Bitcoin and the Blockchain Are Not So Bad

Let's discuss what should be done to fix those flaws and how blockchain technology has already been improved and made to work more efficiently.First of all, we should emphasize the difference between Bitcoin and the blockchain again. Although many people think that they are the same thing or closely related, in reality, they are two different technologies. According to Satoshi Nakamoto book’s Bitcoin: A Peer-to-Peer Electronic Cash System, bitcoin technology includes many others, such as transactions, hashing, blockchain per se, proof-of-work (PoW), P2P network, members interest, crypto, etc.

Why is this important? Well, it’s important because blockchain technology can also be used for other cryptocurrencies and made to work differently. In other words, the way that blockchain technology is applied to Bitcoin is not the only way. At the same time, it is true that since cryptocurrencies use the proof-of-work algorithm, most features will be used in the same way as they are in Bitcoin. Proof-of-work is a system that prevents the creation of fake blocks and, subsequently, deception in the distribution of rewards among members. In the article “All you need to know about bitcoin and the blockchain,” we explained how new blocks are created by solving math tasks. All these are components of proof-of-work.

Do you recall the key weakness of bitcoin technology? That’s right, speed. It’s too slow. As we’ve already explained, the creation of a new block takes approximately 10 minutes while confirming a transaction can take 40+ minutes. Bitcoin technology does seven transactions per second on average – not per member, seven transactions for all members. PoW means that miners will keep burning electricity and buying new hardware as long as it's profitable to mine Bitcoins. They could use up all the power on the planet, but bitcoin technology won’t work any faster. So, how can this issue be resolved?

The Lightning Network

The Lightning Network is technology that speeds up transactions by not making them not directly on the blockchain but outside it. When a transaction is complete, the blockchain receives only the result, and that piece of information is logged in the block. In other words, members make transactions on separate information channels and send only the results of those transactions to the blockchain. This way, they sidestep the blockchain’s slow speeds.This is how it works: On the Lightning Network, users set up private transaction channels – something like private chats – where they make transactions. To ensure that all parties uphold their obligations, they each make a “pledge” (security deposit) on the blockchain. Then they start their transaction directly, separate from the main blockchain. When the transaction is complete and all sides have confirmed it as true, the private channel closes, the security deposits are withdrawn, and the result of the transaction is made public on the main blockchain.

If someone breaks the rules, the injured party files a complaint with the blockchain, and the offender loses his/her pledge. This simple solution makes it possible to execute millions of transactions per second on the “slow” blockchain.

The blockchain is too transparent

As mentioned in our previous article, it is not easy to keep bitcoin transactions secret. Using several wallets does not help because, the moment a wallet is used, everyone can see that it belongs to you. Also, when you try to change Bitcoins on an exchange, government authorities can identify you through your fiat currency account (USD, EUR, etc.).Last time, we also spoke about mixers that mix clean and “dirty” money from multiple sources, so that it becomes impossible to know where the money is coming from.

Former Darkcoin developers tried building a mixer into their currency’s algorithm, but this was a rather clumsy solution since all the money ended up becoming “grey” and suspicious. Using it in legal transactions was not comfortable since you faced barriers from regulatory authorities.

One example truly private cryptocurrency is Monero, which uses a so-called “ring” technology. According to Getmonero.org, “Monero uses ring signatures, ring confidential transactions, and stealth addresses to obfuscate the origins, amounts, and destinations of all transactions. Monero provides all the benefits of a decentralized cryptocurrency, without any of the typical privacy concessions.”

Simply put, a “ring” is a group of users. Each user has an electronic signature and can sign personal transactions using the name of the group. That way, when a transaction is completed, no one knows who made it.

Monero is untraceable because “sending and receiving addresses as well as transacted amounts are obfuscated by default. Transactions on the Monero blockchain cannot be linked to a particular user or real-world identity.” Also, every Monero wallet has two sets of private and public cryptographic keys, each set being comprised of a “spend key” and a “view key.” This means that, if somebody knows your wallet address, he/she can’t see your balance or any incoming transactions.

Finally, Monero, Bitcoin, and all other cryptocurrencies recommend creating one-off addresses for different senders.

The issue of size

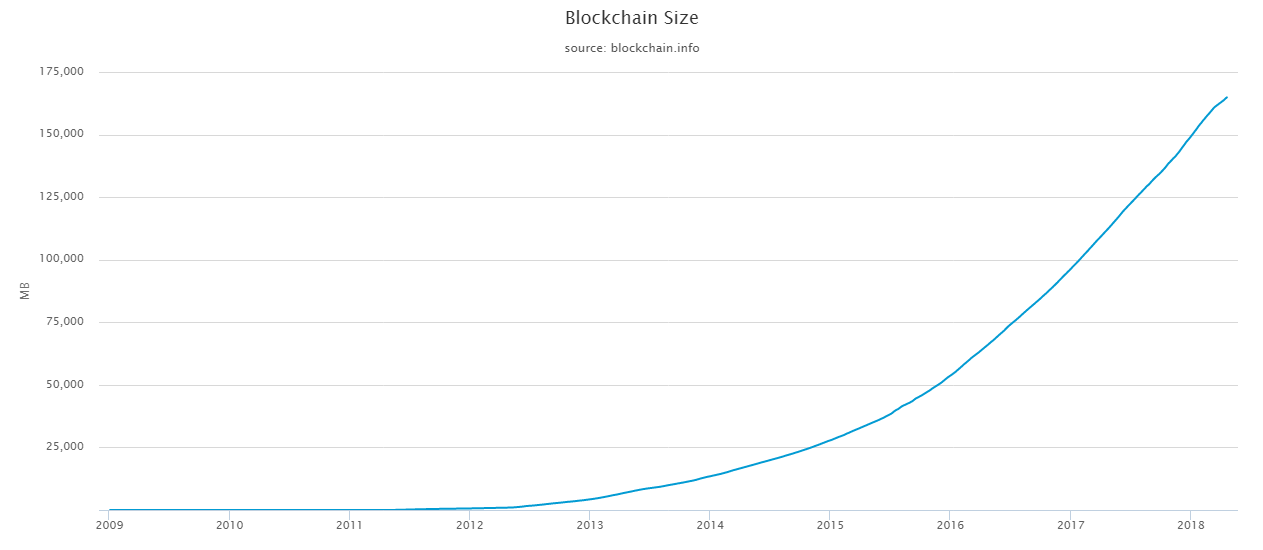

We’ve discussed the issues of speed and privacy, but what about the size of the blockchain? Total Blockchain Size.

Source: Blockchain.info

It’s too big – remember? You need days to download the entire transaction history. Beyond that, the history also has to be checked by the system to make sure it’s correct – this needs a few days more. Take a look at the above chart and try to calculate when it will reach 1-2 Tb. It looks like that will happen rather soon, possibly in a few years. Have you ever tried downloading 2 Tb data from the net, installing, and checking it? The process will likely take weeks. So how can it be made faster and simpler?

To take liberties with the famous Beetles’ song, “All you need is trust; trust is all you need.” As you may recall, it’s necessary to download and keep a log of the entire transaction history because no one trusts anyone. Having each member keep an identical copy of the whole history resolves the issue of trust. But is there a workaround to the problems that that creates?

Yes, if you have some trust, you do not have to download all that data. First of all, there are web wallet and web money services that keep records of the entire blockchain history. If there have been no complaints about a particular web wallet, why mistrust it? These services make money by trusting their clients, and it’s against their interests to make fake transactions because they will lose business.

Using a web Bitcoin wallet allows you to change it without problems because all Bitcoin wallets have logs of the transaction history.

Satoshi Nakamoto proposed another solution with the so-called “light wallets.” You can choose not to download the entire history but only blocks headers (which weight around 50Mb) and those blocks that are relevant to you personally. You can also select a specific point in the history to start downloading from, as opposed to downloading the entire log from the very beginning.

As you can see, a little bit of trust can solve some big problems.

Miners burn planetary resources

Mining uses up enormous resources. “This averages out to a shocking 215 kilowatt-hours (KWh) of juice used by miners for each bitcoin transaction (there are currently about 300,000 transactions per day). Since the average American household consumes 901 KWh per month, each bitcoin transfer represents enough energy to run a comfortable house, and everything in it, for nearly a week. On a larger scale, De Vries' index shows that bitcoin miners worldwide could be using enough electricity to at any given time to power about 2.26 million American homes,” according to the U.S. Energy Information Administration.Sounds staggering, right? The truth is that miners will keep mining as long as it is profitable. Although proof-of-work is the most popular algorithm for protecting the interests of all members of the blockchain, time-consuming calculations are required to create new blocks and to safeguard against illegal changes.

Other algorithms are beginning to appear such as “proof-of-stake” and “proof-of-authority.” Moreover, proof-of-work could be used differently – for instance, by setting tasks that solve problems in the fields of biology, physics, genetics, etc. In other words, this massive processing power and energy could be used in the service of science.

Proof-of-stake does not offer equal chances for the creation of new blocks since the probability depends on the account and the number of coins. In other words, the more coins you have, the more likely that the system will choose you to create a new block. In fact, your chances of creating a new block and receiving a reward are equal to the percentage of the coins that you hold in relation to the total amount of coins. This provides good motivation because the more coins you have, the greater your interest in making the system and network function properly.

Proof-of-authority is a more radical approach. It suggests a “circle of trust” of members who have the right to create new blocks. Those members would have to be approved by the others. What this means, however, is that a network built on proof-of-authority will not be decentralized – this is a significant break from the original concept of the blockchain.

Bitcoin can’t be scaled up

Now we’re coming to more serious problems – Bitcoin can’t be scaled up.First, let’s understand what “scaling up” means. A system or algorithm can be scaled up, if it works more quickly and efficiently when you bring more calculating resources to it, for example, by adding more hardware, faster CPUs, video cards, more computers in the net, etc.

From this standpoint, the blockchain can’t be scaled up; despite the resources you bring to it, it will continue working at the same speed and efficiency.

Different approaches are being considered to address this problem. We have already discussed the Lightning Network; another solution is to make bigger blocks. However, each approach has its own flaws and does not completely solve the problem.

The best scientists are currently working on this problem, and one possible solution might be the so-called “blockchain of blockchains.” As it has been reasonably argued, however, “this raises a conundrum: if every blockchain is on the blockchain, what will that blockchain be on?”

As mentioned in this article, “There must eventually be a final layer to this authentication system, ultimate authority on data validity. For now, this is the bitcoin network’s blockchain, being the one with the most nodes and highest mining difficulty rate. The whole point of hashing to a blockchain is to benefit from its greater security, so we have to use the most secure one available. Bitcoin’s dominance might not last forever, though, due to scalability issues with the protocol. Its blockchain is too large, transaction speeds are too slow, and the fees are too high to be used for anything except currency.

The ultimate blockchain will be one designed entirely for this purpose, a relatively small file intended only to store hash values. Its low resource consumption will make it easy for any device to join the network, and conceivably, almost every device will. It will become the universal judge of truth, capable of resolving any dispute–the blockchain of blockchains.”

Plasma: Scalable autonomous smart contracts

The solution might be found in the so-called “plasma” technology offered by Joseph Poon and Vitalik Buterin, the creator of Ethereum. The technology was created for Ethereum but could also be used for Bitcoin.The idea is similar to the Lightning Network: A member of the root blockchain places a pledge in the root system and creates a private “smaller” blockchain, where he/she is responsible for the accuracy of data and transactions. From time to time, a “smaller blockchain” log is placed in the root system. All members of this smaller blockchain control data propriety and transactions and can lodge a complaint against any party, if something goes wrong.

This system is still in development but, if it becomes fully operational, it could solve the problem of blockchain scalability.

The blockchain is decentralized; it can’t be improved or updated

How is the blockchain updated? Well, either one member forces the others to accept the update, or the update is done silently by the system itself. This is not easy to do with Bitcoin. If one developer has the power to forcibly update the system, then this is not a true P2P network. If the developer has no power to do it, then he/she needs to convince the others to accept the update or improvement. This is a double-edged sword because if the majority of denies the update, the network could split into two incompatible parts. This situation is called a “fork,” which results in two different currencies.A “fork” could happen for different reasons, for example, miners interested in higher rewards for block creation, users wanting to reduce transfer fees, fans wishing to make Bitcoin more popular, others wanting to see new features, and so on.

Forks are already happening both in Bitcoin and Ethereum. That said, Bitcoin members did not agree on block size increase.

How can forks be avoided in the future? The simplest way is for members to vote. For example, the new “Tezos” cryptocurrency algorithm suggests voting as a way of preventing forks. Voting rights are based on the number of coins you hold. If certain members lack the expertise to vote, they can proxy their voting rights to other members – this is called “built-in governance.”

According to Tezos.com, “The Tezos protocol rewards community innovation with an on-chain mechanism, which seamlessly amends the rules governing its protocol and incentivizes protocol development.” That’s why it is based on proof-of-stake, which we mentioned above. “Tezos’ unique proof-of-stake consensus algorithm enables every stakeholder to participate in the validation of transactions on the network.”

The weakness in this solution is that it results in the domination of “fat cats,” which could significantly limit the voting rights of others. Since this would likely hurt the value of the currency, even the “fat cats” would not favor this solution.