mind that the entire blockchain history would have to be checked beforehand – anyone who attempts this should remember this.

Why would we need to download all that information? What if we simply stored it on a server instead? Yes, this would the solution but, in that case, the blockchain would no longer be decentralized. This is the point when we would have to decide whether we prefer to have the entire history stored on our PCs in order to be a real member of the blockchain, or to use only its features by trusting the wallet and the server.

Statement #4: Bitcoin is revolutionary technology, a breakthrough.

Without doubt, this statement is true, despite that some modules and parts of blockchain technology were known before its invention – mostly the idea of a decentralized system of information transfer. However, the way in which those known algorithms and modules were combined in bitcoin merits respect. It certainly deserves to be called a “breakthrough.”For almost ten years, there was only one serious bug in the code that showed up when an exorbitant number of extra bitcoins appeared in one block – 92 billion more bitcoins than are ever supposed to exist. The problem was remedied by undoing all the financial transactions that took place that day. Other issues, such as the Mt. Gox exchange crash, are not directly related to code. Thus, we acknowledge that, in general, the system is somewhat stable and protected. Our PC’s operational systems are much worse.

As already discussed in the previous article, the primary task for bitcoin and blockchain creators was to invent a system of information transfer outside of a controlled and regulated center where no one knows or trusts each other. The task was accomplished but not very efficiently. Yes, it seems very easy to talk after the fact, but our intention is not to criticize blockchain technology; we agree that it is unique and revolutionary and that it has a tremendous future in various social spheres like logistics, medicine, banking, etc. Our intention here is to cool down some “hotheads,” who are focusing only on its advantages, eager to create sensationalism and revolution, while overlooking some critical issues.

Statement #5: The blockchain is efficient and could be scaled (up)...

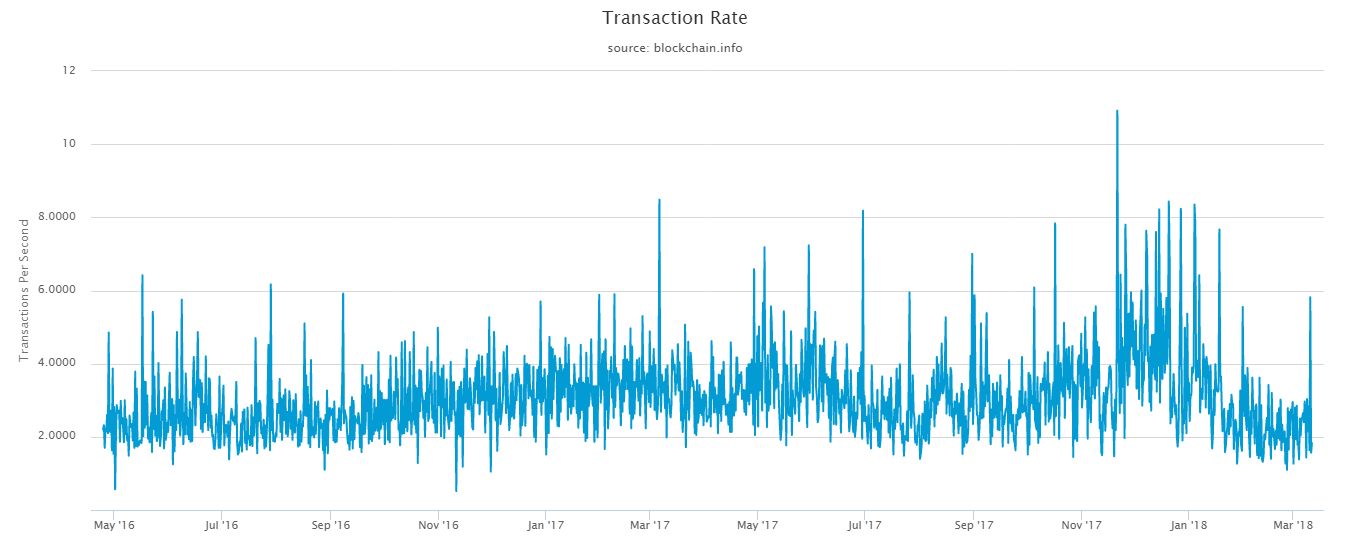

…and we won’t need fiat money anymore. I respond to that with only one question: Since the blockchain is a single-level chain where every computer makes the same calculation, what is the end product of the whole network? It’s safe to assume that it is equal to the result of one computer – not of the entire computer network, just one.Now let’s go a step further: How fast is the blockchain? The answer will surprise you. It is very slow. It can process only 4-5 transactions per second on average.

Blockchain transactions per second.

Source: Blockchain.info

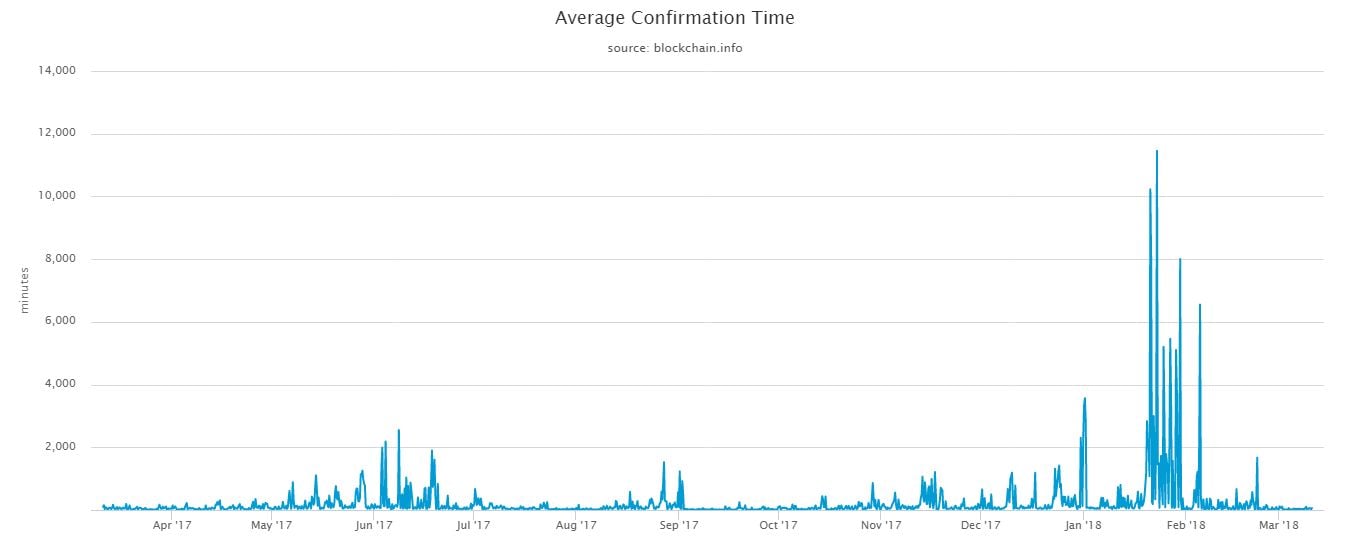

And that’s not all... How long do I need to wait for a confirmation of my transaction? The chart below could shock you, so don’t look if you’re too emotional! The minimum wait time stands at 30 minutes, with an average of 50-60 minutes. Sometimes, it could take as long as 2-3 days!

Blockchain average confirmation time.

Source: Blockchain.info

Visa and Mastercard servers make thousands of transactions per second. If required, they could process them even faster because they can be scaled up. How many people are using the blockchain right now? How many transactions are being carried out each day? The answer is around 200-300K transactions per day, not per minute! And this is globally. Even with this limited usage, the blockchain is already facing serious barriers in terms of transaction speed. Are you prepared to spend at least one hour in a store to buy something? Hardly! Even a 15-minute wait would be exasperating, right?

Statement #6: The blockchain is a giant world supercomputer.

The widely held belief is that the blockchain is a type of Skynet from the movie “Terminator” that unites all computers, distributing very sophisticated tasks proportionally among them for fast calculations, in order to arrive at solutions. We have to disappoint you because this is not so. In fact, we touched on this topic in our first article. Remember that all blockchain members have logs where the same information is stored. This also holds true for every blockchain computer …So, millions of computers around the world (maybe billions now) are making the same transactions on the same algorithms, making logs of the same information, and keeping a record of the entire transaction history since the beginning. What do we see in that? No distribution, no contribution, no cooperation – only copying or multi-doubling. It is not very efficient, right? It is, however, a necessary function.

Statement #7: Miners are a necessary part of the blockchain because they provide the security and stability of its function.

If you’re reading this article, you’ve probably heard about the mysterious “miners.” We will dedicate a separate article to them in near future. For now, we will only say that miners are responsible for creating new blocks in the blockchain, or rather, making “properly-shaped” new blocks to be included in the blockchain. Creating a new block in a chain is the only way to get a bitcoin, which is the reward for creating a new block. All new bitcoins are created by mining.As you may know, a new block appears only once in 10 minutes. There are two reasons for this. First, this is done to guarantee the distribution of just-appeared information about recent blocks among all members. Second, this is the amount of time needed to create a properly shaped block. Only a “proper” new block can be accepted and included in the blockchain. In other words, miners make multiple math iterations with a block in order to get a “proper” shape (a lot of zeros at the beginning of the hash code). To achieve this they require enormous calculation power, so they build massive mining-farms near powerhouses. These mining farms use up enough electricity to power a mid-size town.

Source: slavorum.org

They do only one thing – twist and turn the block, which has yet to be included in the blockchain for 10 minutes, while the history of the most recently completed block is distributed among all members.

So, in reality, if the blockchain had 10, 20, or even 100 times fewer miners, bitcoin transactions would continue to work with the same efficiency. In fact, this was the beginning of bitcoin fever. But since we can’t be 100% sure of the honesty of every miner, large numbers of miners are needed to protect the blockchain from dishonesty. At this point, we can speak about the “Attack 51%” blockchain weakness: In short, if someone accumulated more than 51% of all mining power, they could write an alternative history of transactions (i.e. a new blockchain). This would allow that individual to spend their money twice or more because they could send money in the “current” blockchain, then re-write history and create “new real blockchain” (and cancel old one), where no transaction was made. In other words, the spent bitcoins would be restored in his account.

So we have a circle of despair – the excessive number of miners can’t stop mining because the scenario of the 51% Attack could become a reality. The conclusion here is that the blockchain will be stable as long as it’s relatively easy and profitable to mine bitcoins. If governments started taxing mining or energy became more expensive, the situation could change.

In closing...

We have discussed the most important fallacies about the blockchain and bitcoin. You have probably heard about some of these things before and read some here for the first time. In general, we would say that the advantages of bitcoin (despite that they do not accurately reflect reality) are distributed widely and actively in media for various reasons. Some people are fascinated with this new technology; some do not understand blockchain technology enough to see its flaws; above all, speaking of disadvantages would not benefit for those who understand them and own many bitcoins...Despite some flaws, blockchain technology could be applied to other spheres like logistics, medicine, science, banking, etc. What is more, solid steps are being taken to make improvements and resolve the flaws mentioned here. We will talk about these changes in our next article.