Part II. The Power of Interest Rates

Pipruit: Hm, I’ve got that. But why do Central Banks changes interest rates? And when do they decide to increase them or decrease?

Commander in Pips: The point is that the reverse side of interest rates is inflation. This is just like a double edged sword. In fact, an economy stands on the balance between growth and inflation. Inflation is a gradual increase in prices of different goods, services and all material in our world. It comes from gradual growth of the amount of money in the world, while all resources are of limited value. That’s why in “Back to the future” in the 50’s a Coke has cost only 20 cents, while currently around 2 bucks. It’s even not necessary to mention that prior to the 70s there was a gold standard; we’ve discussed it in the history chapter. Although this perspective is a bit hard for many people to believe, the dependence between interest rates, economy growth and inflation is very tight. Moderate inflation comes with economic growth, but too much inflation could harm an economy. That’s why Central Banks always take a close look over commodity prices and some inflation indicators, such as PPI, CPI and PCE indexes.

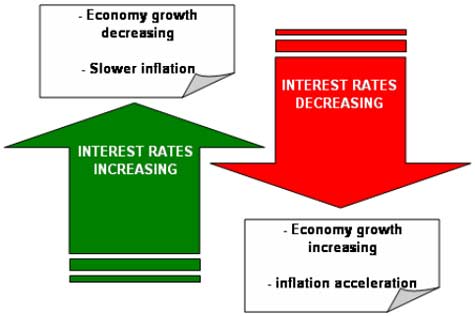

To hold down inflation, a central bank usually starts a so-called tightening policy, when it starts to increase interest rates. This is a long-term process, since a Central Bank also should track the changes in economy growth pace, unemployment, sales etc, and inflation of course. Changes rate a bit – look at what happens. If more is needed, change again, etc.

Pipruit: Ok, I understand that to reduce and hold inflation, a Central Bank has to increase the interest rate, but I do not see logic here. What correlation is there between economic growth, interest rates and inflation?

Commander in Pips: Oh, right. Listen. Imagine that you have your own business. Let’s assume that you produce something, no matter what particularly. When is better to increase your business, when rates are low or high?

Pipruit: Low, I suppose, since to develop any business, to increase production, I need to borrow money to pay operating and capital expenses.

Commander in Pips: Absolutely. So, when interest rates are low, the real economy starts to rise, since every company wants to use this condition to borrow money and invest these funds in growth. Since companies actively start to borrow – this is also good period of times for banks. The public also starts to borrow since low interest makes loans cheap. This leads to capital spending, personal spending, growth of retail, capital sales – to growth in whole economy.

Pipruit: So, that’s excellent! Let it grow! Why should Central Bank interrupt that?

Commander in Pips: This is not so simple. Growth in an economy leads to a significant increase in demand for raw materials and commodities. If demand is growing, then price will grow also. Growth in price on raw materials and commodities increases producers’ operational expenses. Hence it increases the final cost of goods for consumers. Now they can buy less for the same amount of money. That’s inflation.

Pipruit: Cool! And what we have to do then?

Commander in Pips: Well, the Central Bank starts gradually to increase interest rates to chill out an overheated economy. The rate of return of companies (profit margin) on borrowed money gradually becomes less (or even negative) due to growth in interest rates, since their interest expenses become bigger. And to continue investment in growth of company becomes less attractive. It becomes more expensive to borrow more money, so the pace of growth is reduced as is the growth of prices on raw materials and final products. Since rates become high, it’s become more attractive to lend money than to borrow it. To reduce inflation, the Central Bank need to reduce money amount in turnover. Since te Central Bank makes high rates – money start to flow to the Central Bank, because banks buy bonds, the public open deposits, companies stop to borrow etc. So the amount of money in turnover gradually is reduced as is inflation. But it can leads to a chilling and stagnation in the economy – demand for commodities is reduced, industrial production decreases, revenues of companies are reduced also.

Pipruit: So now the Central Bank needs to decrease rates again. Otherwise, there will be a recession…

Commander in Pips: Ok, you see it already. Right. Then the Central Bank starts to decrease interest rates, and all that stuff repeats again. This makes economy moves with cycles.

Pipruit: But why can’t a Central Bank find some equilibrium – such rates that will allow the economy to grow and to not overheat.

Commander in Pips: This happens because a nation’s economy is a big thing, you know…between Central Bank action and the real effect on economy some time passes. So, a Central Bank will see how it impact on economy after some months have passed. So, they will be able to assess their action only after some time. So if the Central bank has overreacted a bit or under-reacted, this will make the economy fluctuate. To neutralize those fluctuations a Central Bank needs to make the opposite action with interest rates. Now imagine how difficult (or even impossible) it is to reach equilibrium, taking into account the time lags between the Central Bank’s action and market reaction to them.

Pipruit: I see…

Pipruit: Ok, I’ve got that, but what is an application to forex market?

Commander in Pips: Hmmm, very simple. Let’s suppose that you have a choice where to invest your money. Say, what do you choose – invest for 1% annually or 3%?

Commander in Pips: That’s right. So interest rates are important, because they dictate the attractiveness of one or another currency, determine world capital flows. Investors among other factors look at interest rates inside some country and decide if they will invest here or not.

Commander in Pips: Well, when investors see that some country has significant interest rates with other factors remain equal (for instance, a AAA rating by S&P), they will invest with that country, since it offers higher yield on their investments. Yield of all other assets, say, bonds will depend on Central Bank interest rates. Later we will also discuss such issues as carry trade that can fully use this possibility. But to buy something, say in Australia – stocks, you need to purchase Australian dollars. Only after that can you invest in stocks, since they denominated in AUD.

When a solid part of world investors decide to invest in Australia due to it’s low budget deficit and high interest rates they start to buy AUD. These purchases lead to solid appreciation of the Australian national currency. The same happens with any other currency, if other risks do not change.

Commander in Pips: For instance, some emerging country could have even higher rates – 8%. But at the same time it could have 3-4 times faster inflation and worse credit quality, say BBB+ compared to AAA. This will not lead to as high of capital flows, since higher rate compensates for the higher risks. That’s why I’ve said “other factors remain equal”.

So, speaking about major currencies we might say that currency with greater interest rates has more chances to appreciate over the currency that has lower interest rate.

Commander in Pips: Oh really? You think you’re so smart and other people like Soros and Buffet are fools, right?

I do not want to upset you but this is not so simple…

Commander in Pips: …the point is that market already includes in the price the current level of interest rates. What really could shake the market is if interest rates are changing or unchanging, and preferably opposed to expectations. For example, if the ECB gradually reduces rates for a long period, then the market anticipates that it will do it in current quarter also. But if ECB will not do it or even will hike rate – that will be opposed to expectation and will change the assessment of currency – its value, perspective and etc. That happens not only with interest rates, but with other macro data, news and other fundamental information.

Since we’ve said that shifting from increasing of interest rates to decreasing and vice versa leads to business cycles in economy - so it works as follows:

Traders do not care much about the current rate, since it already has been priced into the quotes by the market. What they are really interested in – when and how these rates will change. Interest rates, as we said, are one of the major tools of central bank fiscal policy. If some bank reduces interest rate for the long-term it’s no doubt that the moment will come when they will stop doing it first and then shift to rate hiking.

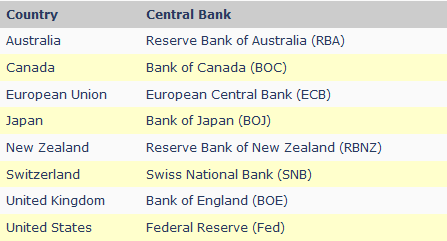

The major source of information here is regular Central Bank meeting report and testimony of the head of the Central Bank. Information comes not only from rate decisions, but mostly from the speech and character of te release – how does the Central Bank assess the current situation in the economy.

When the tone of that speech changes, the market starts to price it in and change the value of the currency, even if rates themselves weren’t yet changed. So the market sentiment starts to change and speculators step in more aggressively. If a Central Bank does something absolutely unexpected then it could lead to huge moves on the market.

Commander in Pips: Excellent question. Here we should start with investigation of rate differential itself. This is just difference between interest rates of two currencies in pair. Then we have to keep an eye on Central Bank monetary policy. The most attractive pairs to trade from the perspective of rate differential are those that show opposite interest rate movements. Say, increasing interest rate policy on one currency and decreasing on another. These pairs could show really huge swings. As example, we can show such pairs as AUD/JPY, AUD/CHF, GBP/JPY and some others. On second place we can appoint pairs, where any interest rate moving happens just with one currency, and most difficult to trade are those pairs where interest rates change in the same direction on both currencies.

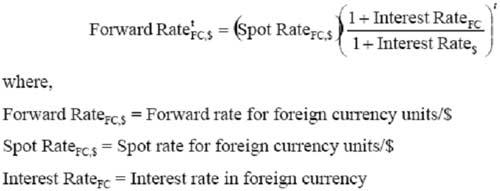

Using following formula, you can calculate future approximate rate of two currencies that have different interest rates:

For instance, if USD rate = 0.25% and EUR = 1% and current rate is 1.43 then when year will pass rate the fair rate should be: 1.43*(1+0.01)/(1+0.0025) = 1.4406

Commander in Pips: Hmmm, very simple. Let’s suppose that you have a choice where to invest your money. Say, what do you choose – invest for 1% annually or 3%?

Pipruit: Of course 3%!

Commander in Pips: That’s right. So interest rates are important, because they dictate the attractiveness of one or another currency, determine world capital flows. Investors among other factors look at interest rates inside some country and decide if they will invest here or not.

Pipruit: I’m still not quite understanding…

Commander in Pips: Well, when investors see that some country has significant interest rates with other factors remain equal (for instance, a AAA rating by S&P), they will invest with that country, since it offers higher yield on their investments. Yield of all other assets, say, bonds will depend on Central Bank interest rates. Later we will also discuss such issues as carry trade that can fully use this possibility. But to buy something, say in Australia – stocks, you need to purchase Australian dollars. Only after that can you invest in stocks, since they denominated in AUD.

When a solid part of world investors decide to invest in Australia due to it’s low budget deficit and high interest rates they start to buy AUD. These purchases lead to solid appreciation of the Australian national currency. The same happens with any other currency, if other risks do not change.

Pipruit: And what other risks are?

Commander in Pips: For instance, some emerging country could have even higher rates – 8%. But at the same time it could have 3-4 times faster inflation and worse credit quality, say BBB+ compared to AAA. This will not lead to as high of capital flows, since higher rate compensates for the higher risks. That’s why I’ve said “other factors remain equal”.

So, speaking about major currencies we might say that currency with greater interest rates has more chances to appreciate over the currency that has lower interest rate.

Pipruit: Well, that’s interesting. So, it should be an easy way to make money – just buy the currency that has higher rate and you will get your profit! Why have we studied all other stuff? You have to start with that point!

Commander in Pips: Oh really? You think you’re so smart and other people like Soros and Buffet are fools, right?

I do not want to upset you but this is not so simple…

Pipruit: I can’t believe it! Any time when we find something simple – it turns like “not so simple”.

Commander in Pips: …the point is that market already includes in the price the current level of interest rates. What really could shake the market is if interest rates are changing or unchanging, and preferably opposed to expectations. For example, if the ECB gradually reduces rates for a long period, then the market anticipates that it will do it in current quarter also. But if ECB will not do it or even will hike rate – that will be opposed to expectation and will change the assessment of currency – its value, perspective and etc. That happens not only with interest rates, but with other macro data, news and other fundamental information.

Since we’ve said that shifting from increasing of interest rates to decreasing and vice versa leads to business cycles in economy - so it works as follows:

Traders do not care much about the current rate, since it already has been priced into the quotes by the market. What they are really interested in – when and how these rates will change. Interest rates, as we said, are one of the major tools of central bank fiscal policy. If some bank reduces interest rate for the long-term it’s no doubt that the moment will come when they will stop doing it first and then shift to rate hiking.

The major source of information here is regular Central Bank meeting report and testimony of the head of the Central Bank. Information comes not only from rate decisions, but mostly from the speech and character of te release – how does the Central Bank assess the current situation in the economy.

When the tone of that speech changes, the market starts to price it in and change the value of the currency, even if rates themselves weren’t yet changed. So the market sentiment starts to change and speculators step in more aggressively. If a Central Bank does something absolutely unexpected then it could lead to huge moves on the market.

Pipruit: Well, that’s great. But, what if rates move in the same direction with some pair, or vice versa – in opposite direction?

Using following formula, you can calculate future approximate rate of two currencies that have different interest rates:

Pipruit: Hm, not impressive appreciation…but, may be we have to buy it?

Commander in Pips: May be, but there are two important issues that appear:

- There is not only interest rates among factors that could influence on the future exchange rate.

- that’s why it is better to choose pairs with greater interest rate difference, say, AUD/JPY if you want to hold position for a long time, since greater interest rate difference (if it will not change, of course) will better compensate for negative surprises from other factors.

Commander in Pips: Also there is such term as “real interest rates”. This is very simple – this is just the interest rate adjusted for inflation:

Real interest rate = nominal interest rate – annual inflation

Some traders think that applying of that formula will give you fairer assessment of rate differential. And they are right. Since a nominal rate could be 25 %, but with inflation of about 20% it will give you just a 5% real yield!

Commander in Pips: Yes, in fact it could.

Commander in Pips: Absolutely the same way as with positive rate. And the last thing to note here… For estimation of future rate based on interest rate differential you do not have to use the 1-day rates that appointed by Central Banks. If you intend to invest in currency pair for, say, 2-years, you may use as a rate the yield of 2-year government bonds, for 5-years – 5-year bonds, and so on:

For instance, 2-year US note yield is 0.2%, while UK 2-year yield is 0.6%. Current GBP/USD rate is 1.65. Hence fair ratio for 2-year investment, if nothing will change, based on rate differential:

1.65*((1+0.006)/(1+0.002))^2 = 1.6632

Commander in Pips: May be, but there are two important issues that appear:

- There is not only interest rates among factors that could influence on the future exchange rate.

- that’s why it is better to choose pairs with greater interest rate difference, say, AUD/JPY if you want to hold position for a long time, since greater interest rate difference (if it will not change, of course) will better compensate for negative surprises from other factors.

Pipruit: I have to remember that.

Commander in Pips: Also there is such term as “real interest rates”. This is very simple – this is just the interest rate adjusted for inflation:

Real interest rate = nominal interest rate – annual inflation

Some traders think that applying of that formula will give you fairer assessment of rate differential. And they are right. Since a nominal rate could be 25 %, but with inflation of about 20% it will give you just a 5% real yield!

Pipruit: Well, but it could lead to negative interest rate!

Commander in Pips: Yes, in fact it could.

Pipruit: And how to deal with that?

Commander in Pips: Absolutely the same way as with positive rate. And the last thing to note here… For estimation of future rate based on interest rate differential you do not have to use the 1-day rates that appointed by Central Banks. If you intend to invest in currency pair for, say, 2-years, you may use as a rate the yield of 2-year government bonds, for 5-years – 5-year bonds, and so on:

For instance, 2-year US note yield is 0.2%, while UK 2-year yield is 0.6%. Current GBP/USD rate is 1.65. Hence fair ratio for 2-year investment, if nothing will change, based on rate differential:

1.65*((1+0.006)/(1+0.002))^2 = 1.6632

Comments

O

One-fm

5 years ago,

Registered user

Good explanation.

Table of Contents

- Introduction

- FOREX - What is it ?

- Why FOREX?

- The structure of the FOREX market

- Trading sessions

- Where does the money come from in FOREX?

- Different types of market analysis

- Chart types

- Support and Resistance

- Candlesticks – what are they?

- Mysterious Fibonacci

- Introduction to Moving Averages

- Bollinger Bands

- Leading and Lagging Indicators

- Basic chart patterns

- Pivot points – description and calculation

- Elliot Wave Theory

- Intro to Harmonic Patterns

- Divergence Intro

- Harmonic Approach to Recognizing a Trend Day

- Intro to Breakouts and Fakeouts

- Again about Fundamental Analysis

- Cross Pair – What the Beast is That?

- Multiple Time Frame Intro

- Market Sentiment and COT report

- Dealing with the News

- Let's Start with Carry

- Let’s Meet with Dollar Index

- Intermarket Analysis - Commodities

- Trading Plan Framework – Common Thoughts

- A Bit More About Personality

- Mechanical Trading System Intro

- Tracking Your Performance

- Risk Management Framework

- A Bit More About Leverage

- Why Do We Need Stop-Loss Orders?

- Scaling of Position

- Intramarket Correlations

- Some Talk About Brokers

- Forex Scam - Money Managers

- Graduation!