Part II. Relation with Other Financial Markets

Relationship with the Bond market

Commander in Pips: Initially I would like to say couple of words about bonds – just so you can become clear about what the beast is. Speaking simply and not diving into different nuances – “Bond” and “loan” have many similarities. Governments, municipal or corporations issue bonds to borrow money. A simple bond has the same requisites as any loan – notional value, term, percent rate, period of payment of accrued interest and maturity date. Bonds are purchased by those who have money and want to invest it with some predefined yield, term and risk level. They are those who lend money to the borrower. Borrowers are, in turn, those, who issue bonds. So, if you, for example will buy a bond of US Treasury – you will be a lender, a creditor of the US Government.

Pipruit: And could you give some more clarification to different terms – “yield”, “term”, “notional” and so on.

The second important parameter is annual coupon yield of the bond – the percent rate that will be paid on the notional value during whole time of the bond existing. Usually it is paid on some predefined schedule – mostly semiannually, but sometimes annually or quarterly. This is almost the same as a percent on your deposit in the bank.

Let’s suppose that you’ve bought US Government bond with principal value of 100K and coupon yield 5%. Coupon yield always shows annual rate. It means that if you will hold this bond for 1 year, you’ll get 5%*100K = 5K. Since the US Government makes coupon payments semiannually – you’ll get 2.5K after 6 months and another 2.5K at the end of the year. In fact, your yield will be a bit greater, since you may reinvest the first 2.5K at some yield, but this is a bit of an advanced conversation, so we will skip it.

The third important parameter is the term of the bond. Term shows how long a time the bond will give you coupon payments and when you will get the notional amount back. What your buddy tells you, if you ask him to return 100 bucks?

Pipruit: Hm, probably he will say, that will try to return on next week but not sure about it…?

Commander in Pips: The most common approach to this is to use not just one but two MAs on the chart.

Pipruit: And what it could give us?

The next two parameters are more complicated. They are Price and yield to maturity (YTM) of the bond. Price is relatively simple and it’s measured in percents from notional value. If Price = 100% it means that you have to pay the notional amount – 100K. If price = 85%, then it will be 100*0.85 =85K USD, Price = 120%, then it will be 120K USD.

YTM is most complicated parameter. In fact it shows your annual return on your investments till the maturity date of a particular bond. It depends on term till maturity, coupon rate and price of the bond. For instance, if you buy bond at price that is higher than notional value – then your yield will be lower than coupon, since you’ve paid more, but coupon is calculated based on notional amount. And vice versa – if you’ve bought the bond with price lower than principal – then your annual yield till maturity will be greater than coupon payment.

Pipruit: And why?

Commander in Pips: It’s simple. Assume that you’ve bought the bond at 120%, i.e. 120 K, but notional amount is 100K. During time till maturity you will receive the same coupon of 5K annually, but at maturity you will get just 100K, since this is notional amount, while you’ve paid 120K – this difference of 20K reduces your total profit from owning the bond, hence your yield will be lower than 5%. The opposite is true if you’ve bought the bond cheaper than the notional amount.

Pipruit: And how it is possible?

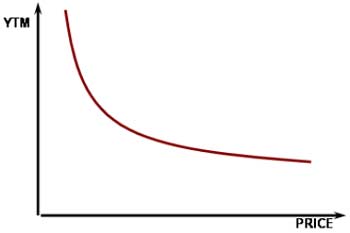

But the relation between YTM and Price is not linear – it looks approximately as on the chart:

Pipruit: Well, that’s very interesting, really. But how does all this stuff relate to the Forex market?

Commander in Pips: Since we’ve turned to education of inter-market relations and already have met with Gold and Oil, don’t you think that Forex has relations with other markets also?

Pipruit: Well, I can’t exclude that.

Commander in Pips: Thanks. I will tell you more. In fact, the bond market, i.e. percent rates market is a carcass of economy cycles frame work, since this is a major tool of central banks to control the balance between inflation and growth. Bonds are financial instruments that allow interest rates to be traded. You probably do not know this, but there are futures exist on Fed Fund Rate also, and on the 3-month rate, and 6-month, 1, 2-year, 10-year, 30-year and some others. This is a huge market. In fact bonds are the closest assets to economic cycles and the most sensitive to them. Let’s remember the Dollar Smile theory from the Dollar Index chapter. When does the US dollar usually rise by this theory?

Pipruit: Well, first, when the economy falls in recession, risk aversion and flight to quality appears. Second is when the economy starts to exit from recession and turns to growth. On that stage the dollar mostly grows due improving of overall situation in the economy and hiking of interest rates.

Pipruit: Well, I think so, but could you show me some charts…

Commander in Pips: Be my guest:

Chart #1 | Dollar Index (red) and 10-year note futures price (black), monthly

Pipruit: Well, I recognize the US DX chart, since I’ve seen it in a previous chapter. The first jump was due to the run-to-quality turmoil, and we see that price on 10-year not has risen significantly, later there was some relief, and an attempt to exit from recession that has failed. In fact, this was just turned into the second leg and W-shape of recession. Now we see that fast growth in US 10-year notes and I suppose that this is because of risk aversion again due to solid problems in the EU – Greece and Italy in particular.

Commander in Pips: You’re absolutely right, but maybe you see something else?

Pipruit: Well, it looks like the US DX a bit lagging behind the 10 year interest rates chart…

Commander in Pips: This is just one way to interpret it. But since this is a cycle – it’s very difficult to say what is lagging and what is advancing. From one point of view, we might say that since interest rates have started to rise – dollar index turns to growth, but from another point of view, since inflation is significant due to dollar devaluation – it forces the rising rates. In fact Bonds and the US Dollar stands right at the edges of cycle and encircle it, if we can say so. If bonds are our starting point, then we can think as follows: After a recession, when inflation is anemic and rates are low – the economy starts to climb out of a pit. This is an attractive time to borrow money, and hence, increase production and invest in business development. Since corporations are starting to grow momentum – stock market turns to growth also. Growing economy demands more raw materials – this leads to price growth for commodities. Since commodities becomes more expensive relatively to US Dollar – inflation starts to growth and this demands rate increasing by Fed to control inflation and this procedure leads to growth in the US Dollar.

Commander in Pips: In fact, the Dollar shows major growth at the inflationary stage of growth and reaches peaks right at recession. If we start to analyze from the dollar stand point, we might say, that the dollar so expensive that it does not allow increasing production any more and goods are loosing attractiveness compared to rival ones. This leads to chilling out in the economy, reducing of pace of growth and turning to stagnation again that usually corresponds with rate decreases and that causes the dollar to fall.

But the major lesson for us is to keep an eye on the bond market, since we know that this correlation exists although there is some lag time between those two assets.

Hence, this is first application of the bond market – it is an excellent barometer of the overall economy. With some lag rising yield (reducing of price) of bond market is a bullish for Dollar, while yield decreasing (price growth) is bearish, except the fast period of risk aversion and flight to quality. During these moments safe-haven assets are growing together – as US Bonds as US Dollar. Reasons are not cyclical, but mostly technical – flow of capital into safe assets.

Pipruit: And how we can I understand – whether it risk aversion or just recession since yield starts to fall?

Commander in Pips: Very simple. Risk aversion appears when Fed rates are high. This is the first significant plunge on markets. Recession comes later, when the Fed has turned to decrease rates already. We even might say, that the initial plunge by risk aversion is recession start point.

Pipruit: Ok, now it becomes clear.

Commander in Pips: The second application is the impact on the stock market. Since stocks are treated as more risky assets than bond ones, bond’s dynamic could be nice indicator of stock market. If investors flow into bonds, it could be a signal that they are uncertain about economic perspectives and need to make their assets safer rather than to make enhanced returns on them. This will lead to a sell-off on stock markets. Later, when economic perspectives become clear and stable, investor money flows back to equities, with hope to gain higher return.

BOND SPREADS

Commander in Pips: I just want to give you small add-on to the bonds topic. First what spread is. Spread is just a difference between yields to maturity (YTM). Spreads could be inter-market or intra-market. Intermarket spread is the one that calculates spread between bonds of different countries but equal maturity. For instance 10-year US Treasuries YTM and 10-year Australian Government note. This kind of spreads has a close relationship to carry trade that we’ve discussed in the corresponding chapter. In fact, this spread shows the value of this carry trade in time, since rates are subject to change since they are traded on an open market.

If you draw on the chart spread between 2-year US Treasuries notes and 2-year Australian notes – you will find that it closely repeats the chart of the AUD/USD, since as spread rises – the cost of carry also rises and that is linked with appreciation of the AUD. When suddenly rates have been decreased by the Australian Central Bank and Fed Reserve – spread has tighten significantly, cost of carry reduced and this has led to closing of AUD positions and decreasing of the AUD/USD.

The second type of spread is intra-market. This is the spread that calculates between bonds of the same country but with different maturities. For instance, the spread between 10-year US Treasuries note and 2-year notes. Since short-term rates are tightly linked with the Fed rate – they react faster on Fed policy. This spread widens during recession period and tightens during growth.

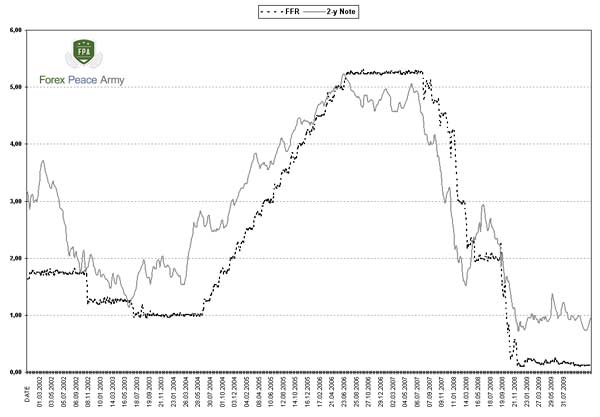

Here is the chart of 2-year Treasury note and Fed Fund Rate:

Chart #2 | 2-year US Treasuries note and Fed Fund rate

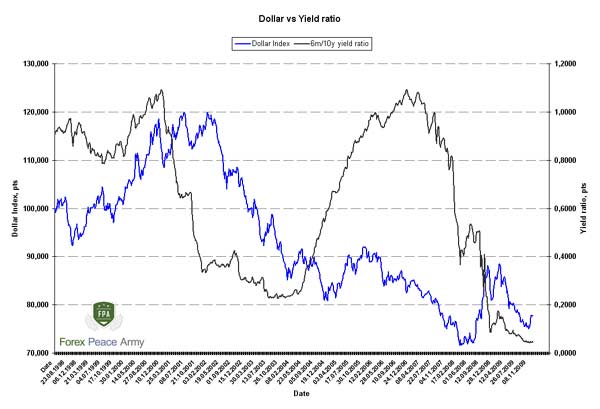

It is based not on subtraction but on division 6-month YTM on 10-year YTM:

Chart #3 | 6m/10y US Treasuries ratio and Dollar Index

We see some kind of dependence between them, but as we previously said – it’s not as obvious as AUD/USD with Gold, for instance. Still if you’re interested in this topic – there is a lot of space for your own study. Here you clearly see the cycles by Ratio. Reducing of the black line shows periods of rate decreasing and recession, while increasing shows growth in the economy and rate hiking.So, tell me how you will use bonds on Forex market?

- Pipruit: Ok, I’ll try:

1. When the Central Bank’s rates right on top and the economy overheated – fast bond yield decreasing will be the first bell of possible chilling out of the economy and leads to fast appreciation of Dollar value. This is a run-to-quality due risk aversion. Also the same could happen with Switzerland's currency and bonds;

2. Inter-market spread is an excellent indicator of carry value. Reducing of spread tells us that carry attractiveness significantly decreases and this leads to depreciation of the carry currency, for example, of the AUD/USD;

3. After the initial splash in bond yields during risk aversion – spread will gradually increase. When rates are at low during recession stage bond spread stands at maximum value;

4. Starting of short-term interest rate increases during recession period that is supported by good macro economic data could be the signal of starting point of economy growth. Some time after that rate hiking will come and increasing of US Dollar;

5. We must take into consideration risk aversion moments – rising yields, especially in short-term bonds after recession is dollar bullish with some lag, while falling yields – is bearish.

Commander in Pips: Yes, you’re absolutely right. At the end of this part I want to give you an important notification. You may speak about possible appreciation or depreciation of some currency due higher rates only if it compares with currency approximately of the same credit quality. For instance, AUD/USD – AUD credit rating by S&P is AAA while US is AA+ (was AAA also). Carry here is about 4.0-4.25% - these are acceptable currencies to compare. If you will take a look at say USD and Russian ruble you will see even greater carry – around 8.0%, but Russia has BBB+ rate – this is 6 grades lower than the US. Each grade costs approximately 0.5%. So, the real spread adjusted for credit risk will be around 5% - almost the same as AUD/USD, but inflation in Russia is much higher – 8-15% in different years. That’s why using USD/RUR spread absolutely does not mean that RUR will appreciate in time. Keep it in mind, when you will assess some exotic pairs.

That’s being said, this correlation works with major currencies or exotic but of approximately equal credit quality. Increasing of the spread between some economies leads to appreciation of the currency with the greater rate. Since all interest rates in country links with rate of Central Bank – it has a tendency to grow in other rates also. Hence, it leads to higher return on all bonds in the country. If a country could give investors higher return of the same credit quality – this is quite attractive for them, isn’t it?

Just be sure, as we’ve said that you compare interest rates with the same maturity also. Otherwise your analysis will be vain. Also I want to give you some web resources where you can find data on interest rates:

1. Bloomberg

2. Eurostat

3. Fed Reserve of New York

4. Fed Reserve

5. FRED

6. Econstats

There is a lot macro data also – may be you will dive in fundamental analysis and inter-markets correlations, who knows…

Comments

A

Aldo Colombo

12 years ago,

Registered user

From my understanding 5% annual rate would not mean 2.5% semi annually, but sqrt(1.05), that is 2.47%. Am I wrong?

Another question: I noticed that bond quotations for long term bonds (as in

https://www.bloomberg.com/markets/rates-bonds/government-bonds/us/

for example) correspond to bonds issued this year. The previous bonds, which must be nearer to maturity, aren´t they traded as well? Anyone can sell or buy bonds at any time?

Thank you

Another question: I noticed that bond quotations for long term bonds (as in

https://www.bloomberg.com/markets/rates-bonds/government-bonds/us/

for example) correspond to bonds issued this year. The previous bonds, which must be nearer to maturity, aren´t they traded as well? Anyone can sell or buy bonds at any time?

Thank you

Sive Morten

12 years ago,

Registered user

> From my understanding 5% annual rate would not mean 2.5% semi annually, but sqrt(1.05), that is 2.47%. Am I wrong?

Another question: I noticed that bond quotations for long term bonds (as in

U.S. Go..

Hi Aldo,

you're speaking about compounding of coupon payments and you use geometric approach, assuming potential reinvestment of coupon payment, if it pays semi-annually. I will tell you even more, if you reinvest coupon payment at lower rate than yield to maturity, you will give even lower return. So, appling devision just by 2 is approximation.

Yes, you're right all previously issued bonds remain in turnover till maturity. They call "off the run" securities. The most recent issue calls "on the run".

Another question: I noticed that bond quotations for long term bonds (as in

U.S. Go..

Hi Aldo,

you're speaking about compounding of coupon payments and you use geometric approach, assuming potential reinvestment of coupon payment, if it pays semi-annually. I will tell you even more, if you reinvest coupon payment at lower rate than yield to maturity, you will give even lower return. So, appling devision just by 2 is approximation.

Yes, you're right all previously issued bonds remain in turnover till maturity. They call "off the run" securities. The most recent issue calls "on the run".

Table of Contents

- Introduction

- FOREX - What is it ?

- Why FOREX?

- The structure of the FOREX market

- Trading sessions

- Where does the money come from in FOREX?

- Different types of market analysis

- Chart types

- Support and Resistance

- Candlesticks – what are they?

- Mysterious Fibonacci

- Introduction to Moving Averages

- Bollinger Bands

- Leading and Lagging Indicators

- Basic chart patterns

- Pivot points – description and calculation

- Elliot Wave Theory

- Intro to Harmonic Patterns

- Divergence Intro

- Harmonic Approach to Recognizing a Trend Day

- Intro to Breakouts and Fakeouts

- Again about Fundamental Analysis

- Cross Pair – What the Beast is That?

- Multiple Time Frame Intro

- Market Sentiment and COT report

- Dealing with the News

- Let's Start with Carry

- Let’s Meet with Dollar Index

- Intermarket Analysis - Commodities

- Trading Plan Framework – Common Thoughts

- A Bit More About Personality

- Mechanical Trading System Intro

- Tracking Your Performance

- Risk Management Framework

- A Bit More About Leverage

- Why Do We Need Stop-Loss Orders?

- Scaling of Position

- Intramarket Correlations

- Some Talk About Brokers

- Forex Scam - Money Managers

- Graduation!