tickmill-news

Tickmill Representative

- Messages

- 79

Oil and EURUSD set to rebound next week but it may hide a selling opportunity

The news continues to be full of headlines that discourage risk appetite. Among them – a new all-time high in daily Covid-19 cases in Poland and gloomy forecast for the course of the third wave from the German Ministry of Health without additional restrictions. Nevertheless, risk assets are successfully developing a technical rebound on Friday. Why technical? First, the intraday growth is moderate, not exceeding 1% in the main indices. Secondly, a fairly spoiled news background can be fixed only by a decline in infection rates, which obviously will not happen overnight. The peak of pessimism in this regard has not been reached. Thirdly, the quarterly rebalancing of large funds, during which they will have to reduce the weight of shares in portfolio and increase the share of cheap bonds, has not yet been completed.

The blockage of the Suez Canal counterbalanced the virus story, causing prices to rise. Risk-on in the commodity market then spread to risk assets. But let’s keep in mind that supply chain disruptions are temporary. As soon as the movement in the channel recovers (1-2 weeks), the market will again be absorbed by fears of fragile demand due to the third wave, which will certainly not go anywhere by that time.

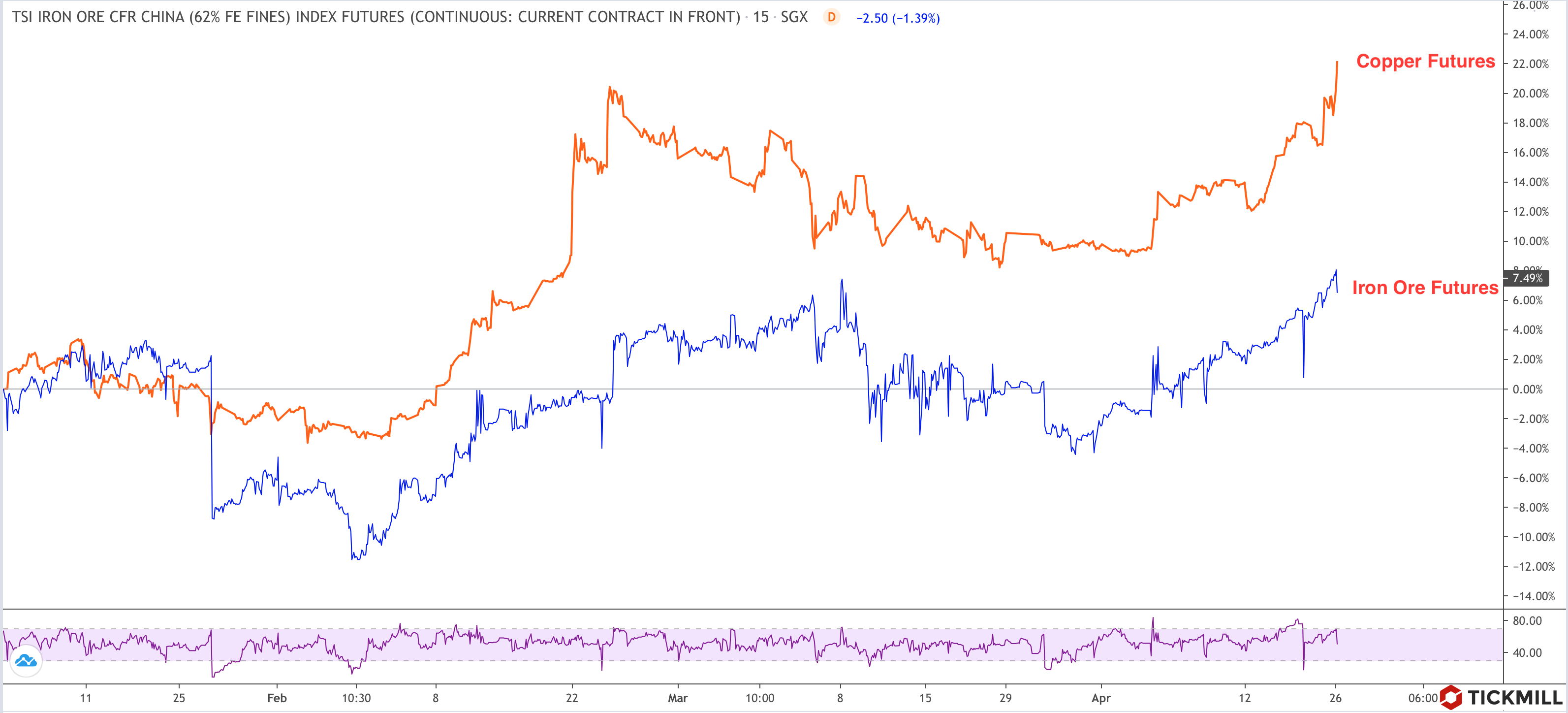

As for the technical picture for oil, a series of recent dips have invalidated the bullish trendline that has been running since November 2020. The breakout has led to a shift in sentiment in the short term, resulting in a short-term bearish channel:

The story with the blocking of the channel increases chances of a short-term rise in oil, however, the main resistance in this rise may be located at around 60.50 (the upper border of the channel). It should be borne in mind that on April 1, OPEC will again decide how to adjust production in response to the deteriorating market conditions. In my opinion, OPEC has already surprised by leaving the restrictions at the same level at the last meeting, so on April 1 there will be disappointment.

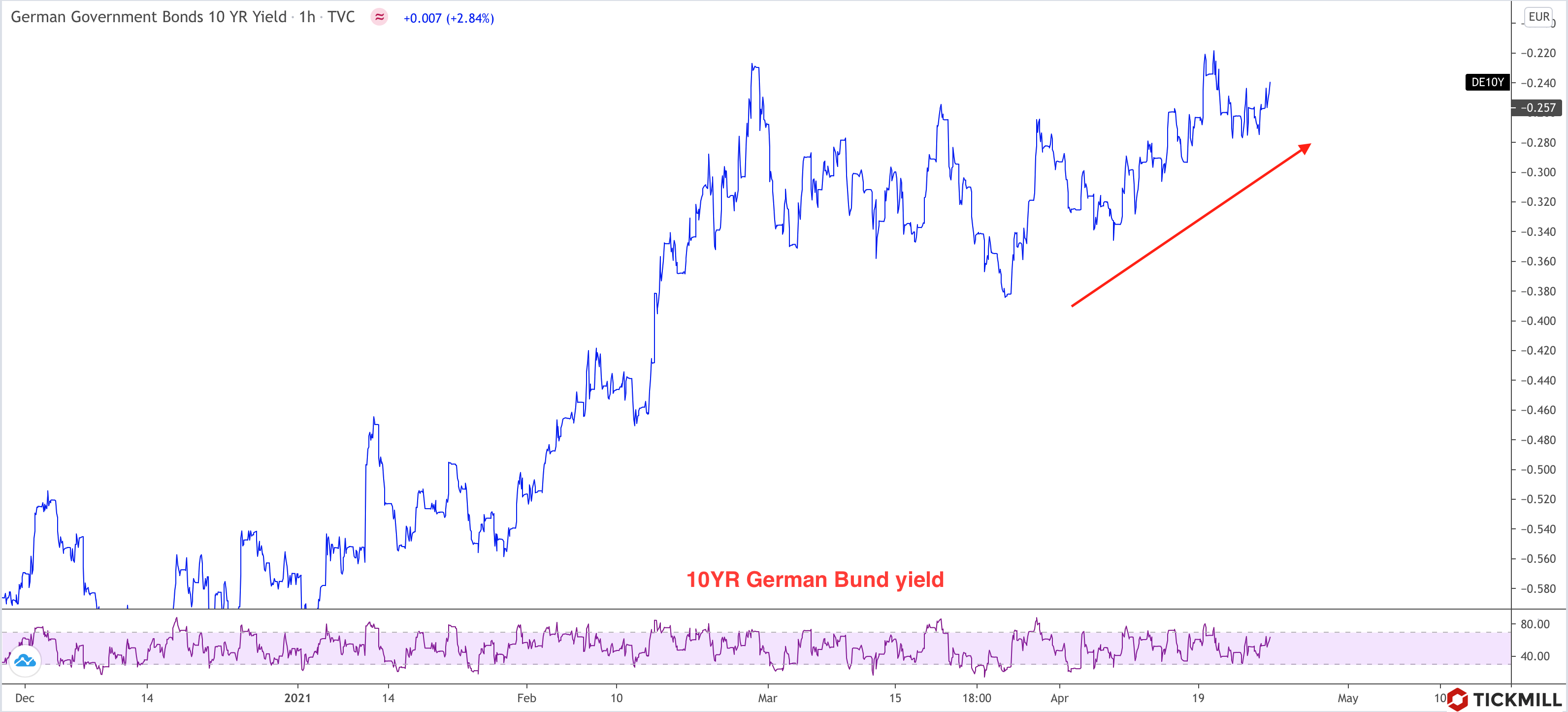

EURUSD has reached the target proposed in yesterday post - the lower border of the current trend corridor. I expect the pair to rise next week to the level of 1.183-1.185 (a repetition of the previous scenario with testing 1.1955), followed by a drop back below 1.18:

The catalysts for the weakening could be data on inflation and the German economy or worsening epi curves or new measures in the EU to contain the virus.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

The news continues to be full of headlines that discourage risk appetite. Among them – a new all-time high in daily Covid-19 cases in Poland and gloomy forecast for the course of the third wave from the German Ministry of Health without additional restrictions. Nevertheless, risk assets are successfully developing a technical rebound on Friday. Why technical? First, the intraday growth is moderate, not exceeding 1% in the main indices. Secondly, a fairly spoiled news background can be fixed only by a decline in infection rates, which obviously will not happen overnight. The peak of pessimism in this regard has not been reached. Thirdly, the quarterly rebalancing of large funds, during which they will have to reduce the weight of shares in portfolio and increase the share of cheap bonds, has not yet been completed.

The blockage of the Suez Canal counterbalanced the virus story, causing prices to rise. Risk-on in the commodity market then spread to risk assets. But let’s keep in mind that supply chain disruptions are temporary. As soon as the movement in the channel recovers (1-2 weeks), the market will again be absorbed by fears of fragile demand due to the third wave, which will certainly not go anywhere by that time.

As for the technical picture for oil, a series of recent dips have invalidated the bullish trendline that has been running since November 2020. The breakout has led to a shift in sentiment in the short term, resulting in a short-term bearish channel:

The story with the blocking of the channel increases chances of a short-term rise in oil, however, the main resistance in this rise may be located at around 60.50 (the upper border of the channel). It should be borne in mind that on April 1, OPEC will again decide how to adjust production in response to the deteriorating market conditions. In my opinion, OPEC has already surprised by leaving the restrictions at the same level at the last meeting, so on April 1 there will be disappointment.

EURUSD has reached the target proposed in yesterday post - the lower border of the current trend corridor. I expect the pair to rise next week to the level of 1.183-1.185 (a repetition of the previous scenario with testing 1.1955), followed by a drop back below 1.18:

The catalysts for the weakening could be data on inflation and the German economy or worsening epi curves or new measures in the EU to contain the virus.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.