Part II. Crosses – Continuation of Discussion...

Pipruit: Is this called “Carry trade” as you’ve once said?

Pipruit: Do you mean that even if the exchange rate will stay stable, my assets will rise?

Commander in Pips: That’s right. As a rule this profit will appear as “swap” in your trading terminal. You may re-read some lessons where we’ve discussed the calculation process (Fundamental analysis chapter 21, Lesson 1 and Chapter 5 Lesson 2, Intermediate Checkpoint) and described what swap is.

Pipruit: Can you give me an example of such a pair?

Commander in Pips: Sure. The most common pair that is traded in such a way is the AUD/JPY pair:

See – here are solid long-term trends, market spends in consolidation very small time. So, imagine that you have long position in AUD/JPY during some trend up. For instance, currently Australian rate is 4.75%, while Japan holds at 0.1%. So, even now it’s big. But that was a time, when it was even bigger – around 6.75% on AUD and almost 0.0% on JPY.

Pipruit: Interestingly, when it was?

Commander in Pips: Approximately in 2002-2007.

Pipruit: Ok, and what kind of appreciation of my assets I could get?

Commander in Pips: Let’s see. I give just approximate calculation and we assume that rates will stay stable all the time.

Let’s take current AUD/JPY rate at 81.23. So, just 1 year holding this long position and you will get:

81.23*(1+0.0475)/(1+0.001) = 85.00

Pipruit: Wow! Not bad appreciation…

Commander in Pips: Yep, and now imagine that you hold position 3-5 years, you have at least 1:20 leverage…

Pipruit: Sir, it looks really significant. Thanks…

Commander in Pips: Well, with pure approach we should calculate it based on real rates (excluding inflation), but even with this approach as it is, we have impressive numbers. A bit later we will return to discussion of this material with more scrutiny.

Crosses are not similar among the crosses

Although we call as a “cross” any currency pair that does not include USD, crosses themselves have some inner classification. For instance such crosses, that contains EUR or JPY are quite common nowadays and have nothing curious for traders. They have relatively solid liquidity, spreads and trading volumes, while other crosses are quite different from them.

Pipruit: What are they?

Commander in Pips: This is really crosses of the crosses (he-he). Such pairs that do not even contain JPY and/or EUR. Can you imagine it?

Pipruit: Well, at least theoretically, for instance GBP/CHF or AUD/NZD.

Commander in Pips: That’s right, but not only this. “Crosses of the crosses” also include some emerging market currencies or small countries currencies that are not very liquid. It could be NOK, DKK, SGD, HKD SEK, TRY and others. Just imagine HKD/TRY cross… Augggchh, habdabs I’ve got the creeps…

Pipruit: Hm and what’s the problem?

Pipruit: Wow, and what we could do?

Commander in Pips: First – don’t trade it. Second, if you still want to trade them, be aware of:

1. Spikes, that you won’t to by stopped out by – place stops farther out;

2. Choppy and sloppy price action – this is the game that is called “try to make good trade”

3. Lack of liquidity – small trading volumes

4. Wide spreads due p.3, that you will have to pay for.

5. Real doom and gloom during macro data releases.

Pipruit: Why we should trade ‘em at all?

Commander in Pips: Nice question, son. Tell me, when you know the answer… Or, wait, I know. We can trade it if we want to have SEK or HKD more than anything else.

Pipruit: That’s not funny…

Additional crosses’ utility

Commander in Pips: Since in previous chapter we’ve spoken about fundamental analysis, let’s discuss how crosses could help us here. The major idea is to extract particular news and trade them purely.

Commander in Pips: Ok, here is some hint to you. Assume that you are waiting for Bank of Australia rate decision. The most common way to trade this news is focus on AUD/USD. Unfortunately there are some data from US expected at the same time. Here you fall into indecision – since your analysis BoA rate decision could be vanquished by unknown data character from US – will they appear to be positive or not? You sure with your expectation about rate, but you absolutely don’t know what data will be from US. What to do?

Commander in Pips: Right, but how?

Commander in Pips: Absolutely. For instance on some crosses, that have some stable information about some currency, or that will not show any data on some currency. For instance the same AUD/JPY, in fact it could be any AUD pair – say, AUD/CHF.

The major idea of this approach is that we do not have to do things the difficult way. Although a trader’s job is itself a hard journey, we have to make short-cuts where we can and make our work simpler where we can. If it will let us make nice trade with lower risk – we must do that. Applying crosses in such a manner allows us to extract specific macro data, news or events and trade them separately to catch the effect only from this particular event or news.

Pairs creating

Commander in Pips: Nice observation, son. You’re absolutely right; this is relatively simple task to do. A pair created in this way is called a “Synthetic Pair”. You have chosen quite an unusual pair…

Commander in Pips: Well, nothing is wrong with it at all. I just want to say that when we do something, we have to know why we do this, right? So, creating synthetic pair is made for a particular property. For example, it could be applied if some specific cross pair does not show necessary trading volumes and liquidity. In that case some large bank or institutional investor could open so-called synthetic position. Let’s say that it wants to sell NZD/CHF pair, since some big corporate clients from New Zealand want to protect their money and invest them in Switzerland. So, this bank is glad to do this, but it shows tight liquidity and it can’t satisfy all the demanded volume from the clients. When speculation is not the target, then it could sell NZD/USD and sell USD/CHF. These are more liquid pairs and as result this bank will get what it wants – short on NZD/CHF.

Additional crosses’ utility

Commander in Pips: Since in previous chapter we’ve spoken about fundamental analysis, let’s discuss how crosses could help us here. The major idea is to extract particular news and trade them purely.

Pipruit: I can't follow what is said.

Commander in Pips: Ok, here is some hint to you. Assume that you are waiting for Bank of Australia rate decision. The most common way to trade this news is focus on AUD/USD. Unfortunately there are some data from US expected at the same time. Here you fall into indecision – since your analysis BoA rate decision could be vanquished by unknown data character from US – will they appear to be positive or not? You sure with your expectation about rate, but you absolutely don’t know what data will be from US. What to do?

Pipruit: Well, you should somehow focus purely on AUD and eliminate impact of USD…

Commander in Pips: Right, but how?

Pipruit: Ok, I’ve got your clue – we should focus on some cross pair. In this case we will not care about US data at all.

Commander in Pips: Absolutely. For instance on some crosses, that have some stable information about some currency, or that will not show any data on some currency. For instance the same AUD/JPY, in fact it could be any AUD pair – say, AUD/CHF.

The major idea of this approach is that we do not have to do things the difficult way. Although a trader’s job is itself a hard journey, we have to make short-cuts where we can and make our work simpler where we can. If it will let us make nice trade with lower risk – we must do that. Applying crosses in such a manner allows us to extract specific macro data, news or events and trade them separately to catch the effect only from this particular event or news.

Pairs creating

Pipruit: Sir, looks like some idea has appeared, but I’m not sure. Now I’m looking in may trading software and see such pairs as USD/DKK (Danish Krone) and USD/SGD (Singaporean Dollar), but do not see, for instance DKK/SGD. But I suspect that somehow I can create this position artifically, but I still can’t catch it.

Commander in Pips: Nice observation, son. You’re absolutely right; this is relatively simple task to do. A pair created in this way is called a “Synthetic Pair”. You have chosen quite an unusual pair…

Pipruit: And what is wrong with it?

Commander in Pips: Well, nothing is wrong with it at all. I just want to say that when we do something, we have to know why we do this, right? So, creating synthetic pair is made for a particular property. For example, it could be applied if some specific cross pair does not show necessary trading volumes and liquidity. In that case some large bank or institutional investor could open so-called synthetic position. Let’s say that it wants to sell NZD/CHF pair, since some big corporate clients from New Zealand want to protect their money and invest them in Switzerland. So, this bank is glad to do this, but it shows tight liquidity and it can’t satisfy all the demanded volume from the clients. When speculation is not the target, then it could sell NZD/USD and sell USD/CHF. These are more liquid pairs and as result this bank will get what it wants – short on NZD/CHF.

Pipruit: I see. Well, I do not have any purpose and was just watching my trading software when this idea has come, that’s all.

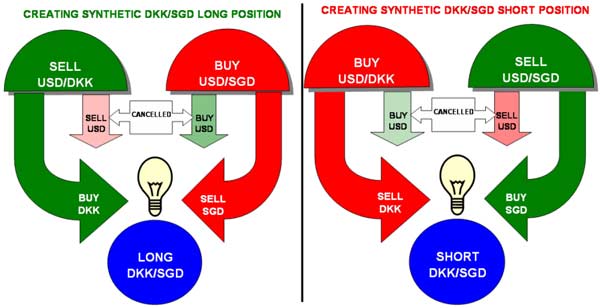

Commander in Pips: All right, let’s describe the process of creating synthetic pair on your example:

Suppose we need Long “Y/Z” pair, but we have “X/Y” and “X/Z”, what we can do?

Commander in Pips: Well, that’s simple – we need Sell X/Y and Buy X/Z. Other words, we Sell X and buy Y and then Buy X and sell Z.

Commander in Pips: Ok, let’s start from the end. Think about synthetic pair first – you need Long position in DKK/SGD, so what does it mean?

Commander in Pips: Right. To have long in DKK what you have to do with USD/DKK?

Commander in Pips: Ok, and to have short in SGD, what you have to do with USD/SGD?

Commander in Pips: See? Nothing difficult is needed to create a synthetic pair. Still there is another question that appears – position size adoption.

Commander in Pips: When you trade USD/DKK, you trade it in terms of USD lots, so it will be 100,000 USD, that you will sell for DKK. But if the rate is 5.2811 you will get 5.2811* 100,000 = 528,110 DKK.

When you will buy USD/SGD, you will get SGD at 1.2083 rate or 120,830 SGD. The question is – how much DKK do you want to have.

IF you don’t care and equivalent of 100,000 USD is acceptable – no problem, just make it with 1.0 common lot. But what if you want, say 1.0 lot particularly DKK or 100,000 DKK. In this case you need to take just 0.2 lot in first trade – then you will get 105,622 DKK. That is close to single lot.

Commander in Pips: All right, let’s describe the process of creating synthetic pair on your example:

Suppose we need Long “Y/Z” pair, but we have “X/Y” and “X/Z”, what we can do?

Pipruit: ???

Commander in Pips: Well, that’s simple – we need Sell X/Y and Buy X/Z. Other words, we Sell X and buy Y and then Buy X and sell Z.

Pipruit: Commander, please stop…

Commander in Pips: Ok, let’s start from the end. Think about synthetic pair first – you need Long position in DKK/SGD, so what does it mean?

Pipruit: It means that I want to buy DKK for SGD – to have Long position in DKK and short in SGD.

Commander in Pips: Right. To have long in DKK what you have to do with USD/DKK?

Pipruit: Sell it – sell USD and buy DKK.

Pipruit: Buy it – buy USD and sell SGD. Hey! It works…

Commander in Pips: See? Nothing difficult is needed to create a synthetic pair. Still there is another question that appears – position size adoption.

Pipruit: What do you mean?

Commander in Pips: When you trade USD/DKK, you trade it in terms of USD lots, so it will be 100,000 USD, that you will sell for DKK. But if the rate is 5.2811 you will get 5.2811* 100,000 = 528,110 DKK.

When you will buy USD/SGD, you will get SGD at 1.2083 rate or 120,830 SGD. The question is – how much DKK do you want to have.

IF you don’t care and equivalent of 100,000 USD is acceptable – no problem, just make it with 1.0 common lot. But what if you want, say 1.0 lot particularly DKK or 100,000 DKK. In this case you need to take just 0.2 lot in first trade – then you will get 105,622 DKK. That is close to single lot.

Pipruit: Cool! That’s important.

Commander in Pips: Also do not forget about bid/ask spread, since the difference could be significant if the position value will be really big.

Another application of synthetic pair is arbitrage trades, but they are not reachable for us due to bid/ask spreads that we have to pay on both legs of cross. In our example legs are USD/DKK and USD/SGD. But in general, if you see that synthetic rate of DKK/SGD is different from common spot DKK/SGD, you can make some action:

1. IF synthetic rate > spot rate – “Sell Synthetic and buy Spot.

2. IF synthetic rate < spot rate – “Buy Synthetic and Sell Spot.

These will be arbitrage or risk-free trades, since it makes money on market mispricing. You have no risk, since you buy and sell the same pair. Unfortunately such kind of transactions are possible mostly by electronic trading systems (as trading robots – special programs, that track the market for such mispricing and make trades) and for those who pays no bid/ask spread, or this spread very tight. Usually this is big banks and institutional investors.

Another disadvantage with trading synthetic pairs is greater expenditures. Since you will have two legs you will have to pay double bid/ask spread, second – you will need approximately two times greater initial margin.

So, dealing just with cross pair will be cheaper and easier. Once you see that this cross is trading with your broker – better to deal with cross. Leave synthetic pairs till the moment when you will become a real whale of Forex.

Commander in Pips: Also do not forget about bid/ask spread, since the difference could be significant if the position value will be really big.

Another application of synthetic pair is arbitrage trades, but they are not reachable for us due to bid/ask spreads that we have to pay on both legs of cross. In our example legs are USD/DKK and USD/SGD. But in general, if you see that synthetic rate of DKK/SGD is different from common spot DKK/SGD, you can make some action:

1. IF synthetic rate > spot rate – “Sell Synthetic and buy Spot.

Buy USD/DKK + Sell USD/SGD + Buy DKK/USD;

2. IF synthetic rate < spot rate – “Buy Synthetic and Sell Spot.

Sell USD/DKK + Buy USD/SGD + Sell DKK/USD;

These will be arbitrage or risk-free trades, since it makes money on market mispricing. You have no risk, since you buy and sell the same pair. Unfortunately such kind of transactions are possible mostly by electronic trading systems (as trading robots – special programs, that track the market for such mispricing and make trades) and for those who pays no bid/ask spread, or this spread very tight. Usually this is big banks and institutional investors.

Another disadvantage with trading synthetic pairs is greater expenditures. Since you will have two legs you will have to pay double bid/ask spread, second – you will need approximately two times greater initial margin.

So, dealing just with cross pair will be cheaper and easier. Once you see that this cross is trading with your broker – better to deal with cross. Leave synthetic pairs till the moment when you will become a real whale of Forex.

Comments

D

deadducks

12 years ago,

Registered user

I need some clarification on the following:

Commander in Pips: Well, nothing is wrong with it at all. I just want to say that when we do something, we have to know why we do this, right? So, creating synthetic pair is made for a particular property. For example, it could be applied if some specific cross pair does not show necessary trading volumes and liquidity. In that case some large bank or institutional investor could open so-called synthetic position. Let’s say that it wants to buy NZD/CHF pair, since some big corporate clients from New Zealand want to protect their money and invest them in Switzerland. So, this bank is glad to do this, but it shows tight liquidity and it can’t satisfy all the demanded volume from the clients. When speculation is not the target, then it could sell NZD/USD and buy USD/CHF. These are more liquid pairs and as result this bank will get what it wants – NZD/CHF.

Shouldn't that be Buy NZD/USD and Buy USD/CHF to result in a Buy of NZD/CHF?

Eric

Commander in Pips: Well, nothing is wrong with it at all. I just want to say that when we do something, we have to know why we do this, right? So, creating synthetic pair is made for a particular property. For example, it could be applied if some specific cross pair does not show necessary trading volumes and liquidity. In that case some large bank or institutional investor could open so-called synthetic position. Let’s say that it wants to buy NZD/CHF pair, since some big corporate clients from New Zealand want to protect their money and invest them in Switzerland. So, this bank is glad to do this, but it shows tight liquidity and it can’t satisfy all the demanded volume from the clients. When speculation is not the target, then it could sell NZD/USD and buy USD/CHF. These are more liquid pairs and as result this bank will get what it wants – NZD/CHF.

Shouldn't that be Buy NZD/USD and Buy USD/CHF to result in a Buy of NZD/CHF?

Eric

Sive Morten

12 years ago,

Registered user

Thanks, Eric we will fix it.

Actually here is mostly another mistake - it should be "sell NZD/CHF", since NZ company wants to invest in Swiss economy. Hence there will be "Sell NZD/USD and sell USD/CHF".

Thank you anyway.

Actually here is mostly another mistake - it should be "sell NZD/CHF", since NZ company wants to invest in Swiss economy. Hence there will be "Sell NZD/USD and sell USD/CHF".

Thank you anyway.

AsstModerator

12 years ago,

Registered user

Fixed, I think.

Table of Contents

- Introduction

- FOREX - What is it ?

- Why FOREX?

- The structure of the FOREX market

- Trading sessions

- Where does the money come from in FOREX?

- Different types of market analysis

- Chart types

- Support and Resistance

- Candlesticks – what are they?

- Mysterious Fibonacci

- Introduction to Moving Averages

- Bollinger Bands

- Leading and Lagging Indicators

- Basic chart patterns

- Pivot points – description and calculation

- Elliot Wave Theory

- Intro to Harmonic Patterns

- Divergence Intro

- Harmonic Approach to Recognizing a Trend Day

- Intro to Breakouts and Fakeouts

- Again about Fundamental Analysis

- Cross Pair – What the Beast is That?

- Multiple Time Frame Intro

- Market Sentiment and COT report

- Dealing with the News

- Let's Start with Carry

- Let’s Meet with Dollar Index

- Intermarket Analysis - Commodities

- Trading Plan Framework – Common Thoughts

- A Bit More About Personality

- Mechanical Trading System Intro

- Tracking Your Performance

- Risk Management Framework

- A Bit More About Leverage

- Why Do We Need Stop-Loss Orders?

- Scaling of Position

- Intramarket Correlations

- Some Talk About Brokers

- Forex Scam - Money Managers

- Graduation!