Part I. Let's Start with Carry

In general, the idea of carry is very simple. This term just points to the difference in interest rates and profits that comes from this difference. We already know that different countries have different interest rates on their currencies at different times, depending on whether their economy contracting or expanding. This imbalance between rates on different currencies lets traders (mostly big financial institutions) extract this profit that comes from the rate difference.

Pipruit: Yes, I remember that. Once we’ve said that rate difference could give profit/loss even if the exchange rate will not change at all. This difference appears since any transaction on the Forex market (if you avoid delivery and hold position open) forces you to do something like to borrow one currency and loan out the other. Say, if I go long in EUR/USD, (hold position for significant time and do not make a delivery or close it) then I borrow USD and loan EUR, because I have to deliver USD and the counterparty owes me to deliver EUR, hence I give them a loan in EUR, while they have given me loan in USD. Since the rates on EUR and USD are different – carry appears. We’ve spoken about it one…

Commander in Pips: Perfect! You’ve really surprised me… So, for those who intend to dive into carry positions, there are two issues are preferable to see:

- As low volatility as it could be – if rate will not change at all – all the better;

- As large difference in rate as it possible.

That is the dream of traders who intend to enter carry trade.

Commander in Pips: Well, concerning about 5% annually – this is without leverage. Add here 20 times leverage and you will double your account… But this will only happen if you will use the total value of your account as a margin. Nevertheless, even 50% profit from carry trade is not bad, right?

Now about the second – don’t be too hasty. We will discuss this topic and how to involve it in day-by-day operations.

Carry Structure

Although you’ve explained me this topic pretty well, I think that we can spend some time and make fast repeat of that. Let’s choose some pairs with significant different in rates… What do you offer?

Commander in Pips: All right let’s take AUD/USD. AUD rate now is 4.5% while USD rate is 0.25%. Hence, carry rate will be 4.50-0.25 = 4.25% - not bad ha - greater than what you can get on 10 year US Treasuries bonds.

Still, on the bond you have to wait for a maturity date – this is a long time, while on forex this difference is deposited or withdrawn from your account balance daily. That’s another small positive splash of the forex market. This transaction is made by your broker.

Commander in Pips: You don’t understand. Your broker deposits or withdraws the sum of carry just for passing a single day. If you will hold position for one more day –he will do this again by close, and so on. Carry result (positive or negative) accumulates on your account day by day. When you will finally close your position – you will get the carry accurately for the term that you’ve held it open.

Commander in Pips: Because it depends on direction of your position, since as you’ve said early, carry could be positive or negative. The first case will lead to deposit while the second to withdrawal. Technically it happens as follows:

If you hold your position overnight, broker makes its so-called “roll over” – closes it and opens at the same quote. All spot forex positions close by the end of the day. This “day” term is a bit blurry and depends on your broker. Each broker has its own “closing day time”, but as a rule this time coincides with 0:00 of local time or some major time zone. Your broker closes your position and reopens again at the same quote, so you do not even see it. At the same moment it deposits or withdraws the carry cost for the past day. So this transaction of closing and reopening calls “Roll over”.

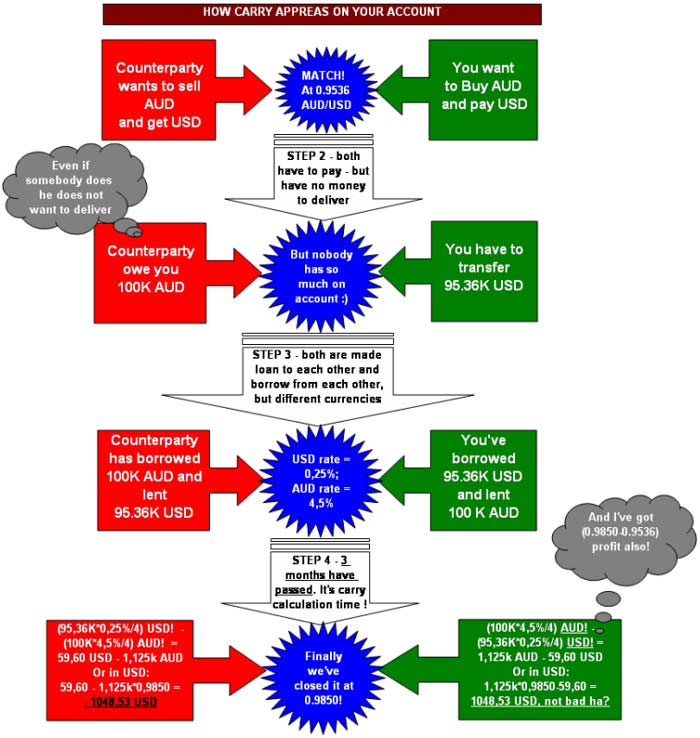

In fact leverage is what makes carry attractive on forex market. But let’s return to your example with AUD/USD… I’ve prepared a picture for that - here it is, take a look. You may assume any leverage you want – it will not change the major idea…

Commander in Pips: Sure, go ahead!

Commander in Pips: Perfect! You’ve really surprised me… So, for those who intend to dive into carry positions, there are two issues are preferable to see:

- As low volatility as it could be – if rate will not change at all – all the better;

- As large difference in rate as it possible.

That is the dream of traders who intend to enter carry trade.

Pipruit: Well, it looks like to borrow at 5% and to lend at 10% per year, for example. So, your profit will be 5% per year. But, sir, I’m not very fascinated with just 5% or even 10% per year and, second, I like to trade, to analyze charts, indicators, you know. Why we’ve spent so much time with it?

Commander in Pips: Well, concerning about 5% annually – this is without leverage. Add here 20 times leverage and you will double your account… But this will only happen if you will use the total value of your account as a margin. Nevertheless, even 50% profit from carry trade is not bad, right?

Now about the second – don’t be too hasty. We will discuss this topic and how to involve it in day-by-day operations.

Carry Structure

Although you’ve explained me this topic pretty well, I think that we can spend some time and make fast repeat of that. Let’s choose some pairs with significant different in rates… What do you offer?

Pipruit: The highest rate right now among the majors is for the AUD, while for the low rates we can take the JPY or even the USD...

Commander in Pips: All right let’s take AUD/USD. AUD rate now is 4.5% while USD rate is 0.25%. Hence, carry rate will be 4.50-0.25 = 4.25% - not bad ha - greater than what you can get on 10 year US Treasuries bonds.

Still, on the bond you have to wait for a maturity date – this is a long time, while on forex this difference is deposited or withdrawn from your account balance daily. That’s another small positive splash of the forex market. This transaction is made by your broker.

Pipruit: Hm, and how does he know how long I will hold my position?

Commander in Pips: You don’t understand. Your broker deposits or withdraws the sum of carry just for passing a single day. If you will hold position for one more day –he will do this again by close, and so on. Carry result (positive or negative) accumulates on your account day by day. When you will finally close your position – you will get the carry accurately for the term that you’ve held it open.

Pipruit: OK, I see. And why do you said “deposit or withdraw”?

If you hold your position overnight, broker makes its so-called “roll over” – closes it and opens at the same quote. All spot forex positions close by the end of the day. This “day” term is a bit blurry and depends on your broker. Each broker has its own “closing day time”, but as a rule this time coincides with 0:00 of local time or some major time zone. Your broker closes your position and reopens again at the same quote, so you do not even see it. At the same moment it deposits or withdraws the carry cost for the past day. So this transaction of closing and reopening calls “Roll over”.

In fact leverage is what makes carry attractive on forex market. But let’s return to your example with AUD/USD… I’ve prepared a picture for that - here it is, take a look. You may assume any leverage you want – it will not change the major idea…

Pipruit: Wow, looks great. But can I ask some “thin” questions?

Commander in Pips: Sure, go ahead!

Pipruit: Well, you’ve recalculated the value of carry at position closing moment. But how in this case, does the broker act, since he does not know when we will close it?

Commander in Pips: Absolutely correct question. If fact, the broker converts carry value at close price every day. Here I’ve shown the conversion just to attract attention to this fact. I did it for simplicity at close of position. But in reality, the broker does it every day of holding position at the day close price. Also I didn’t mention, but the conversion done in those currency that your account is. So, if you have dollar account then you will get carry in dollars, EUR – in euros and so on…

Commander in Pips: Strictly speaking you’re right, and large participants follow this procedure. But be careful with retail brokers, since they can have “not quite the same” procedures and “slightly other rates”. When you will intend to open real account, talk to broker about carry calculation procedure, since there could appear really bad surprises. For instance, some brokers could withdraw a fixed amount of money every day of holding your position despite what position do you carry – long or short, S&P500 futures, AUD/USD or CHF/JPY. Be careful with that, especially if you intend actively use this feature.

Ok, as an intermediate result, I want to discuss the possible results of such position. Let’s say, you’re long AUD/USD:

1. If AUD/USD rate has decreased – then your loss will be a bit smaller, since you’ve got positive carry. If this decreasing very shallow, you even can get profit still, but let’s look at this scenario as negative;

2. AUD/USD rate remains unchanged. You will get profit equals to carry.

3. If AUD/USD rate has increased, then you will get two different profits – one greater part from rate appreciation and second is carry.

What will happen if you’re short – just replace green rectangles with red ones…

Commander in Pips: Absolutely correct question. If fact, the broker converts carry value at close price every day. Here I’ve shown the conversion just to attract attention to this fact. I did it for simplicity at close of position. But in reality, the broker does it every day of holding position at the day close price. Also I didn’t mention, but the conversion done in those currency that your account is. So, if you have dollar account then you will get carry in dollars, EUR – in euros and so on…

Pipruit: But sir, in this case it appears to be some sort of double conversion. So, we need to find carry on both currencies and only after that convert it in EUR – AUD to EUR and USD to EUR and then find the difference, right?

Commander in Pips: Strictly speaking you’re right, and large participants follow this procedure. But be careful with retail brokers, since they can have “not quite the same” procedures and “slightly other rates”. When you will intend to open real account, talk to broker about carry calculation procedure, since there could appear really bad surprises. For instance, some brokers could withdraw a fixed amount of money every day of holding your position despite what position do you carry – long or short, S&P500 futures, AUD/USD or CHF/JPY. Be careful with that, especially if you intend actively use this feature.

Ok, as an intermediate result, I want to discuss the possible results of such position. Let’s say, you’re long AUD/USD:

1. If AUD/USD rate has decreased – then your loss will be a bit smaller, since you’ve got positive carry. If this decreasing very shallow, you even can get profit still, but let’s look at this scenario as negative;

2. AUD/USD rate remains unchanged. You will get profit equals to carry.

3. If AUD/USD rate has increased, then you will get two different profits – one greater part from rate appreciation and second is carry.

What will happen if you’re short – just replace green rectangles with red ones…

Pipruit: Heh, I’ve got it…

Comments

P

papao

12 years ago,

Registered user

Hi Commander and thank you for that lesson. I'd like to ask you some question.

1) according to Interest rate parity theory (in particular, the uncovered version), returns on domestic and foreign assets should be equal. This because the high yielding currency is expected to depreciate in order to balance the net return. The assumptions of the theory are strong and compelling, the theory seems to be correct so the carry trade shouldn't yield higher returns. From that perspective, higher returns on carry trade should be justified by the exchange rate risk. I know, we are traders and we don't take care of what should happen (like Efficient-market hypothesis, random walk etc.). But i'm curious: why the carry trade works? :-) I mean, why the high-yielding currency tend to appreciate? In fact, the covered interest rate parity theory seems to be very accurate (we can clearly see different quotes on spot and future market, even with tiny interest rate differentials).

2) however, a carry trade is a risky trade (like any other trade), and the amount of interest collected by the trade could be easily wiped out by a small movement of the market (in terms of pips). So, i was wondering if it was possible covering the position using options, in order to gain "risk free" leveraged interest. (For example, if we go long on AUD/USD, we can cover the risk buying a put. Paying the premium we are assured that if the market goes down, we gain interests, and if the market goes up we can also profit from the appreciation of the currency). Probably this is not possible (probably the premium is higher than the interests). And what about making a syntethic short position with options? (Let's say we are again long on AUD/USD. We can hedge that positino making a synthetic short position, buying a put and selling a call. In this case we couldn't profit from an appreciation of the high yielding currency, but the price would be lower (the cost of the put option minus the price of the call option)).

Thank you in advance!

1) according to Interest rate parity theory (in particular, the uncovered version), returns on domestic and foreign assets should be equal. This because the high yielding currency is expected to depreciate in order to balance the net return. The assumptions of the theory are strong and compelling, the theory seems to be correct so the carry trade shouldn't yield higher returns. From that perspective, higher returns on carry trade should be justified by the exchange rate risk. I know, we are traders and we don't take care of what should happen (like Efficient-market hypothesis, random walk etc.). But i'm curious: why the carry trade works? :-) I mean, why the high-yielding currency tend to appreciate? In fact, the covered interest rate parity theory seems to be very accurate (we can clearly see different quotes on spot and future market, even with tiny interest rate differentials).

2) however, a carry trade is a risky trade (like any other trade), and the amount of interest collected by the trade could be easily wiped out by a small movement of the market (in terms of pips). So, i was wondering if it was possible covering the position using options, in order to gain "risk free" leveraged interest. (For example, if we go long on AUD/USD, we can cover the risk buying a put. Paying the premium we are assured that if the market goes down, we gain interests, and if the market goes up we can also profit from the appreciation of the currency). Probably this is not possible (probably the premium is higher than the interests). And what about making a syntethic short position with options? (Let's say we are again long on AUD/USD. We can hedge that positino making a synthetic short position, buying a put and selling a call. In this case we couldn't profit from an appreciation of the high yielding currency, but the price would be lower (the cost of the put option minus the price of the call option)).

Thank you in advance!

Sive Morten

12 years ago,

Registered user

> Hi Commander and thank you for that lesson. I'd like to ask you some question.

1) according to Interest rate parity theory (in particular, the uncovered version), returns on domestic and foreign as..

Hi Papao,

nice questions.

I'm shame a bit, but I didn't hear about "Interest rate parity theory". I've heard about prescious metal (monetary theory) that better money push worse money - gold vs. silver for instance, or gold vs paper money.

Although I didn't think much about what you've said, but it sounds curious. For instance, Australia has AAA rating and 4.5% rate on its currency, while US has AA rating 0.25% rate and much worse fundamental ratios - deficit, debt burden, budget earnings/interest, M3 money supply and others. The reasonable question - why AUD should depreciate to USD? I see some nonsense in the statement that all curencies have to give the same return. Since USD now is more risky - it depreciate to AUD. And that is logical, because investors demand more USD for every AUD.

I can find the foundation for your theory only may be in inflation term, but I'm not sure. Here is make sense to take a look at real returns instead of nominal. In this case, may be, carry will be not so significant.

It works, because you may borrow Yens or USD for 0.25%, convert them in AUD and buy AAA gov. bonds for 4.5-6%. That's why it works. The most risk here is to make reverse transaction in time. It also depends on your major account currency. Also carry suggests low leverage or even abscense of it.

You can't hedge this neither by futures nor by options. Because if you will take a look at math - you'll see that currency options include rate differential for the term of option. So it price already includes this difference for term till expiration.

The same is with futures. It includes rate difference.

One thing that is possible somehow here is to create some structural product. For example, if you borrow money in USD, convert them and buy some AUD bonds - you may use some part of coupon income to buy USD/AUD options. This will reduce your overall income but you will be hedged against unwelcome AUD depreciation. But this is just an idea.

1) according to Interest rate parity theory (in particular, the uncovered version), returns on domestic and foreign as..

Hi Papao,

nice questions.

I'm shame a bit, but I didn't hear about "Interest rate parity theory". I've heard about prescious metal (monetary theory) that better money push worse money - gold vs. silver for instance, or gold vs paper money.

Although I didn't think much about what you've said, but it sounds curious. For instance, Australia has AAA rating and 4.5% rate on its currency, while US has AA rating 0.25% rate and much worse fundamental ratios - deficit, debt burden, budget earnings/interest, M3 money supply and others. The reasonable question - why AUD should depreciate to USD? I see some nonsense in the statement that all curencies have to give the same return. Since USD now is more risky - it depreciate to AUD. And that is logical, because investors demand more USD for every AUD.

I can find the foundation for your theory only may be in inflation term, but I'm not sure. Here is make sense to take a look at real returns instead of nominal. In this case, may be, carry will be not so significant.

It works, because you may borrow Yens or USD for 0.25%, convert them in AUD and buy AAA gov. bonds for 4.5-6%. That's why it works. The most risk here is to make reverse transaction in time. It also depends on your major account currency. Also carry suggests low leverage or even abscense of it.

You can't hedge this neither by futures nor by options. Because if you will take a look at math - you'll see that currency options include rate differential for the term of option. So it price already includes this difference for term till expiration.

The same is with futures. It includes rate difference.

One thing that is possible somehow here is to create some structural product. For example, if you borrow money in USD, convert them and buy some AUD bonds - you may use some part of coupon income to buy USD/AUD options. This will reduce your overall income but you will be hedged against unwelcome AUD depreciation. But this is just an idea.

P

papao

12 years ago,

Registered user

Thank you Sive for your quick answer.

> Hi Papao,

nice questions.

I'm shame a bit, but I didn't hear about "Interest rate parity theory". I've heard about prescious metal (monetary theory) that better money push worse money - gold vs. si..

no, i think this is a quite different theory :)

The interest rate parity theory is one (out of many) theory that tries to explain movements on exchange rates. I studied it in Macroeconomics (Oliver Blanchard, 4th edition). This is a quite simple theory. If we have similar assets (domestic and foreign, similar in riskiness and liquidity), and we can choose in which invest (or, we can move our capital in and out our country) we will choose the higher yielding asset. And this is obvious, both for local and foreign investors. So all investors should buy only the high yielding asset. (in order to buy the higher yielding asset they need to change their currency (they buy it in the spot market, and this lead to an appreciation of the spot rate), they buy the high yielding asset (and his price will increase, so his net return will decrease). Now they might either cover their position selling the revenue of the investment on the future/forward currency market (depreciating the future exchange rate. This is the covered version of the theory) OR they might wait the end of the investment and sell at that time the revenue of the investment (this is the uncovered version of the theory)). Anyway, this is a condition of non-arbitrage, and we can see it in action every time a central bank increase or decrease his rates surprising markets (money flows almost instantaneously on the higher yielding currency, and this keeps the net returns of investment in equilibrium).

(may be you can read a better explaination of the theory in wikipedia:

Interest rate parity - Wikipedia, the free encyclopedia

).

>

Although I didn't think much about what you've said, but it sounds curious. For instance, Australia has AAA rating and 4.5% rate on its currency, while US has AA rating 0.25% rate and much worse fun..

may be this isn't the right question (the exchange rate that we will have in the future should remain at his mid-long term level of equilibrium. It's the current, the spot rate, that is higher due to the mechanics explained by the theory).

>

I see some nonsense in the statement that all curencies have to give the same return. Since USD now is more risky - it depreciate to AUD. And that is logical, because investors demand more USD for e..

ok, i understood it. Of course, different risks justifies different returns. I posted my question because i'm always surprised seeing again and again how "strange" are markets (they are strange because they didn't always follow theories), and because i read on different books something about the carry trade (most of times they talk about it as a risk free trade, and it can't be!). Now i see we agree that is a risky trade (because of the risk in closing position and because the leverage (and the leverage makes it attractive, but implies additional risk)).

>

You can't hedge this neither by futures nor by options. Because if you will take a look at math - you'll see that currency options include rate differential for the term of option. So it price alrea..

ok, it would be too good for being true :D (and, i think, this is an effect (or a confirmation) to the covered interest rate parity (we can't get a risk free higher yielding)).

As usual, thank you Sive for your kindness!

> Hi Papao,

nice questions.

I'm shame a bit, but I didn't hear about "Interest rate parity theory". I've heard about prescious metal (monetary theory) that better money push worse money - gold vs. si..

no, i think this is a quite different theory :)

The interest rate parity theory is one (out of many) theory that tries to explain movements on exchange rates. I studied it in Macroeconomics (Oliver Blanchard, 4th edition). This is a quite simple theory. If we have similar assets (domestic and foreign, similar in riskiness and liquidity), and we can choose in which invest (or, we can move our capital in and out our country) we will choose the higher yielding asset. And this is obvious, both for local and foreign investors. So all investors should buy only the high yielding asset. (in order to buy the higher yielding asset they need to change their currency (they buy it in the spot market, and this lead to an appreciation of the spot rate), they buy the high yielding asset (and his price will increase, so his net return will decrease). Now they might either cover their position selling the revenue of the investment on the future/forward currency market (depreciating the future exchange rate. This is the covered version of the theory) OR they might wait the end of the investment and sell at that time the revenue of the investment (this is the uncovered version of the theory)). Anyway, this is a condition of non-arbitrage, and we can see it in action every time a central bank increase or decrease his rates surprising markets (money flows almost instantaneously on the higher yielding currency, and this keeps the net returns of investment in equilibrium).

(may be you can read a better explaination of the theory in wikipedia:

Interest rate parity - Wikipedia, the free encyclopedia

).

>

Although I didn't think much about what you've said, but it sounds curious. For instance, Australia has AAA rating and 4.5% rate on its currency, while US has AA rating 0.25% rate and much worse fun..

may be this isn't the right question (the exchange rate that we will have in the future should remain at his mid-long term level of equilibrium. It's the current, the spot rate, that is higher due to the mechanics explained by the theory).

>

I see some nonsense in the statement that all curencies have to give the same return. Since USD now is more risky - it depreciate to AUD. And that is logical, because investors demand more USD for e..

ok, i understood it. Of course, different risks justifies different returns. I posted my question because i'm always surprised seeing again and again how "strange" are markets (they are strange because they didn't always follow theories), and because i read on different books something about the carry trade (most of times they talk about it as a risk free trade, and it can't be!). Now i see we agree that is a risky trade (because of the risk in closing position and because the leverage (and the leverage makes it attractive, but implies additional risk)).

>

You can't hedge this neither by futures nor by options. Because if you will take a look at math - you'll see that currency options include rate differential for the term of option. So it price alrea..

ok, it would be too good for being true :D (and, i think, this is an effect (or a confirmation) to the covered interest rate parity (we can't get a risk free higher yielding)).

As usual, thank you Sive for your kindness!

dkami

12 years ago,

Registered user

Hi Sive Thanks for this lesson as I have been waiting for a carry trade lesson to hopefully pick up some more tips;)

This is all I do to get great 50++% returns even with my low leverage system I use with little more than 5min work a day,Swap + pip profit its really a no brainer:D

Got to love the AUD/JPY and am a proud Aussie:D

Looking forward to reading part 2

Thanks again Sive for sharing

This is all I do to get great 50++% returns even with my low leverage system I use with little more than 5min work a day,Swap + pip profit its really a no brainer:D

Got to love the AUD/JPY and am a proud Aussie:D

Looking forward to reading part 2

Thanks again Sive for sharing

Pharaoh

12 years ago,

Registered user

Personally, I'm annoyed that kangaroo currency is doing so well against the USD in the long run, but do enjoy the swap interest. :p

What really ticks me off how most brokers find this as an easy way to steal more money from traders. I don't expect positive swap on a pair to be exactly equal to negative swap, but I've seen cases where the negative swap on a pair was 4 or 5 times larger than the positive swap and also cases where swap was negative in both directions. :mad:

What really ticks me off how most brokers find this as an easy way to steal more money from traders. I don't expect positive swap on a pair to be exactly equal to negative swap, but I've seen cases where the negative swap on a pair was 4 or 5 times larger than the positive swap and also cases where swap was negative in both directions. :mad:

Sive Morten

12 years ago,

Registered user

> Personally, I'm annoyed that kangaroo currency is doing so well against the USD in the long run, but do enjoy the swap interest. :p

What really ticks me off how most brokers find this as an easy way ..

Right. This is extremely important notice on OTC Forex market. I totally agree that understanding of swap calculation with particular broker is must, especially if you are planning to rely on swap as a part of your total income.

From that perspective trading futures on AUD/USD is much safer - here is no voluntarism in swap calculation ;)

What really ticks me off how most brokers find this as an easy way ..

Right. This is extremely important notice on OTC Forex market. I totally agree that understanding of swap calculation with particular broker is must, especially if you are planning to rely on swap as a part of your total income.

From that perspective trading futures on AUD/USD is much safer - here is no voluntarism in swap calculation ;)

A

Aldo Colombo

12 years ago,

Registered user

> Hi Papao,

nice questions.

I'm shame a bit, but I didn't hear about "Interest rate parity theory". I've heard about prescious metal (monetary theory) that better money push worse money - gold vs. silv..

I´m interested in basic theory, I couldn't find what you refer to as "better money push worse money", why would gold be better than silver or paper money?

nice questions.

I'm shame a bit, but I didn't hear about "Interest rate parity theory". I've heard about prescious metal (monetary theory) that better money push worse money - gold vs. silv..

I´m interested in basic theory, I couldn't find what you refer to as "better money push worse money", why would gold be better than silver or paper money?

Sive Morten

12 years ago,

Registered user

> I´m interested in basic theory, I couldn't find what you refer to as "better money push worse money", why would gold be better than silver or paper money?

Hi Aldo, just because it is worthy and has greater value. I suggest you to read classical monetary theories.

Just imagine that you're some producer of some goods. You will be offered to pay for your goods either with gold, silver or paper money. What you will choose?

Hi Aldo, just because it is worthy and has greater value. I suggest you to read classical monetary theories.

Just imagine that you're some producer of some goods. You will be offered to pay for your goods either with gold, silver or paper money. What you will choose?

Table of Contents

- Introduction

- FOREX - What is it ?

- Why FOREX?

- The structure of the FOREX market

- Trading sessions

- Where does the money come from in FOREX?

- Different types of market analysis

- Chart types

- Support and Resistance

- Candlesticks – what are they?

- Mysterious Fibonacci

- Introduction to Moving Averages

- Bollinger Bands

- Leading and Lagging Indicators

- Basic chart patterns

- Pivot points – description and calculation

- Elliot Wave Theory

- Intro to Harmonic Patterns

- Divergence Intro

- Harmonic Approach to Recognizing a Trend Day

- Intro to Breakouts and Fakeouts

- Again about Fundamental Analysis

- Cross Pair – What the Beast is That?

- Multiple Time Frame Intro

- Market Sentiment and COT report

- Dealing with the News

- Let's Start with Carry

- Let’s Meet with Dollar Index

- Intermarket Analysis - Commodities

- Trading Plan Framework – Common Thoughts

- A Bit More About Personality

- Mechanical Trading System Intro

- Tracking Your Performance

- Risk Management Framework

- A Bit More About Leverage

- Why Do We Need Stop-Loss Orders?

- Scaling of Position

- Intramarket Correlations

- Some Talk About Brokers

- Forex Scam - Money Managers

- Graduation!